Reviewing Broadcom's Dividend in Light of CA Deal, Apple's Struggles

Broadcom (AVGO) investors have had plenty to worry about in recent months including:

Broadcom's exposure to the trade war with China, which accounts for nearly 50% of the company's sales

Apple's (AAPL) iPhone slowdown, since the smartphone maker generates 25% of Broadcom's revenue

Broadcom's $18.9 billion acquisition of CA Technologies (CA), which will strain the balance sheet

The broader selloff in the tech sector

Thanks in part to these concerns, which have kept a lid on the chipmaker's stock price, AVGO's dividend yield now sits above 4%, near the highest level in its history. With such an unusually high yield for a tech company, some investors might be wondering about Broadcom's ability to sustain its dividend in the future.

Let's take a closer look at some of the recent events impacting Broadcom and assess whether or not the company's long-term outlook appears to remain intact.

Why Broadcom Has Been So Volatile Lately

Besides the unusually high volatility across the tech sector, there are three primary reasons for Broadcom's choppy performance over the past year. Among the most important issues is the firm's $18.9 billion acquisition of CA Technologies, announced on July 11, 2018.

The majority of mergers fail to create shareholder value, due to integration challenges, overpaying, and the risks that come with taking on a lot of debt to fund a deal. Risk is even higher when the acquiring company buys assets that don't naturally fit with its existing business model, venturing outside of its circle of competence.

The CA merger was announced soon after Broadcom's failed attempt to buy Qualcomm (QCOM) in a deal valued at more than $115 billion. That merger was quashed by the U.S. government in March 2018 over concerns that the company's large percentage of revenue from China (48% in fiscal 2018) might pose a national security risk, especially(in terms of U.S. development of 5G chips.

Broadcom's bid for CA Technologies, which the market may have assumed was a knee-jerk reaction to the Qualcomm merger failure, is also rather unusual for several reasons.

While Broadcom has a long history of growing through M&A (see below), typically management's strategy is to acquire a tech hardware maker with a focus on securing just its top one or two fastest growing businesses. The slower growing, lower margin segments get sold off, and the R&D for those segments gets cut.

Thanks to this strategy, Broadcom has built up strong positions supplying a variety of chips used in smartphones, data centers, routers, and various network and storage equipment.

Source: Broadcom Investor Presentation

CA Technologies, on the other hand, derives most of its revenues and almost all of its profits from software tools used for mainframe computers, a mature industry that's in a gradual secular decline thanks to the continued rise of cloud computing.

That's why after the acquisition (which valued CA at 16 times free cash flow) was announced, RBC Capital Markets analyst Amit Daryanani stated that "lots of explanation is needed" while Summit Insights Group's KinNgai Chan commented that the deal "definitely will create some uneasiness among its current investor base."

Then, in October, the overall semiconductor industry was rocked by worries that slowing global growth, when combined with a potential cyclical peak in industry sales in 2018, might cause disappointing results this year.

What's more, as America's trade war with China continued on with no resolution in sight, investors worried that 2019 earnings declines could be even worse due to both slower global economic growth (made worse by tariffs) and supply chain disruptions.

Fears only escalated when Apple unexpectedly released its first revenue guidance cut in 16 years on January 2, 2019. In the firm's letter to shareholders, Apple's CEO Tim Cook lowered the company's revenue guidance for the holiday quarter by 8%, citing China as the cause for over 100% of the revenue shortfall:

"China’s economy began to slow in the second half of 2018. The government-reported GDP growth during the September quarter was the second lowest in the last 25 years. We believe the economic environment in China has been further impacted by rising trade tensions with the United States.

As the climate of mounting uncertainty weighed on financial markets, the effects appeared to reach consumers as well, with traffic to our retail stores and our channel partners in China declining as the quarter progressed. And market data has shown that the contraction in Greater China’s smartphone market has been particularly sharp." - Tim Cook

The day after that letter was released, most semiconductors (plus Apple) plunged 5% to 10% (Broadcom shares fell about 8%). Not only did this news provide apparent confirmation that the trade war is hurting China's economy (where 48% of Broadcom's sales come from), but also that smartphones, already experiencing far slower growth in recent years (longer upgrade cycles, market saturation), are being hit especially hard.

According to Broadcom's 2018 annual report, 25% of the semiconductor firm's revenues come from Apple, and overall 30% of the company's sales are from smartphone chips. Thus if the smartphone market has a bad year, with Apple, in particular, being hit hard, then Broadcom's 2019 could be worse than what the market's already lowered expectations might anticipate.

