Wells Fargo (WFC) was founded in 1852 and is the fourth largest bank in the country as measured by assets. The bank ended 2018 with $1.3 trillion in total deposits, and its 90 different business lines collectively generated over $86 billion in revenue from a diversified mix of banking, insurance, investment, mortgage, and consumer and commercial finance services.

Unlike many big banks, Wells Fargo has little exposure to investment banking and trading operations, which tend to be more cyclical and riskier businesses. Instead, the firm focuses on simple lending activities (mortgages, auto loans, commercial financing, etc.) and fee income.

The company has three operating segments:

Community banking (43% of net income): diversified financial products and services for consumers and small businesses including checking and savings accounts, credit and debit cards, and automobile, student, mortgage, home equity, and small business lending.

Wholesale banking (46% of net income): provides financial solutions to businesses across the U.S. and globally with annual sales generally in excess of $5 million. These include Business Banking, Commercial Real Estate, Corporate Banking, Financial Institutions Group, Government and Institutional Banking, Middle Market Banking, Principal Investments, Treasury Management, Wells Fargo Commercial Capital, and Wells Fargo Securities.

Wealth & Investment Management (11% of net income): provides a full range of personalized wealth management, investment, and retirement products and services to clients across U.S.-based businesses including Wells Fargo Advisors, The Private Bank, Abbot Downing, Wells Fargo Institutional Retirement and Trust, and Wells Fargo Asset Management. Services include financial planning, private banking, credit, investment management, and fiduciary services to high-net-worth and ultra-high-net-worth individuals and families.

In 2018 Wells Fargo's loan book of $956 billion was rather evenly divided between commercial and consumer loans. The company serves over 70 million customers through its network of about 8,500 store locations and 13,000 ATMs, as well as its website and mobile banking application.

Wells Fargo has grown its dividend for eight consecutive years. While it was one of just two large banks to remain profitable during the Financial Crisis, the government required all large banks to take part in the bailout which came with the provision of steep dividend cuts.

During the 1990 and 2001 recessions Wells Fargo actually continued to grow its dividend, highlighting how, outside of extreme financial crises, it's been a relatively safe and attractive dividend growth stock.

Business Analysis

Banks primarily gather deposits and loan them out for interest income. As borrowers, consumers, and businesses are most concerned with getting access to dependable financing at the lowest interest rate possible.

In other words, banks are largely commodity businesses, and the lowest-cost operator usually survives the longest in commodity markets. As one of the biggest banks in the country, Wells Fargo enjoys numerous cost advantages, which begin with its track record of gathering low-cost deposits from consumers and businesses that it can lend out at higher interest rates.

According to Wells Fargo’s annual reports, the company’s total deposits have grown from $3.7 billion in 1966 to $1.3 trillion in 2018, representing approximately 12% annual growth over that period. Wells Fargo’s deposits were growing at a healthy mid-to-high single-digit rate in recent years as well, before the Federal Reserve imposed an asset freeze on the bank (see risk section).

The company has some of the largest retail deposits of any bank in the country and ranks among the biggest banks in terms of total deposits. When combined with company's conservative lending practices, which generate a predictable stream of higher-yielding cash flows, it's no surprise that Wells Fargo is famously Warren Buffett's favorite bank.

In fact, Berkshire owns over $20 billion worth of Wells Fargo stock (over 9% of the company), making it one of Buffett's largest equity holdings. And in the past, Charlie Munger, Buffett's right-hand man at Berkshire Hathaway (BRK.B), has called Wells Fargo his favorite company period, against which all others should be measured.

That's thanks to the firm's long-term track record of conservative and trustworthy banking practices, which have allowed it to remain one of the most consistently profitable large U.S. banks, even during periodic industry crises.

For example, during the financial crisis, Wells Fargo's relatively small exposure to toxic mortgage debt and credit default swaps allowed it to not only survive largely unscathed but actually remain profitable. Even at the peak of the crisis, loan losses only amounted to 2.71% of the firm's assets. Only JPMorgan Chase (JPM), which also followed a very conservative banking strategy, was able to match this feat.

