TJX Companies: An Impressive Retailer Paying Higher Dividends Since 1987

Founded in 1976, TJX Companies (TJX) has grown into the world’s largest off-price retailer, selling deeply discounted brand name and designer fashions. TJX's prices are generally 20% to 60% below department and specialty stores' regular prices on comparable merchandise.

The company’s core customer is a fashion and value conscious female shopper between 25 and 54 years old who makes a middle to upper-middle income. This type of customer usually shops high-end and moderate department and specialty stores, as well as online.

The company’s 4,000-plus stores operate under the T.J. Maxx, Marshalls, HomeGoods, Winners, HomeSense, T.K. Maxx, and Sierra (plus several e-commerce sites). TJ Maxx and Marshalls account for the majority of locations.

By product category, apparel and footwear generate 52% of the company's sales, followed by home fashions (33%) and jewelry and accessories (15%). Around 80% of the company’s sales and profits are derived in the U.S.

TJX has paid a higher dividend each year since going public in 1987.

Business Analysis

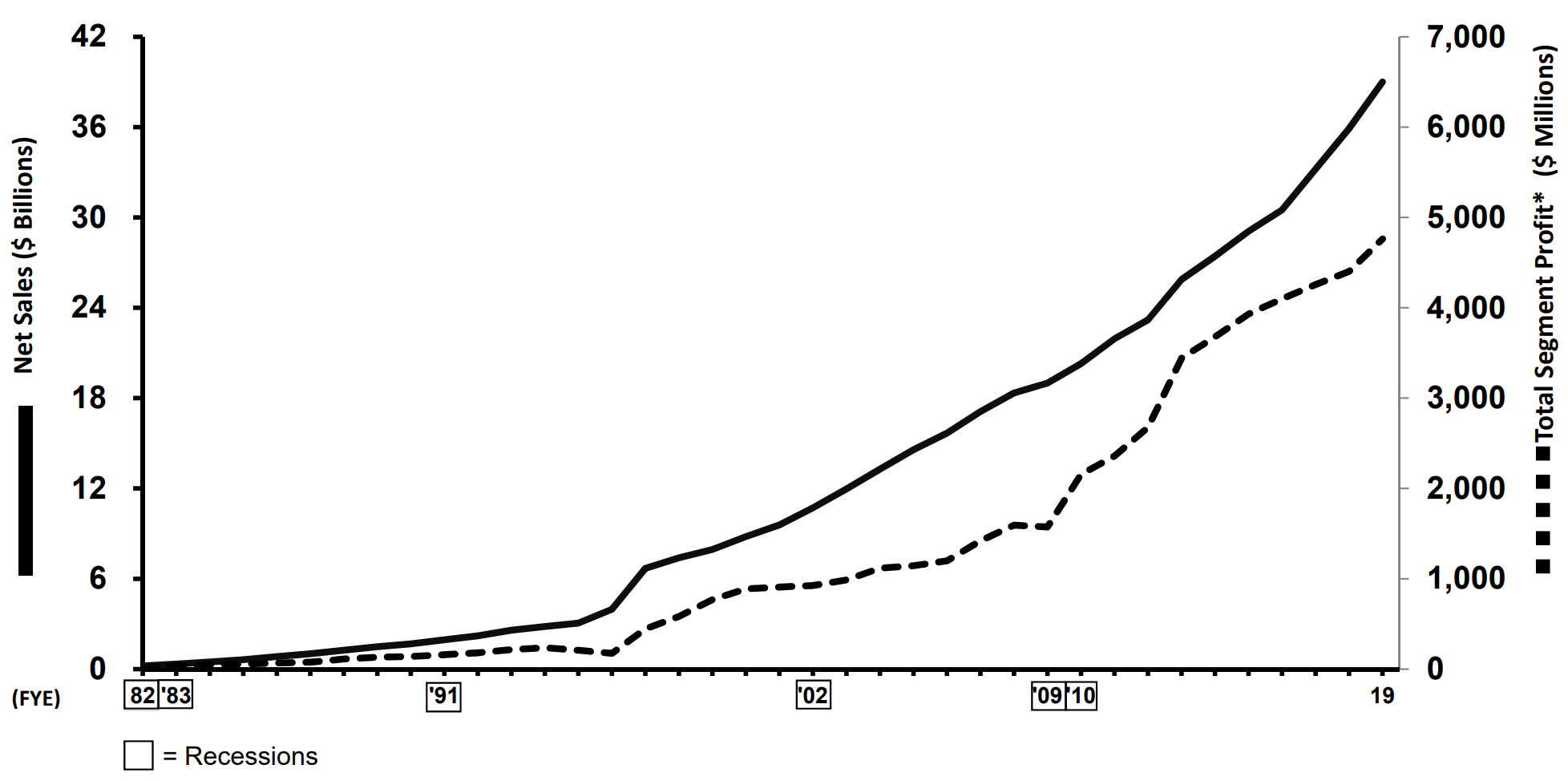

Retail is a cyclical and challenging business thanks to high economic sensitivity, fickle consumer trends, and cutthroat competition leading to low margins. Yet TJX has driven very impressive growth over the years, in all types of economic and retail environments.

