TELUS: A Canadian Telecom Targeting 7-10% Annual Dividend Growth

Formed in 1990, Telus (TU) is one of Canada’s major telecom businesses and a leading wireless provider. The firm's operations are grouped into two segments:

Wireless (57% of revenue, 66% of EBITDA): Telus's 4G LTE network covers 99% of Canada's population. The company makes money by selling voice and data services and equipment.

Wireline (43% of revenue, 34% of EBITDA): primarily sells high-speed internet, home phone, and cable TV services. Home phones are in secular decline but only account for about 10% of company-wide revenue, so this segment has continued reporting growth despite this exposure. Telus's Wireline business also includes healthcare technology solutions, home security, and managed IT and business process solutions.

Telus has paid dividends since 1999, although the firm cut its payout by more than 50% in 2001 to free up cash to grow its wireless and internet businesses across the country. Telus has paid uninterrupted dividends since then and targets 7% to 10% annual dividend growth through 2022.

Business Analysis

Telus used to be a regional telecom player, but in 2000 it acquired Clearnet Communications for $6.6 billion. This deal transformed Telus into a blossoming national wireless company while also broadening the range of bundled services it could offer.

In other words, acquiring Clearnet positioned Telus to go head-to-head with major rivals Bell Communications and Rogers Communications. The company’s efforts to build out its mobile-phone presence across Canada in the years following the deal have been very successful.

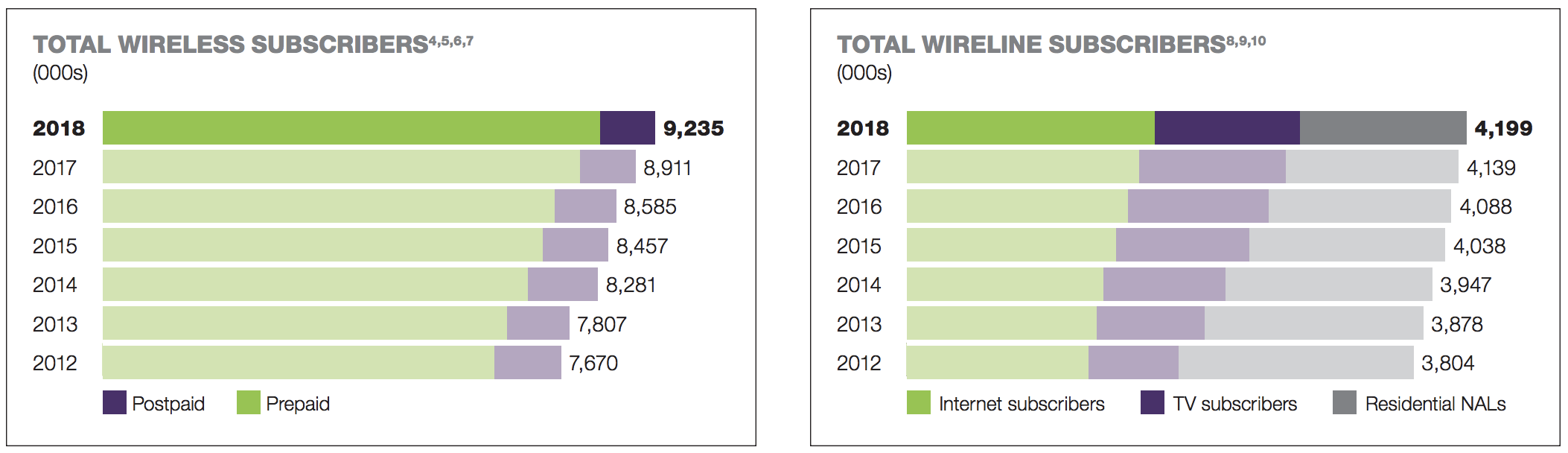

Today Telus has about 23% market share of Canada's $63 billion telecom industry, which is growing at a low-single digit pace, according to the firm's annual report. As you can see, Telus has done an admirable job of growing consistently over time, in both its wireline and wireless business.

Source: Telus Annual Report

While the decline in the residential landline phone business has tripped up some telecom companies, Telus has undertaken a multi-year restructuring to evolve its wireline business towards faster-growing internet, pay-TV, and data-focused businesses.

As a result, home phones only account for about 10% of Telus's revenue today, and wireline data businesses such as high-speed internet services, business process and IT solutions, and digital health solutions generate 33% of sales.

However, the company's main growth driver is still its wireless business, which generated 66% of firm-wide EBITDA in 2018. Telus has invested heavily ($2 billion to $3 billion per year in capex, or over 20% of sales) into expanding its 4G LTE network which covers 99% of Canada's population. In Canada, Telus is analogous to Verizon in the U.S. with the best national wireless network.

Year after year, industry surveys rank Telus at or near the top of the list for having the fastest wireless network and best customer service. This combination has resulted in Telus achieving industry-leading average monthly churn figures (i.e. high customer retention).

Low churn helps maximize the lifetime revenue per subscriber that Telus earns, providing the reliable cash flow the company needs to continue investing in the performance and reliability of its network to create a virtuous cycle of success.

To retain its lead in wireless, the company is testing out 5G technology which it expects to bring to Canada in 2020. Telus expects to build out a leading 5G wireless network that will allow it to hopefully dominate not just phones, but also wireless internet and devices connected to the so-called internet of things, such as driverless cars.

At the end of the day, consumers and businesses value the reliability of Telus's wireless network and its reputation for superior performance. As long as Telus continues to invest in its leading network coverage and architecture, the company should continue maintaining a massive base of customers. Disrupting Telus's base of customers would be almost impossible barring a revolutionary change in network technologies.