Basically, Wells Fargo has chosen to largely ignore faster-growing but more volatile businesses, such as investment banking, in favor of operating like America's largest regional bank. Another benefit to this simpler and less risky business model is that the Federal Reserve, which regulates U.S. banks, has lower capital requirements for Wells Fargo than other strategically important ("too big to fail") banks.

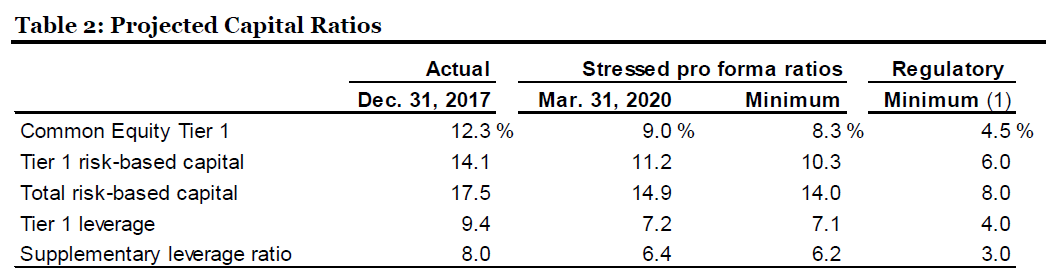

Among the most important signs of Wells Fargo's strong balance sheet (which will protect it during the next recession) are its key capital metrics known as the common equity tier 1 capital, or CET1, and supplementary leverage ratio, or SLR.

CET1 is a bank's net assets (equity), including retained earnings and liquid risk-free assets, divided by its risk-weighted asset base. SLR measures a bank's equity against its entire risk-weighted asset portfolio, including off-balance sheet loans (which blew up many banks during the housing crisis).

The Fed sets minimum capital requirements in accordance with the Basel 3 banking accords designed to ensure that all major U.S. banks have enough capital reserves to be able to survive a severe recession without a bailout, and without failing.

CET1 regulatory minimum: 10.5%

SLR regulatory minimum: 6%

These minimum requirements consist of both a minimum ratio (for all U.S. banks) plus capital conservation buffers and a globally systemically important bank surcharge. In essence, the minimum capital requirements for U.S. banks are now based on how risky regulators feel their total businesses and loan books are.

Most large U.S. banks like JPMorgan and Bank of America have 10.5% CET1 minimum ratios and 6% for SLRs. At the end of 2018 Wells Fargo's capital ratios were very conservative and well above the regulatory minimums:

CET1: 12.4%

SLR: 7.7%

As importantly, Wells Fargo's loans are conservative and unlikely to get the bank into deep trouble up during a recession. The Fed conducts an annual stress test for major banks, simulating a historically "normal" recession as well as a very severe downturn (worse than the Great Recession) to estimate how loan losses will affect a bank's capital ratios during an economic downturn.

The stress test's goal is to make sure that, even at the bottom of a severe recession, a bank's capital ratios don't fall below 4.5% for CET1 and 3% for SLR. Those are levels regulators believe can keep a bank solvent and avoid another bailout.

As you can see below, under even worse conditions than seen in 2007-2009 Wells Fargo's estimated minimum CET 1 ratio was 8.3% and its SLR was 6.2%. That's well above the regulatory minimums and highlights how safe the bank's lending practices are, at least according to the Federal Reserve. This makes the chances of another dividend cut relatively low, even during another financial crisis.

Source: Wells Fargo 2018 Stress Test Results

However, Wells Fargo's industry-leading balance sheet is just one part of the company's long-term investment case. The other two attractions were its ability to achieve some of the top profitability in the industry and grow faster than its peers (but with lower risk).

In terms of profitability, Wells Fargo's giant scale allows it to achieve substantial operational leverage, thanks to some of the lowest cost capital in the industry.

For example, 27% of the bank's massive deposit base (which it lends out) bears no interest at all. This is why the bank's overall interest cost as a percentage of assets is just 0.85%, well below the 3.76% average yield Wells Fargo enjoys on loans funded by its deposit base. Thanks to its cheap funding base, Wells Fargo is virtually guaranteed to generate a positive return on its loan portfolio despite today’s low interest rate environment.

