Bank of America Corporation (BAC)

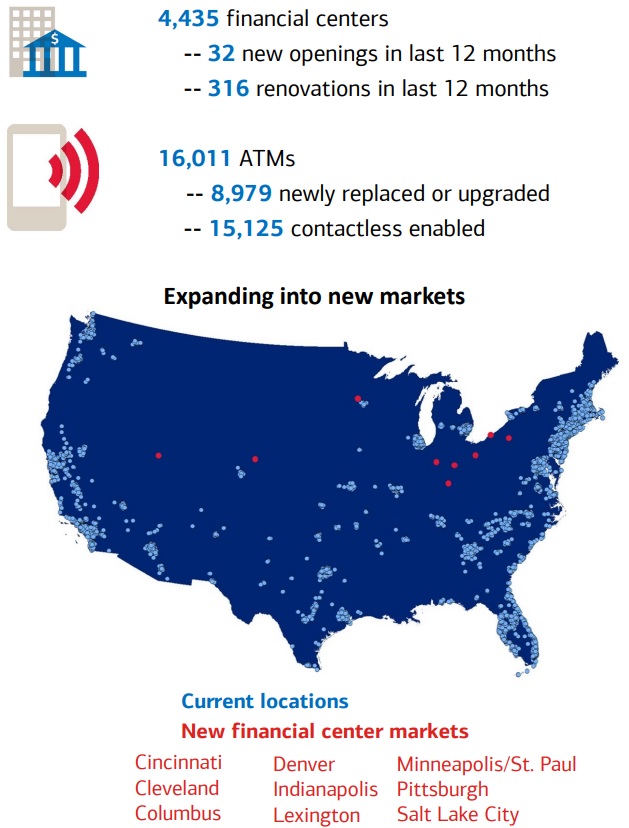

Founded in 1874, Bank of America (BAC), with just over $2.3 trillion in total assets, is the world’s 9th largest bank and the 2nd largest U.S. megabank. The company operates over 4,400 branches in the U.S., as well as more than 16,000 ATMs. In total, Bank of America has 47 million U.S. consumer and business relationships.

Bank of America primarily operates in four main business segments, with the bulk of its income generated from its core consumer and corporate banking divisions:

- Consumer Banking (38% of revenue, 38% of profit): provides retail banking services such as checking, savings, and money market accounts, as well as credit and debit cards.

- Global Wealth & Investment Management (21% of revenue, 14% of profit): wealth management, brokerage, and retirement services. The segment is dominated by the company's US Trust and Merrill Lynch wealth management brands.

- Global Banking (21% of revenue, 28% of profit): commercial, and real estate loans, revolving credit facilities, merger & acquisition consulting, debt, and equity underwriting.

- Global Markets (20% of revenue, 20% of profit): market maker on numerous global exchanges, risk management, securities clearing, settlement, and custodial services, treasury bonds (helps US government sell freshly issued debt), and mortgage backed securities.

Despite its U.S. focus, Bank of America operates in over 35 countries worldwide, mostly through its commercial and capital markets businesses. For example, the bank does business with 79% and 95% of the Forbes Global 500 and Global 1000 companies, respectively.

Business Analysis

Bank of America's turnaround since the financial crisis has been nothing short of impressive. Under former CEO Ken Lewis, the company made two enormous mistakes, specifically acquiring Countrywide Financial (the home mortgage originator) and Merrill Lynch.

These acquisitions, thanks to their exposure to toxic mortgage-based derivatives, ultimately created over $200 billion in losses, compliance costs, and regulatory fines that dogged the bank for years.

However, under current CEO Brian Moynihan, who took the top job in 2010, Bank of America has committed itself to becoming a far simpler and safer bank. In fact, UBS (UBS) analyst Brennan Hawken has said that Bank of America is fast becoming “the most conservative large bank.”

However, under current CEO Brian Moynihan, who took the top job in 2010, Bank of America has committed itself to becoming a far simpler and safer bank. In fact, UBS (UBS) analyst Brennan Hawken has said that Bank of America is fast becoming “the most conservative large bank.”