TJX has proven resilient in this industry thanks to its unique business model. The firm's focus on name brand but highly discounted merchandise appeals to bargain-focused customers who are attracted to its "treasure hunt" experience.

As a result, TJX is more insulated from disruption caused by online shopping and economic downturns.

In retail, same-store sales or "comps", which measure sales from stores open at least a year, is a key metric investors watch to determine a retailer's health. TJX has managed to post positive comps in all but one year in its 40-plus year history, demonstrating the resiliency and long-term appeal of its business concept.

Source: TJX Investor Presentation

TJX's sales and profits have steadily grown over time due to several factors, starting with its supply chain. TJX has over 1,000 purchase associates sourcing products from over 20,000 vendors in more than 100 countries.

When a fashion designer overproduces or other retailers buy too much inventory, TJX's buyers swoop in, negotiate the lowest possible price, and pass the savings on. Many of its rivals do not have access to these vendor sourcing networks, and TJX’s relatively low selling prices make it even harder for new competitors to copy the business and turn a profit.

Besides being able to offer name-brand goods at lower costs than rivals, TJX also provides customers with a constantly changing mix of merchandise. Each of its stores receives several deliveries each week that contain thousands of items.

As long as manufacturers make too much product, vendors want to clear merchandise at the end of a season, and department stores cancel orders, TJX has plenty of opportunity to continue stockpiling its locations with quality products at bargain prices.

TJX's solid balance sheet supports its merchandising strategy, too. The company earns an A+ credit rating from Standard & Poor's and has excellent financial liquidity, giving its vendors a high degree of confidence in the business.

Many of its rivals with weaker finances are forced to buy discounted merchandise (excess inventory from department stores and specialty retailers) on credit and ask for concessions, such as markdown allowances and return privileges in case the discount retailer can't sell the merchandise.

On the other hand, TJX can pay in cash and buy in variable quantities (non-full lot shipments). The company also doesn't have to ask for concessions because of its enormous store base, industry-leading distribution network, and proprietary inventory management system.

In other words, TJX’s massive size and access to capital mean that it is often the best partner for its suppliers to sell to, giving it an edge in sourcing unique, bargain-priced merchandise. The company’s diversified store base can absorb a large amount of various products and turn them over quickly.

However, none of these advantages would be possible without TJX's unique inventory management system. The company has spent decades building an in-house data analysis system to allow it to optimize its inventory and logistics chains. TJX can quickly identify regional tastes and know exactly where to ship its low-cost merchandise with minimal risk of it not selling.

In addition, the stores themselves embrace an open layout design with items displayed on wheeled racks and merchandise bins. Store managers can easily move products around to optimize customer traffic flow and sales, and the lack of permanent fixtures helps keep costs down too.

