Con Edison's Exposure to PG&E Does Not Threaten Its Dividend

Consolidated Edison (ED) was recently downgraded by Bank of America Merrill Lynch on concerns that the firm's renewable energy business could run into trouble given its exposure to troubled utility PG&E (PCG).

With PG&E planning to pursue Chapter 11 bankruptcy by the end of the month due to the liabilities it faces from its role in causing the California wildfires, some analysts believe PG&E may not honor the solar supply contracts it has with Con Edison.

As the financial media tends to do, Bloomberg published a scary headline about this possibility: "PG&E's Woes Have Spread to New York's ConEd, 3,000 Miles Away."

However, once you get into the details of the situation, it's one that dividend investors don't need to worry about. Con Edison's dividend safety profile and long-term outlook should remain unchanged, regardless of what happens with the solar contracts it has with PG&E.

First, understand the scope of Con Edison's overall business. Analysts expect the regulated utility to generate 2019 adjusted EBITDA of approximately $4.2 billion.

Of this total, just $485 million (about 11%) is derived from the firm's Clean Energy Businesses (CEB) segment, which develops, owns, and operates renewable and energy infrastructure projects in North America.

Note that those figures include contributions from Con Edison's $1.6 billionacquisition of Sempra Solar Holdings, which made Con Edison the second largest solar energy producer in North America when the deal closed in December 2018.