This development is being driven by a two-part turnaround strategy designed to help the bank maximize its risk-adjusted profit growth in the future. The first part of the turnaround plan has been eliminating the company's most speculative and risky businesses and greatly enhancing the bank's balance sheet.

A strong balance sheet is critically important for any bank, since the nature of fractional reserve banking means that this industry is highly leveraged. Thus loan losses can be magnified during an economic downturn which can wipe out a bank's capital and even threaten its survival.

“The banking business is no favorite of ours. When assets are twenty times equity – a common ratio in this industry – mistakes that involve only a small portion of assets can destroy a major portion of equity…Because leverage of 20:1 magnifies the effects of managerial strengths and weaknesses, we have no interest in purchasing shares of a poorly-managed bank at a “cheap” price. Instead, our only interest is in buying into well-managed banks at fair prices.”

The most important safety metric to look at is the common equity tier 1, or CET1 ratio, which measures the banks common equity (shareholder net assets and retained earnings) against its risk-adjusted assets (loans). Under the new Basel III global banking accords, the fully phased in CET1 ratio is considered the gold standard of bank balance sheet safety.

The U.S. Federal Reserve, which regulates America's banks, has set a minimum CET1 ratio of 8.0% to 9.5% for banks, depending on their size and systemic importance (Bank of America is at the high end of this range). Back in 2010 at the start of the bank's turnaround, the bank's CET1 ratio was just 7.6%, indicating a severely undercapitalized bank.

By the first quarter of 2018 Bank of America's fully phased in CET1 had risen to 11.3% which is far above the minimum regulatory standards. More importantly, the bank's much safer loan book (higher underwriting standards) means that Bank of America likely faces much smaller potential losses during any economic downturn.

This can be seen by the results of the most recent Federal Reserve annual stress test. Their stress test simulates a much more severe global economic recession than the 2008-2009 financial crisis and is designed to test how a bank's balance sheet would fair under extreme conditions including:

- A GDP drop of 6.5% (during the Great Recession GDP dropped 4.2%)

- U.S. unemployment rising to 10%

- Stock market falls 50%

- Residential and commercial real estate prices drop 25% and 35%, respectively

The 2017 stress test resulted in in Bank of America's CET1 ratio dropping to a minimum of 8.9%, far above the regulatory requirement of 4.5%. Even in a severe economic downturn, the company would remain solvent (i.e. not need a bailout) and would likely be able to continue paying its current dividend.

The second part of the company's turnaround came in the form of cost cutting. Since 2008, Bank of America has managed to greatly reduce its expenses through multiple means. For example, the firm reduced its branch count by 28% (from 6,100 to 4,400 locations), slimmed down its workforce by about 75,000 employees, and invested very heavily into digital banking technology.