For one thing, growth in the number of new wireless subscribers has slowed with smartphone adoption now being widespread. With new customer growth hard to come by, the industry has consolidated to become more productive and expand coverage. In fact, the three largest mobile service providers account for more than 90% of retail mobile revenues, according to the Canadian Radio-television and Telecommunications Commission.

Telus's large subscriber base (over 9 million wireless subscribers) provides it with the cash flow needed to support and enhance its existing wireless network. Potential new entrants lack the subscriber base needed to fund a nationwide wireless network and acquire spectrum licenses, effectively keeping them locked out of the market.

Trying to win subscribers over from Telus would be extremely costly and impractical for almost any newcomer. It’s a lot easier to maintain an existing large base of subscribers in a mature market than it is to build a new base from scratch.

Simply put, new entrants lack the capital, spectrum, and subscriber base to effectively compete with any of the big three carriers in the Canada. In addition to the industry’s high barriers to entry, the wireless communications market is also appealing because its services are non-discretionary in nature.

In recent years, Telus's monthly postpaid churn rate has averaged less than 1%. The majority of the company’s revenue is also recurring because consumers and businesses have a continuous need to communicate and use data, even during recessions.

As mobile and broadband usage continues growing with increased consumption of data and video, Telus' wireless network should become increasingly valuable.

Key Risks

First, note that as a Canadian company, Telus pays its dividend in Canadian dollars. This creates some currency risk in that a stronger U.S. dollar might decrease the effective dividend amount for American shareholders, at least in the short term (each quarterly dividend is converted from Canadian dollars to U.S. dollars when it is paid, based on prevailing exchange rates).

In addition, like all Canadian stocks, U.S. Telus investors face a 15% foreign dividend tax withholding. Tax treaties between the U.S. and Canada allow U.S. investors to potentially recoup this withholding, but it can be a complicated and lengthy amount of paperwork at tax time.

There are several company-specific risks to consider as well.

Telus, Rogers, and Bell are Canada's three national carriers who command around 90% of the wireless market in Canada. However, in recent years the Canadian Radio-television and Telecommunications Commission, which regulates the industry, has become concerned about a lack of competition.

This has resulted in some unfavorable developments for Telus. For example, a 2015 rule change capped wireless contracts at two years (previously they had been as long as three years).

A major new entrant could also disrupt the Canadian telecom industry’s favorable structure. In 2012, for example, the industry grew fearful that Verizon was planning to buy wireless company Wind Mobile in an effort to enter Canada and challenge the three major incumbents. Valuation multiples quickly droppedbetween 7% and 27% for Telus, Bell Communications, and Rogers.

While the potential threat from Verizon never materialized, cable operator Shaw Communications (SJR) ended up acquiring spectrum-rich Wind Mobile for $1.6 billion in March 2016, marking its entry into the wireless market in an effort to better compete with Telus’ bundled services. Shaw can now offer television, wireless, and internet in major urban areas such as Ontario, Alberta, and British Columbia.

Here’s what Shaw CEO Brad Shaw said in an interview, according to TheTelecomBlog.com:

“Wireless was a missing piece. Now we’re on the same page, we’re at the same level…and we’ve improved our competitive position in Western Canada just by doing this deal, let alone the opportunity in the East.”

Shaw rebranded the wireless business Freedom Mobile and positioned it as a lower-priced option compared to the major three operators (driven by its inferior service quality). Regardless, Shaw is looking to play the role of disruptor and is now the fourth telecom company to cover the entire length of Canada.

Should Freedom Mobile improve its network coverage and quality enough to experience strong growth (Freedom Mobile had 1.6 million wireless subscribersas of June 2019), the big three incumbents could face subscriber growth pressure and margin compression over the coming years.

The good news is that the Canadian wireless market is still growing, providing some elbow room, and Telus continues reporting solid network performance and customer service results, as demonstrated by its subscriber growth and churn rates.

Only time will tell if Telus’ superior network quality and customer service will allow it to continue enjoying its industry-leading churn rate and average revenue per user, or if it will ultimately face the greatest pressure to lower prices in an effort to close the gap with lower-priced competition. That's arguably the biggest risk factor investors need to monitor.

Aside from the high degree of competition across Telus's wireless and wireline businesses, the telecom industry is very capital intensive. From acquiring 5G wireless spectrum to building out a modern network of fiber optic lines to provide faster internet, Telus's capital expenditure needs could increase in the future, depending on how competitive and technological trends evolve.

Higher investments could slow the firm's free cash flow growth and stretch Telus's balance sheet. Fortunately, management runs the business conservatively and expects Telus to maintain an investment grade credit rating. Furthermore, Telus's industry-leading network performance and churn rates suggest the firm has not been underinvesting in its business, reducing future surprises.

Another threat to Telus' wireless business is the potential for very expensive bidding to acquire 5G wireless spectrum. With just three major players in the market, if Telus and its major peers get into a bidding war and overpay for this spectrum, than their capex costs could soar, crimping profitability and limiting how fast they could grow their dividends.

Closing Thoughts on Telus

As Canada's largest wireless provider, and one of the most dominant telecoms in the country, Telus enjoys large economies of scale and a predictable recurring revenue business model.

The company has only reinforced its competitive advantages by continuing to upgrade its wireless network and offer relevant services as consumers' needs evolve. This has helped Telus achieve the industry's best customer service reviews and retention rates.

Despite some of the potential challenges facing the telecom sector (market saturation, a potentially disruptive fourth player in Freedom Mobile), Telus has proven itself to be capable of adapting well over time. The business has been a reliable source of safe and growing dividends over the years, and that seems unlikely to change anytime soon.