With a better understanding of why Broadcom's shares have been so volatile, including their plunge into a bear market last July, let's take a look at whether or not the company's dividend profile remains solid.

Broadcom's Dividend Remains Healthy

On the firm's third-quarter 2018 conference call, Broadcom CEO Hock Tan outlined the company's plans to make CA Technologies (acquisition closed in November) a great deal for investors:

"We are focusing all our attention on renewing existing products with existing mainframe-centric customers, customers that represent virtually all of the world's largest enterprises and largest spenders on information technology...We are also targeting expansion opportunities within this core mainframe customer base...This new business model, we believe, plays to our strengths, focusing on the largest 500 customers tied to mainframeswith the ability to up-sell enterprise software competitively using an all-you-can-eat subscription-based model." CEO Hock Tan

Basically, Broadcom is refocusing CA's core strengths to place more emphasis on better monetizing the firm's existing customer base (many with decades-long relationships with the company) rather than pursuing new customers. Greater focus is on selling more subscription services as well, which management expects will lead to a:

"dramatically more profitable revenue base which is more aligned to the rest of Broadcom and that we expect will grow...The cost of running this renewed and expanded model will be substantially less than the legacy land-at-all-cost model and importantly renewing and expanding plays to CA’s strengths." - CEO Hock Tan

The Wall Street Journal also noted that Broadcom CFO Tom Krause stated in an interview that software was a natural extension for the company when you think about the ecosystem Broadcom plays in. He believes the deal will "help Broadcom expand in a total market for infrastructure technology that amounts to $200 billion, about triple the size of its current opportunity."

In essence, while the shift towards software might be unusual for Broadcom, the overall strategy appears to be in line with what the company has been doing well for decades.

If nothing else, the company's 2019 guidance calling for 18% revenue growth and 14% adjusted EPS growth doesn't signal reason for long-term investors to panic. It's true that this guidance is likely to come down, possibly a lot, now that Apple has disclosed its worse than expected revenue hit.

However, even with Apple accounting for 25% of Broadcom's sales, it's unlikely that the company will face a decline in either revenue or cash flow in 2019. Certainly not enough to put the generous dividend at risk.

It's also important to realize that a big reason why Broadcom's dividend yield is near an all-time high is due to the company's policy of paying out 50% of free cash flow as dividends (the other half used for buybacks and future acquisitions), not because the market is worried the dividend is likely to be cut.