Meanwhile, Wells Fargo was historically able to grow quickly, thanks to industry consolidation over the past few decades. In fact, Wells Fargo now serves about one in three households in the U.S., and its convenience and brand recognition are two reasons why it has enjoyed such strong deposit growth.

The company maintains industry-leading distribution channels, including storefronts, ATMs, online, and mobile, for example. This allows Wells Fargo to serve customers in more locations than any other bank, creating stickier and longer-lasting customer relationships.

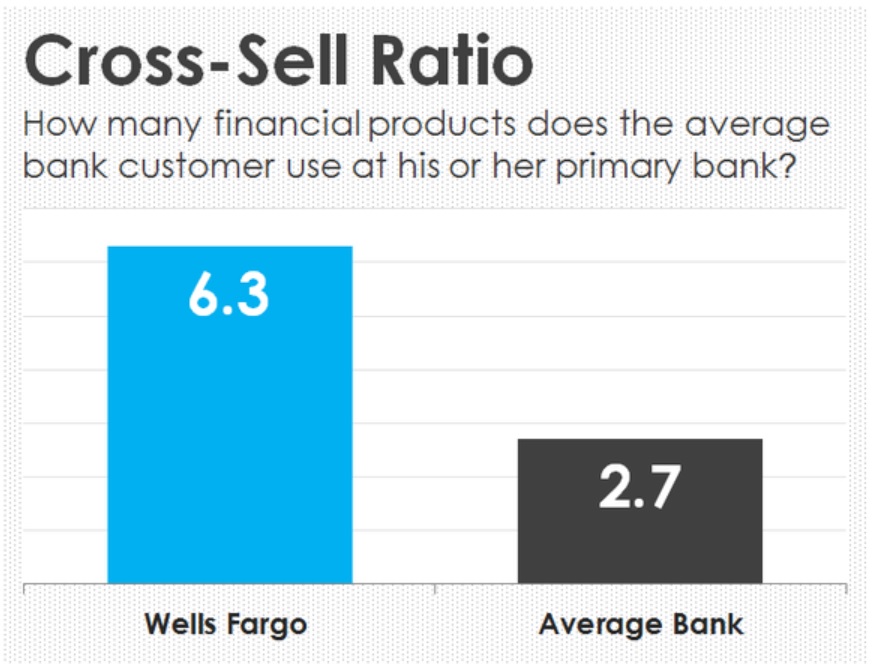

These factors helped the bank become the industry's unquestioned leader in cross-selling numerous products to customers (more on this in a moment), helping it achieve the best returns on equity and assets of any large U.S. bank. The end result was strong earnings and dividend growth, which historically made Wells Fargo one of the best long-term investments in banking.

While the bank is working through many large challenges, it still appears to have a relatively large moat (customers didn't abandon it en masse during its recent scandals). The company gains competitive advantages from its substantial scale, low-cost deposit base, strong capitalization, and leading market share positions.

Despite Wells Fargo's impressive past track record, the bank has recently fallen from grace, and in a big way.

Key Risks

There are numerous risks associated with Wells Fargo, including a few potentially major concerns for the bank's long-term growth prospects.

We need to consider that historically Wells Fargo has grown quickly via two main methods. The first was through aggressive industry consolidation of smaller regional banks, including:

$11.6 billion acquisition of L.A.-based First Interstate Bancorp in 1996.

$31.7 billion merger with Minneapolis, Minnesota-based Northwest Corporation in 1998.

19 small to medium-sized regional banks acquired between 1999 and 2001 (that were hurt during the 2000 recession and tech bubble implosion).

Five acquisitions between 2007 and 2008, including the $15.1 billion purchase of Wachovia, which had just failed due to toxic subprime debt made during the housing bubble.

It's important to realize that going forward, Wells Fargo is very unlikely to receive approval from regulators to make ongoing acquisitions under a much stricter regulatory regime that is more worried about banks being "too big to fail." And that was before the bank's two-plus years of scandals rocked its reputation.

Furthermore, some of these purchases have come back to haunt the company. Specifically, the merger with Northwest saw key top Wells Fargo executives replaced by Northwest ones, most notably Northwest CEO Dick Kovacevich. Mr. Kovacevich took the company's corporate culture down a treacherous path, one that brings us to the next major growth risk for the bank.