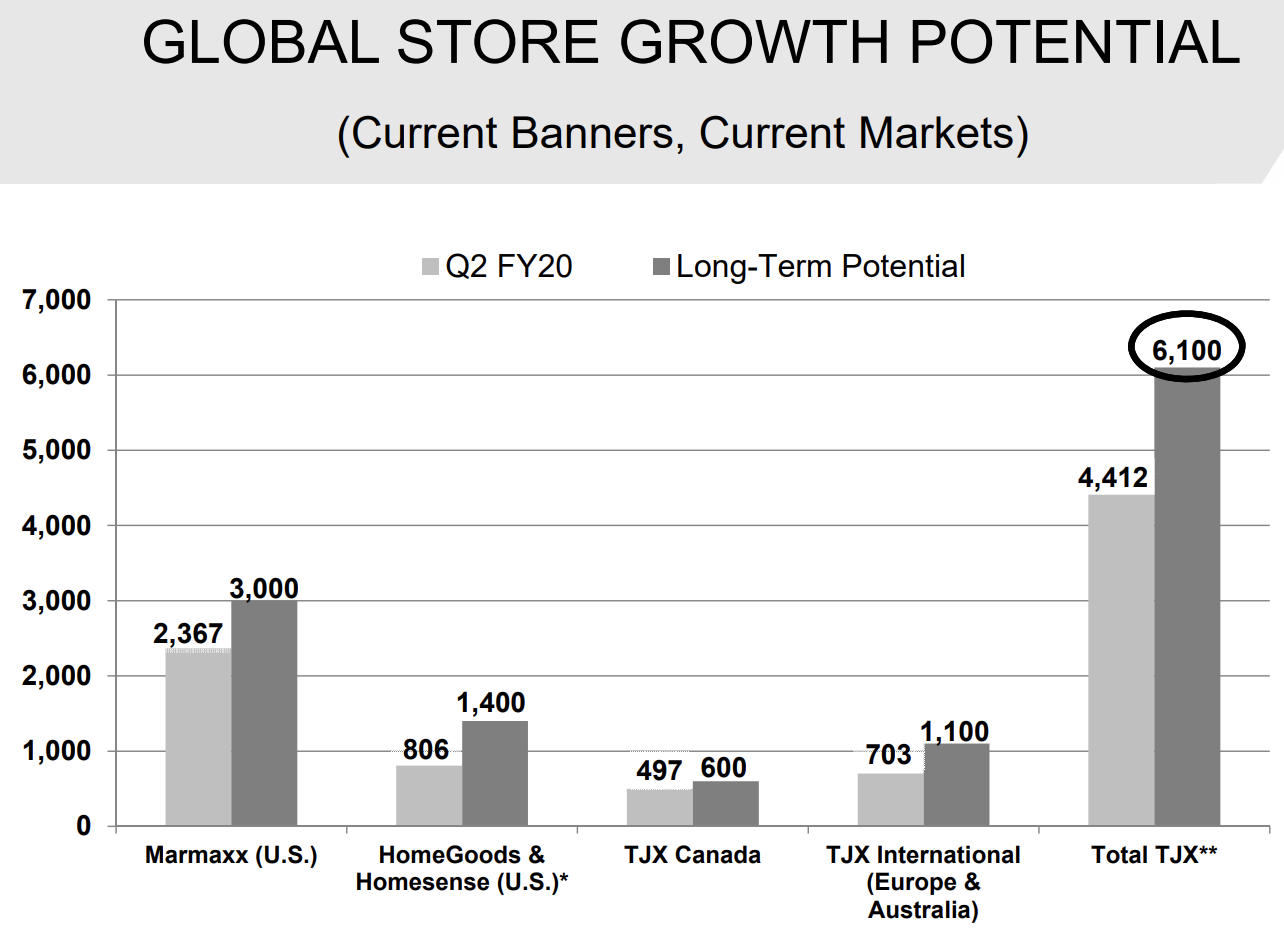

While many brick-and-mortar retailers are struggling in an increasingly digital world, TJX believes its best days are ahead of it. In fact, management expects to eventually increase the company's store count by nearly 50% to 6,100 locations.

Source: TJX Investor Presentation

Overall, TJX has proven that its discount retail business model, combined with solid execution and competitive advantages in supply chain, inventory management, and product pricing, make it one of the best-managed and fastest-growing global retailers.

As importantly, TJX has thus far proven to be largely Amazon-proof while showing an exceptional dedication to large dividend increases that make it an appealing choice for a growth-focused income portfolio.

That being said, TJX, like all retailers, still faces numerous challenges that challenge its long-term expansion plans.

Key Risks

TJX is one of the oldest discount retailers and has long enjoyed the first-mover advantage in the industry.

However, the discount retailer space is getting more crowded with competitors such as Ross Stores (ROST) and Burlington Stores (BURL) opening more of their own off-price locations.

The continued growth of rivals also sourcing excess name-brand merchandise means that TJX could one day find it more challenging to get enough inventory to satisfy customers at an ever-increasing number of global stores.

Fortunately, the company's relationships with more than 20,000 vendors makes supply challenges seem unlikely. The ongoing contraction of full-price department stores such as Macy's and Kohl's likely provides more opportunities, too.

Another risk to consider is that the appeal of TJX's stores, particularly the "treasure hunt" nature of its business, might not always remain popular. Online shopping is increasingly the easiest way for vendors to find customers for excess merchandise and for consumers to find the best prices.

For now, TJX's business model appears to be relatively immune from the rise of e-commerce, since many customers value the experience of physically shopping fast-changing inventory even if it's not as convenient as online bargain hunting.

However, investors can't assume that this will always be the case. After all, Sears (SHLD) was famous as a major disruptor of department stores back in the 19th century when it started as a mail-order catalog company. But times changed, and if a company doesn't adapt, then it can end up being disrupted.

Should the competitive environment intensify, there’s risk that the company’s ambitious expansion plans could be reduced or leave it overstored, which has been an issue for many brick-and-mortar retailers in recent years. If that were to happen, TJX's stock would lose its premium valuation multiple as investors reprice its long-term growth prospects.

In the short term, TJX's results can experience seasonal fluctuations and be sensitive to changing consumer tastes. For example, management won't always pick the right merchandise to buy. This can occasionally result in weak comps growth, although it shouldn't affect TJX's long-term earning power.

Finally, it’s worth noting that TJX has approximately 270,000 employees, many of whom work less than 40 hours per week. Potential changes to minimum wage laws and healthcare regulations could adversely affect the company’s cost structure and earnings growth rate.

Closing Thoughts on TJX Companies

Retail is a tough industry that’s undergoing a lot of disruption thanks to e-commerce. Naturally this makes dividend investors nervous about the safety and growth prospects of many retail stocks.

However, TJX has proven to be one of the most adaptable retailers in the world. The firm's off-price business model and focus on providing an exciting customer shopping experience with fast-moving inventory have thus far proven to make TJX fairly resilient to the rise of online shopping.

When combined with management's impressive operational track record and the firm's potential to grow its store base by nearly 50% over the long term, TJX is likely to provide double-digit dividend growth for the foreseeable future.

TJX's conservatism, financial discipline, and unique merchandise sourcing advantages make it one of the few consumer retailers that conservative dividend growth investors might want to consider.