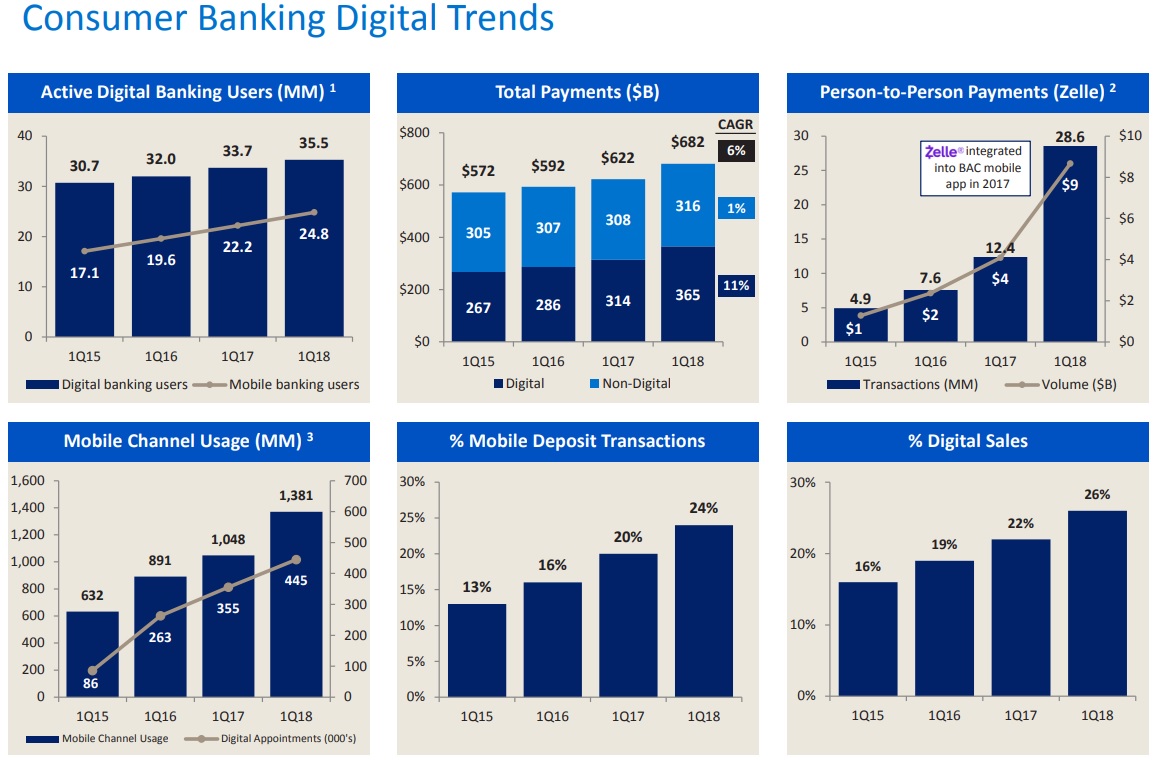

In fact, the bank's total digital user base (business and consumer) has grown over 40% in the last three years. And thanks to its launch of peer-2-peer payments application Zelle in 2017, the company is at the leading edge of shifting consumers from physical banking to digital.

Digital banking helps a bank grow through two ways. First, the more consumers bank online compared to at physical branches, the fewer branches (and their higher fixed costs) a bank needs to maintain, improving profitability.

Next, an integrated digital platform creates higher switching costs, helping a bank retain market share. In the U.S. there are approximately 9,000 banks, and their core offers are highly commoditized. A well-designed digital experience that maximizes convenience can attract customers to a bank, including offers for numerous products such as loans, credit cards, savings accounts, mortgages, and more. That in turn makes customers less likely to leave, allowing banks to minimize the amount of interest they have to pay on deposits.

At their core, banks primarily gather deposits and loan them out for interest income. As borrowers, consumers and businesses are most concerned with getting access to dependable financing at the lowest interest rate possible.

In other words, banks are largely commodity businesses, and the lowest cost operator usually survives the longest in commodity markets. As one of the biggest banks in the country, Bank of America has numerous cost advantages, which begin with its ability to gather low-cost deposits from consumers and businesses that it can lend out at higher interest rates.

For instance, Bank of America has 33% of its approximately $1.3 trillion in deposits in non-interest bearing accounts (such as checking). That helps minimize its borrowing costs and allows it to increase its profitability on loans in a rising interest rate environment.

For example, management says that for every 1% that short-term and long-term rates rise (a parallel shift), it estimates that Bank of America's net interest margin (profits on loans) will increase by $3 billion. That would represent about a 15% increase compared to the bank's trailing 12-month profits of $20 billion.

For example, management says that for every 1% that short-term and long-term rates rise (a parallel shift), it estimates that Bank of America's net interest margin (profits on loans) will increase by $3 billion. That would represent about a 15% increase compared to the bank's trailing 12-month profits of $20 billion.

Meanwhile, the bank's efficiency ratio (operating costs/revenue) has fallen 3% in the past year to 60%. Thanks to ongoing cost cutting efforts and continued growth in digital banking, Morningstar estimates that Bank of America's efficiency ratio will fall to 51% by 2022. For context, the average U.S. bank efficiency ratio was 60% in the past year.

The bank's key profit metrics, specifically return on common equity (ROE) and return on assets (ROA), have continued to rise at an impressive rate as well:

- ROE: up from 8.1% to 10.8% in the past year (8.4% industry average)

- ROA: up from 0.97% to 1.21% in the past year (0.87% industry average)

In the U.S. banking industry, a return on assets of 1% and a return on equity of 10% are generally indicators of a well-run bank. After years of struggling with sub-standard profitability, Bank of America has finally become an above-average bank, both in terms of profitability and conservative and safe lending practices.