Part of what allowed Wells Fargo to grow so quickly while focusing on more traditional and less risky banking businesses, was its historically high cross-sell ratio. This was a policy that had been started by Wells Fargo's previous CEO's but was ramped up to an extreme under former Northwest alumni Kovacevich and John Stumpf.

Specifically, the goal was to make Wells Fargo the best bank at cross-selling its customers numerous services. Having customers take at least several financial products, such as checking and savings accounts, credit cards, personal loans, home equity loans, mortgages, and insurance services, was simply a stickier and more lucrative strategy for the company.

Source: The Motley Fool

In fact, the previous CEO, John Stumpf, famously had a long-term goal exemplified by the corporate motto "8 is great," meaning that he ultimately wanted Wells Fargo to achieve a cross-sell ratio of 8 products per customer.

Under Stumpf,Wells Fargo embarked upon its now-infamous practice of strictly enforcing products sales quotas from its employees, sometimes under the threat of job termination if they failed to meet them.

Employees have described this as a pressure cooker and "boiler room" like work environment that ended up resulting in numerous unethical and even illegal sales practices, including:

110,000 customers were inappropriately charged "mortgage rate lock extension fees" for missing mortgage payments that were actually a result of Wells Fargo's initiated payment processing delays

With that said, the rest of the banking industry isn’t exactly filled with angels either (not that it makes Wells Fargo’s behavior any less despicable). Banks have paid over $200 billion in fines and settlements since 2009. Another article puts the figure even higher.

Wells Fargo was historically the “cleanest” of its big bank brothers, but the ongoing series of scandals resulted in a final settlement (in December 2018) with the U.S. States Attorney's General of $575 million to cover its various misdeeds over the years. The bank has incurred billions of dollars in legal expenses as well.

More troubling for Wells Fargo in the short term is the fact that, in February 2018, outgoing Fed Chairman Janet Yellen took the unprecedented action of barring the bank from growing its asset base until it can prove to the Fed's satisfaction that it can grow safely, without harming customers.

Current Fed Chair Jerome Powell has told Congress that he also views Wells Fargo's actions in recent years as "outrageous" and says the Fed won't lift the asset cap until it's confident the bank's scandals won't be repeated.

Former CEO Tim Sloan, who resigned abruptly in March 2019, had initially said the bank hoped the cap might be removed at the end of 2018. However, the bank know expects the cap to remain in effect for all of 2019. Wells Fargo's earnings and dividend growth rates will be suppressed until the cap is lifted.