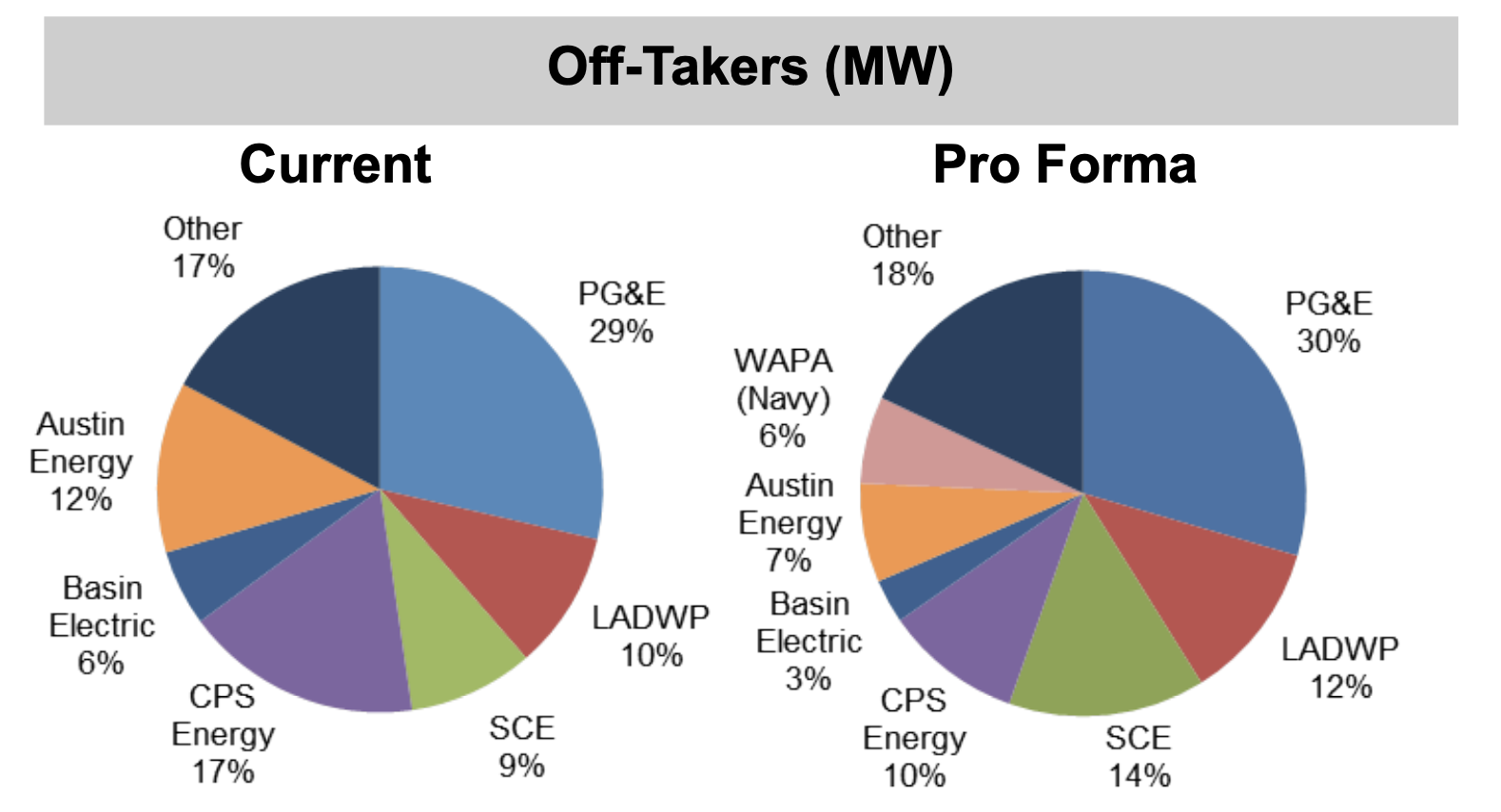

Within the CEB segment, PG&E is the firm's largest customer, consuming approximately 30% of the megawatts that Con Edison's renewables facilities generate.

Source: Consolidated Edison Investor Presentation

What if PG&E decided to reject the off-take agreements it has in place with Con Edison? If we assume PG&E also accounts for 30% of CEB's adjusted EBITDA, approximately $146 million of Con Edison's adjusted EBITDA would be a risk.

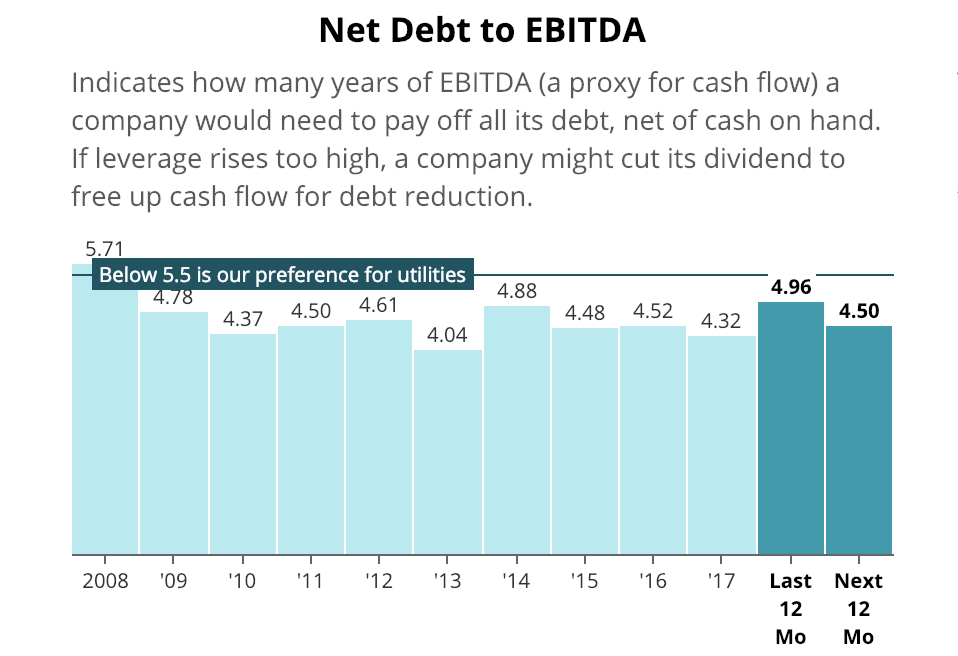

For perspective, that's just 3.5% of expected 2019 company-wide EBITDA. If Con Edison lost this business completely and could not find another utility to arrange a new power purchase agreement with, we estimate the firm's net debt / forward EBITDA ratio would tick up from 4.8 to 5.0, including debt assumed from the Sempra Solar acquisition.