Should the bank continue to execute well on its ongoing cost cutting and market share growing efforts, Bank of America should be able to reward investors with strong capital returns, including aggressive buybacks (4% of shares repurchased in the past year) and fast-rising dividends (up 60% in the last year).

However, before buying any bank, investors need to understand the unique risks facing this industry.

Key Risks

While Brian Moynihan's turnaround of Bank of America has been very impressive, there are nonetheless three major risks that investors need to consider.

First, bank stocks are more challenging to analyze than most other types of businesses because it’s hard to understand what is really going on with their balance sheets and financial health, which are the result of numerous subjective accounting assumptions made by management.

First, bank stocks are more challenging to analyze than most other types of businesses because it’s hard to understand what is really going on with their balance sheets and financial health, which are the result of numerous subjective accounting assumptions made by management.

In other words, things usually look fine…until they don’t.

When you think about how a bank makes money, it takes in deposits and lends them out at higher interest rates. To earn an attractive return on equity, banks take on financial leverage to magnify their profit margins.

As long as people and businesses feel safe putting their money with the bank and the bank’s customers continue making their interest and principal repayments on their loans, the bank mints money.

However, banks’ leverage cuts both ways. When delinquencies rise and loans can no longer be paid, a bank’s equity can quickly be wiped out.

To use a simple example, suppose a bank makes a $100 loan to a manufacturing business. To fund the loan, the bank uses $96 of deposits on hand and contributes $4 of its own capital. If the manufacturer is unable to repay its entire loan and only pays $97, the bank’s capital will be hit first instead of depositors’ money. In this case, the bank would see 75% ($3) of its capital wiped out.

If things get really bad, a poorly managed bank that took too much risk can be completely wiped out. This is a simple explanation of what happened during the housing crisis when consumers could not make their mortgage payments and banks had taken on far too much financial leverage and credit risk.

Simply put, all bank revenues and earnings are cyclical by their very nature because they are tied to the health of the economy. In other words, banking profits (and dividend growth) go through boom and bust cycles. That's why very few banks are capable of consistent dividend growth over time, and as we saw in the U.S. banking crisis, sharp dividend cuts are a distinct possibility in the event of a severe financial crisis.

In addition, Bank of America derives a significant portion of its income from asset management and global markets activities, which are highly cyclical and tied to the health of global stock markets, economies, and bond markets. During a downturn, these businesses might be especially hard hit.

Next, many investors are optimistic that bank profits will see strong growth due to rising interest rates. This is an understandable, but potentially incorrect assumption, created by management's interest rate sensitivity guidance such as "a 100 basis point parallel shift in rates will lead to a $3 billion increase in net interest income over a 12 month period". Note that this statement mentions a "parallel shift", meaning that the difference between borrowing and lending costs remains the same.