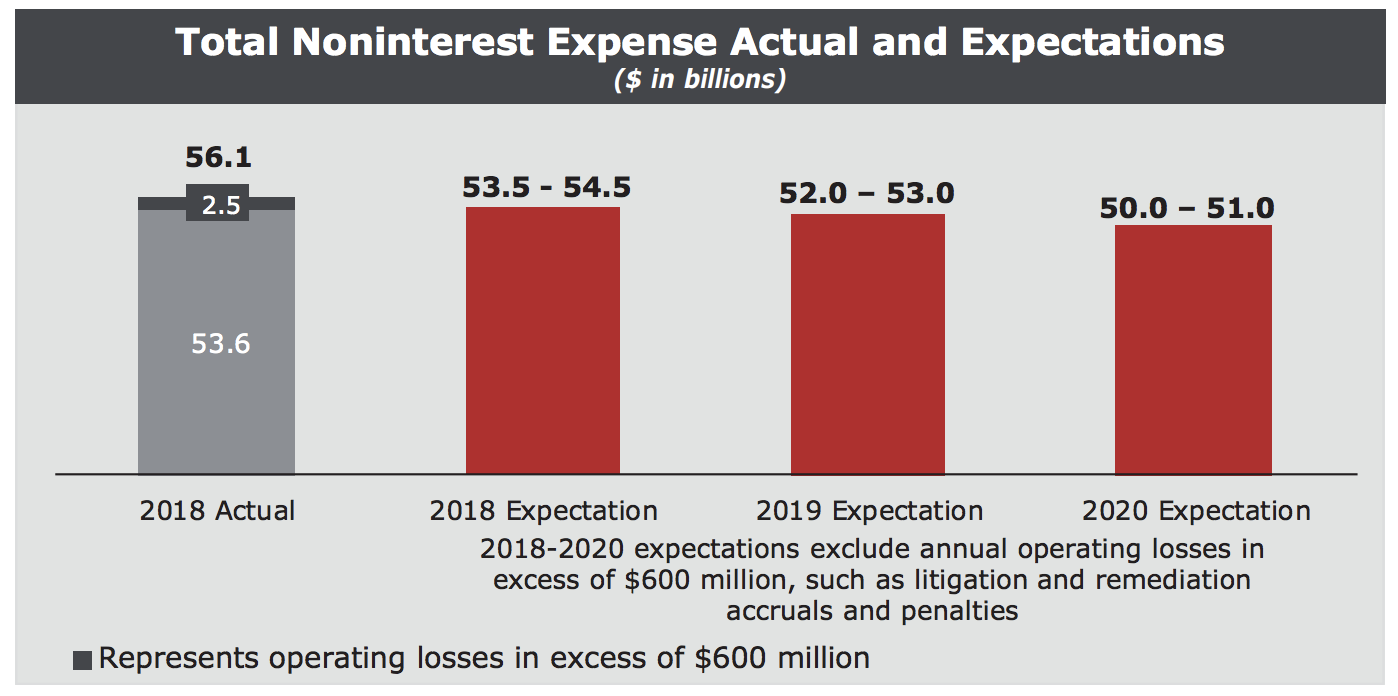

Another challenge Wells Fargo faces deals with its efficiency ratio, which divides a bank's non-interest expenses by its revenue (lower is better). Thanks to a large increase in legal bills, Wells Fargo's efficiency ratio soared in recent years and has only recently started declining.

Management has vowed to slash expenses by a total of about $5.5 billion by the end of 2020 in an effort to reduce Wells Fargo's efficiency ratio from 56.1% in 2018 to its historical norm near 51%. The bank needs to make progress here to demonstrate that its long-term profitability profile remains intact despite the challenges it's facing today.

Source: Wells Fargo Earnings Presentation - Efficiency Ratio

Finally, investors should remember that Wells Fargo operates in an inherently cyclical industry, one whose profits are volatile and rise and fall with the health of the economy. Whenever the next U.S. recession arrives, Wells Fargo's earnings will get hit thanks to a decline in lending demand and a rise in default rates.

But while bank stocks usually underperform in such an environment, their long-term earnings power shouldn't be affected. Importantly, banks are also much better capitalized than they have ever been as a result of new regulations. Here is what Buffett said about banks in a 2013 interview:

“The banks will not get this country in trouble, I guarantee it. The capital ratios are huge, the excesses on the asset side have been largely cleared out. Our banking system is in the best shape in recent memory.”

Fortunately, Wells Fargo's strong balance sheet means the firm's dividend is likely to remain safe during a potential downturn. For now, the big question facing Wells Fargo is whether or not its long-term growth prospects and profitability are permanently impaired thanks to its sales scandal and tighter regulatory oversight. It could take years to have a clearer answer.

Closing Thoughts on Wells Fargo

Wells Fargo was once known for having the industry's best growth, strongest balance sheet, highest profitability, and most conservative management team. However, the asset cap imposed by the Fed due to years of scandals has hamstrung the bank's growth and reputation.

Fortunately, Wells Fargo remains highly profitable and its balance sheet is among the safest of any large banks'. With that said, investors need to realize that many of the problems ailing Wells Fargo, particularly slow growth and tense regulatory relationships, could persist for at least the next couple of years.

Investors need to watch who the company appoints as the next CEO. Bringing in an outsider seems necessary to appease regulators and take bigger steps with the bank's turnaround efforts. However, it could further delay the amount of time it takes Wells Fargo to resolve the various operational and regulatory issues that continue weighing on its short-term growth prospects.

Ultimately, the company seems likely to eventually get its asset cap removed and hopefully put the scandals of the last few years behind it. The dividend should remain safe as well, but investors considering the stock need to have a lot of patience. Investors who would rather deal with less hair and faster dividend growth may consider reviewing JPMorgan Chase and Bank of America as alternatives with more fundamental momentum.

.png)