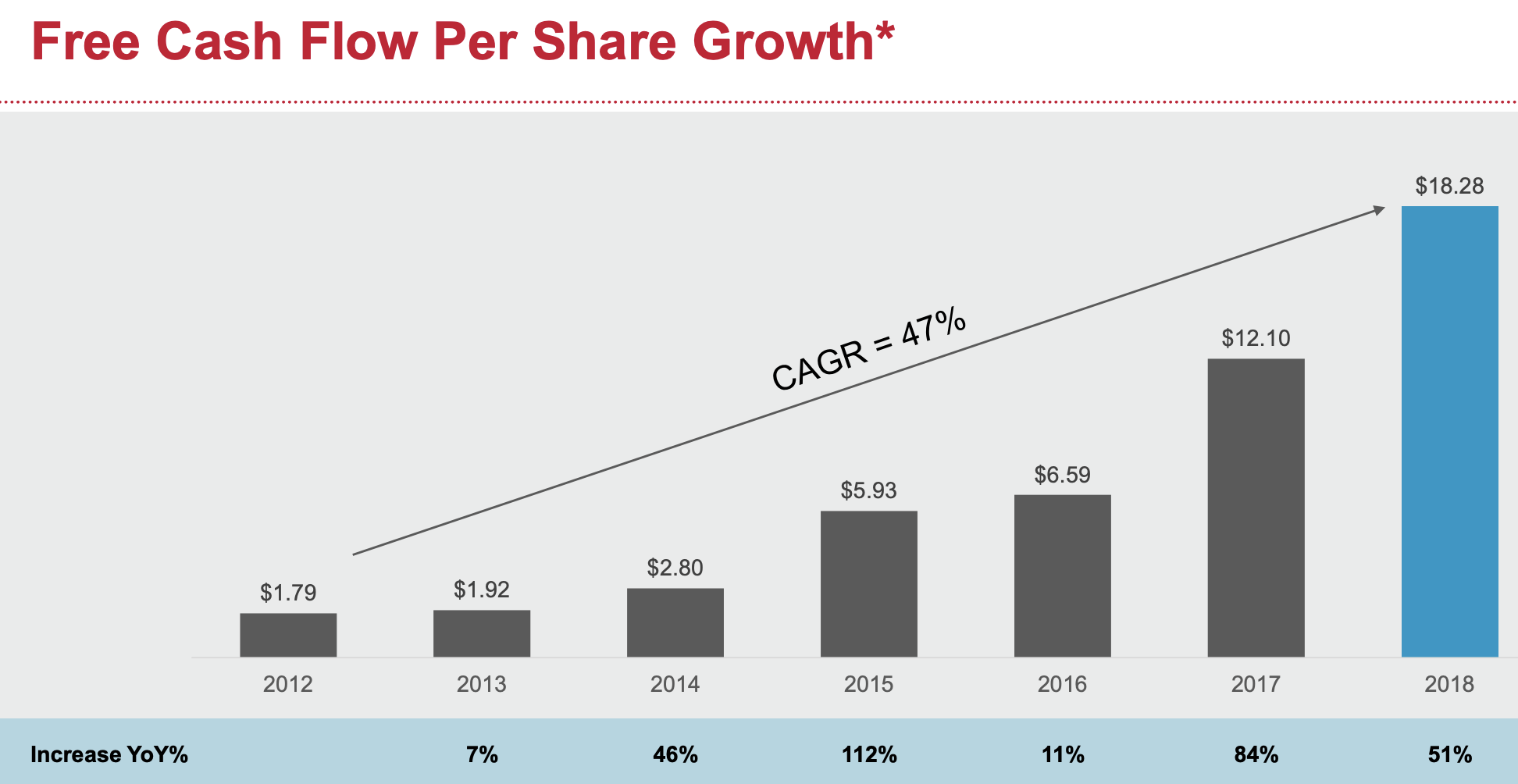

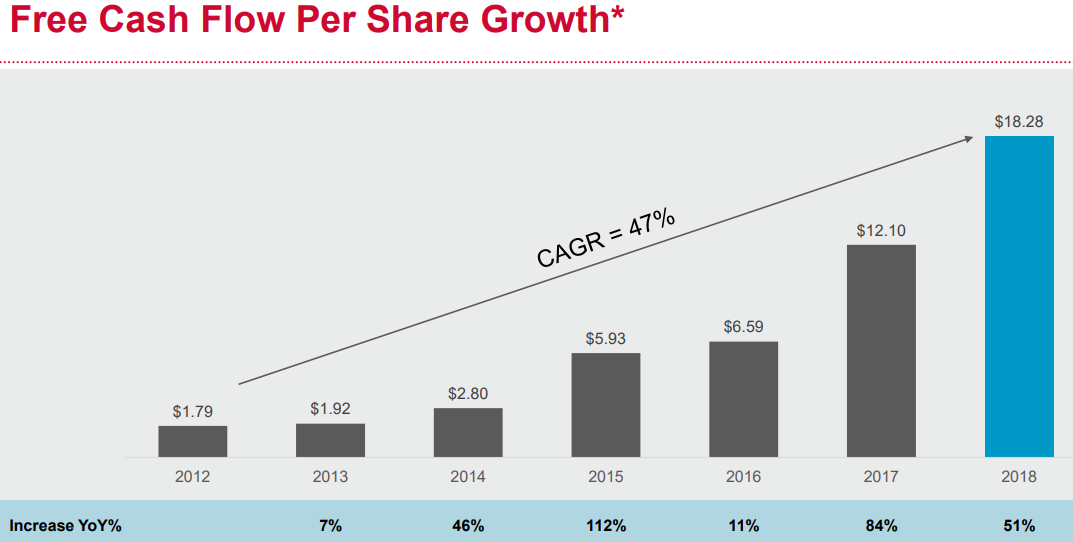

In large part due to aggressive M&A, Broadcom's free cash flow per share has grown at a torrid pace in recent years, and the dividend right along with it. That includes a 51% dividend hike for 2019 (in line with the firm's free cash flow growth last year) announced in December, which is why the stock's yield suddenly spiked so high.

Source: Broadcom Investor Presentation

And according to CFO Tom Krause, unlike some semiconductor makers bracing for a cyclical downturn, Broadcom expects to continue growing its free cash flow at a solid clip for the next few years. In fact, on its last conference call, Broadcom's CFO hinted that cost-cutting at CA Technologies could result in double-digit annual dividend increases for the next few years:

"So when you do that math, you are going to come up with a number that’s north of 20% in terms of potential for dividend growth (for 2019).Now, going forward we will have a couple of other tailwinds that we have benefited from in the past, which is frankly M&A and the accretion that we drive once we are fully integrated and restructured.