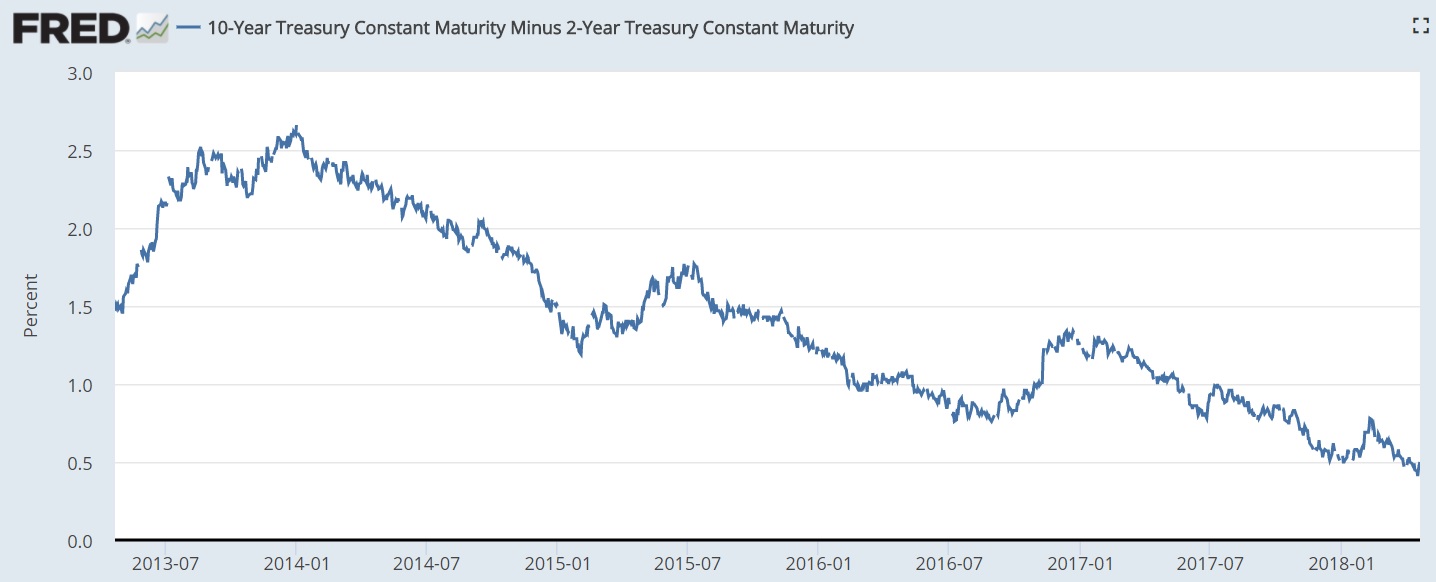

In lending, what matters for profits is not the absolute rate of interest rates but the difference, or spread, between long-term rates (at which companies lend), and short-term rates (at which they borrow). This is known as the yield curve, and the steeper the curve (bigger the difference between long and short-term rates), the greater the potential for financial company profits.

In lending, what matters for profits is not the absolute rate of interest rates but the difference, or spread, between long-term rates (at which companies lend), and short-term rates (at which they borrow). This is known as the yield curve, and the steeper the curve (bigger the difference between long and short-term rates), the greater the potential for financial company profits.

2-Year and 10-Year Treasury Yield Curve

Should short-term rates rise faster than long-term rates, then the yield curve is said to flatten and financial companies can find it harder to lend profitably. In fact, if the curve inverts, or goes negative, then lending profits can actually fall and aggregate credit decreases, which can result in a recession. An inverted yield curve (short-term rates rise above long-term rates) has actually preceded every recession since 1960.

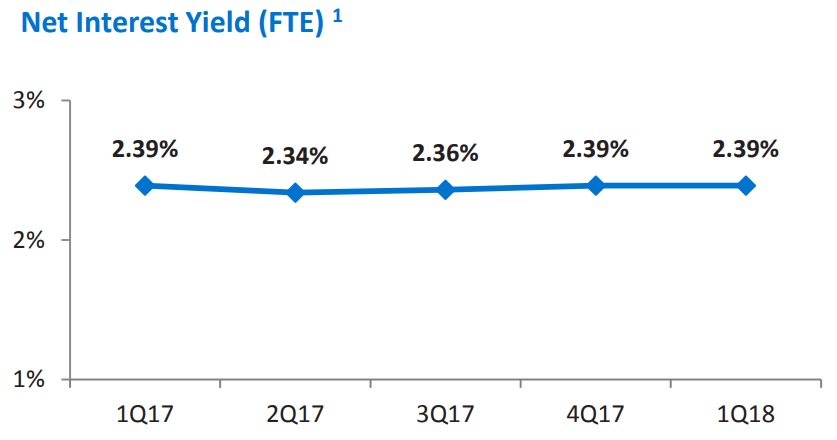

In reality, U.S. banks fund their lending through a variety of short-term rates, including customer deposits that usually have very low interest rates, or none at all (such as checking accounts). This is why large U.S. banks expect a parallel rate shift, in which the yield curve remains unchanged, to result in positive earnings growth; the interest rate they have to pay on deposits is likely to rise slower than both short-term and long-term rates.

However, Bank of America's overall interest costs are rising quickly. For example, in the first quarter of 2017 the bank's average interest on deposits was .78%, but in it rose to 1.13% in the first quarter of 2018. Despite interest rates rising, the bank's net interest margin spread has remained flat for the past year.