While a leverage ratio near 5.0 would be on the high end of Con Edison's historical range, it's still a healthy level for a stable regulated utility. Con Edison's ability to access low-cost capital and maintain its dividend would remain intact.

Source: Simply Safe Dividends

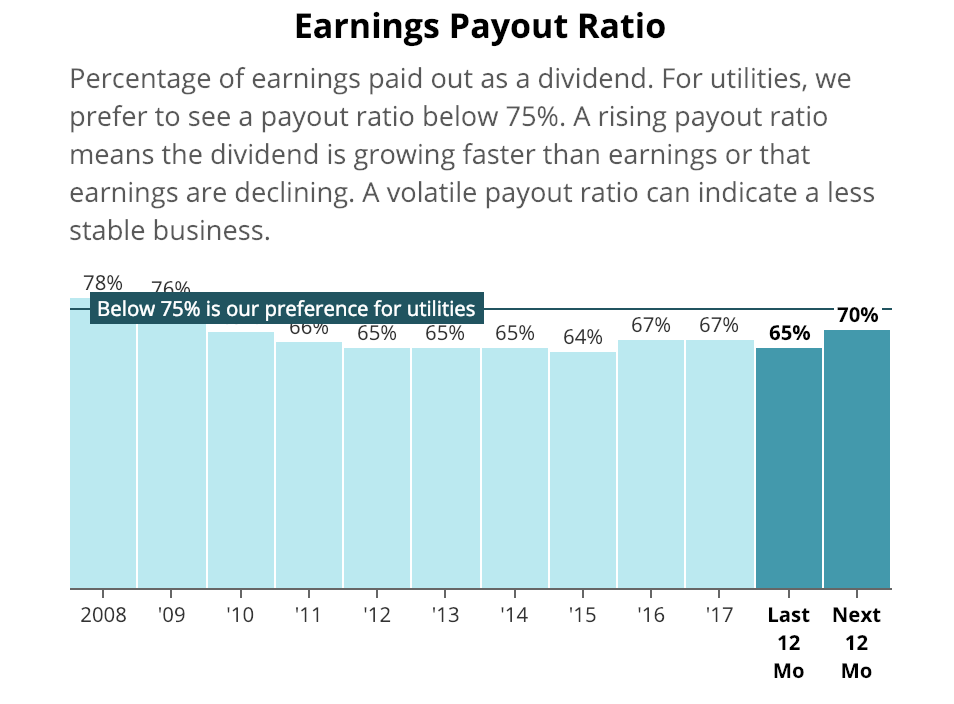

Similarly, Con Edison's dividend would remain covered by the firm's earnings. The utility's payout ratio over the next 12 months is already expected to increase to around 70% or higher "as a result of non-cash earnings impact from its Sempra Solar acquisition," according to management.

Source: Simply Safe Dividends

If PG&E did not honor its contracts, we estimate it's possible that Con Edison's diluted earnings per share could take a hit of around 3% to 5%. To be conservative, if Con Edison's earnings per share unexpectedly declined by 10% in the year ahead, the firm's payout ratio would rise to 78%.

Once again, while high compared to Con Edison's history, this is not an alarming level for regulated utilities. For example, Southern Company (SO), a utility boasting more than 70 consecutive years of uninterrupted dividends, has maintained an average payout ratio above 75% over the past decade.

Perhaps the biggest indicator that PG&E is not a concern for Con Edison's dividend safety or long-term outlook is management's recent action to boost the payout.

On January 17, 2019, the utility announced a 3.5% dividend increase, marking Con Edison's 45th consecutive annual increase for shareholders. That's the longest period of consecutive annual dividend increases of any utility in the S&P 500 index.

While there is always pressure to maintain such a lengthy streak, had PG&E represented a material threat to the firm's financial flexibility, Con Edison's board would likely not have felt comfortable boosting the dividend by much, if at all, until more clarity on the situation was provided later this year.

Discerning news from noise is one of the biggest challenges investors face. In this case, concerns about Con Edison's (limited) exposure to PG&E seem overblown and unlikely to matter for long-term dividend growth investors.