And so as Hock has been articulating, when we get to the $2.5 billion-plus of operating profit, that’s going to start to be realized in 2020, into 2021. Absent additional M&A, we would continue to focus not just on the dividend but also the buyback, which would allow us to reduce the share count as well. So I think we have a good setup to continue to be able to drive the dividend well into the double digits over the next several years." - CFO Tom Krause

So not surprisingly, the company's guidance and comments are very bullish (as one would expect from any management team). But what about Apple's surprise revenue guidance cut? Even if you assume a very pessimistic scenario of a 20% volume decline in 2019 iPhone sales, that would only represent a 6% decrease in Broadcom's overall sales for the full year.

In other words, while Broadcom's sales and free cash flow in 2019 will very likely miss management's earlier rosy forecast, they could still grow at close to a double-digit pace. It's also worth mentioning that with the CA deal closed, 20% of Broadcom's sales are now from recurring software services and subscriptions, which is a nice shift away from its past sole reliance on volatile hardware sales.

Source: Broadcom Investor Presentation

And if a trade deal is reached to end the tariff conflict with China, which most analysts and economists expect to happen sometime in 2019, then the company's long-term forecast calling for double-digit dividend growth for several years seems likely to remain intact as well.

What about Broadcom's high amount of debt taken on to buy CA Technologies? Could that threaten the firm's dividend safety?

Broadcom is taking on an additional $18 billion of debt as part of the acquisition, which will increase the company's leverage ratio substantially. Per Moody's, Broadcom's total debt / EBITDA ratio will rise from 2.0 to 3.7. Given management's intentions to return the majority of Broadcom's free cash flow to shareholders and continue pursuing acquisitions, Moody's expects the firm's pace of deleveraging to be gradual.

As a result, Moody's downgraded Broadcom's credit rating from Baa3 to Baa2 (a BBB- rating equivalent). Management intends to maintain an investment grade credit rating, which seems reasonable given Moody's expectations for the firm to generate "organic revenue growth in the low to mid single digits over the next year and improve the EBITDA margin as operating synergies are captured at CA."

Even if Broadcom's free cash flow per share grows at just half the rate its CFO hinted at in the most recent conference call, that would still leave the chipmaker with about $8.5 billion in free cash flow generation in 2019, half of which will be used to fund the dividend.

In other words, Broadcom will retain about $4.25 billion of cash after paying dividends that can be used for buybacks, acquisitions, or debt reduction. Although unlikely, if management wanted to direct all retained cash flow towards deleveraging, Broadcom could pay off all the debt it incurred from the CA acquisition in less than five years. Simply put, despite its generous dividend and increased leverage, Broadcom appears to have solid financial flexibility.

As a result, Moody's expects that within just 12 to 18 months Broadcom's debt / EBITDA ratio will fall into the low threes, and notes it could upgrade the firm's credit rating to Baa2 (BBB equivalent) as soon as leverage falls below three.

Due to its spike in leverage, Broadcom's Dividend Safety Score also decreases from the 80s into the 60s, still a safe level. As the firm deleverages in the years ahead, its score should improve.

With the company generating healthy and growing free cash flow, Broadcom should have little trouble achieving Moody's targets, retaining its investment grade credit rating, improving its dividend safety profile, and continuing to reward shareholders with dividend growth.

Concluding Thoughts on Broadcom

While all stocks can be volatile at times, cyclical semiconductor makers such as Broadcom are notorious for their often violent ups and downs, especially when sentiment sours on tech stocks. For this reason alone, conservative income investors who can't stomach big price swings may prefer to look elsewhere.

Over the past several months, Broadcom's shares have experienced several bumps mainly due to the firm's CA acquisition (execution risk), the overall bear market in the tech sector, and concerns that the U.S.-China trade war might especially hurt semiconductor makers via slower smartphone sales at Apple, Broadcom's largest customer.

While all of these risks pose threats to the company's solid fundamentals, Broadcom's management deserves the benefit of the doubt for now due to the team's impressive track record of pulling off large M&A deals and adapting to short-term challenges. When combined with the firm's investment grade balance sheet and healthy free cash flow generation, Broadcom's dividend seems likely to remain safe and growing.

{kind=link}