Going forward, investors will want to watch to see how Bank of America's net interest margin changes. Increasing competition for consumer deposits in a higher interest rate environment might cause the company to have to increase the interest rates on its interest bearing deposit accounts at a faster pace.

That in turn would increase its borrowing costs and might put pressure on its overall lending profitability, especially as more online-only banks pop up, which have lower operating costs and offer higher savings rates in some instances.

That in turn would increase its borrowing costs and might put pressure on its overall lending profitability, especially as more online-only banks pop up, which have lower operating costs and offer higher savings rates in some instances.

Bank investors also need to remain aware of regulatory risk. U.S. banks, especially strategically important ones, are very highly regulated. In 2018, the Federal Reserve's stress test will become harder, potentially limiting how much capital banks can use for cash returns to shareholders over the next 12 months.

For example, here are the hypothetical scenarios the 2018 stress test will incorporate:

- Unemployment jumps to 10% (unchanged)

- GDP declines by a maximum of 8.9% (instead of 6.5%)

- Stock prices fall 65% (instead of 50%)

- Residential and commercial real estate prices fall 30% and 40%, respectively (instead of 25% and 35%, respectively)

Also remember that a bank's ability to return cash to shareholders via buybacks and rising dividends is regulated by the Federal Reserve, specifically its review of each bank's Comprehensive Capital Analysis and Review, or CCAR. The Federal Reserve approves or rejects a bank's CCAR based on the results of its annual stress test, and the Fed has hinted that it wants a bank's dividend payout ratio to be around 30%.

That level ensures there is a sufficient safety cushion to maximize the chances that a bank's dividend can be maintained during an economic downturn when earnings will decline due to rising loan losses.

That level ensures there is a sufficient safety cushion to maximize the chances that a bank's dividend can be maintained during an economic downturn when earnings will decline due to rising loan losses.

As impressive as America's banking industry turnaround has been, we have yet to see how well it can stand up to a recession. Despite Bank of America's much stronger balance sheet and the optimistic outcomes of its latest stress test, ultimately economic models can only tell us so much.

At some point, the world will experience another recession. Bank of America's "fortress" balance sheet will be tested, and investors will see whether or not its dividend is really safe this time.

Given the Federal Reserve's requirement that banks maintain much more conservative balance sheets, the risk seems to be low. An excerpt from a 2013 interview of Warren Buffett reinforces this point:

At some point, the world will experience another recession. Bank of America's "fortress" balance sheet will be tested, and investors will see whether or not its dividend is really safe this time.

Given the Federal Reserve's requirement that banks maintain much more conservative balance sheets, the risk seems to be low. An excerpt from a 2013 interview of Warren Buffett reinforces this point:

“The banks will not get this country in trouble, I guarantee it. The capital ratios are huge, the excesses on the asset side have been largely cleared out. Our banking system is in the best shape in recent memory.”

Closing Thoughts on Bank of America

Bank of America has done a wonderful job of turning itself around over the past decade. The firm's far more disciplined and conservative banking culture, combined with aggressive cost cutting and investments into digital banking, have caused one of the worst-run banks to become one of the best.

The company has even earned Warren Buffett's stamp of approval. Buffett became involved with Bank of America back in 2011 when he purchased $5 billion of preferred stock and received warrants for shares that Berkshire Hathaway (BRK.B) could exercise over the next 10 years. The firm exercised its warrants during the third quarter of 2017, and Buffett said “Berkshire is going to keep every share for a very long time.”

With that said, U.S. banking is still a highly competitive, cyclical, and complex industry, one that isn't well suited to consistent dividend increases. Investors who are comfortable with those risks and uncertainties are likely best off limiting their position sizes and sticking with industry leaders, which Bank of America appears to be following its turnaround.

All else equal, bank stocks also benefit if long-term interest rates begin to rise, providing some diversification benefits to dividend portfolios that are otherwise heavily dependent on low interest rate beneficiaries such as utilities and real estate investment trusts.

All else equal, bank stocks also benefit if long-term interest rates begin to rise, providing some diversification benefits to dividend portfolios that are otherwise heavily dependent on low interest rate beneficiaries such as utilities and real estate investment trusts.