Clorox: A Quality Dividend Aristocrat With 42 Straight Years of Higher Payouts

Clorox (CLX) started in 1913 when five businessmen invested $100 each to start manufacturing and selling one product, Clorox bleach. Impressively, the company remained a one-product business for its first 56 years.

Today, Clorox boasts a portfolio of well-known brands spanning categories including home care, laundry, charcoal, food, water filtration, cat litter, and more.

Source: Clorox

Clorox generates 34% of its sales from cleaning products, 30% from household products (bags, wraps, charcoal, cat litter, digestive health), and 20% from lifestyle products (food products, personal care, water filtration, dietary supplements).

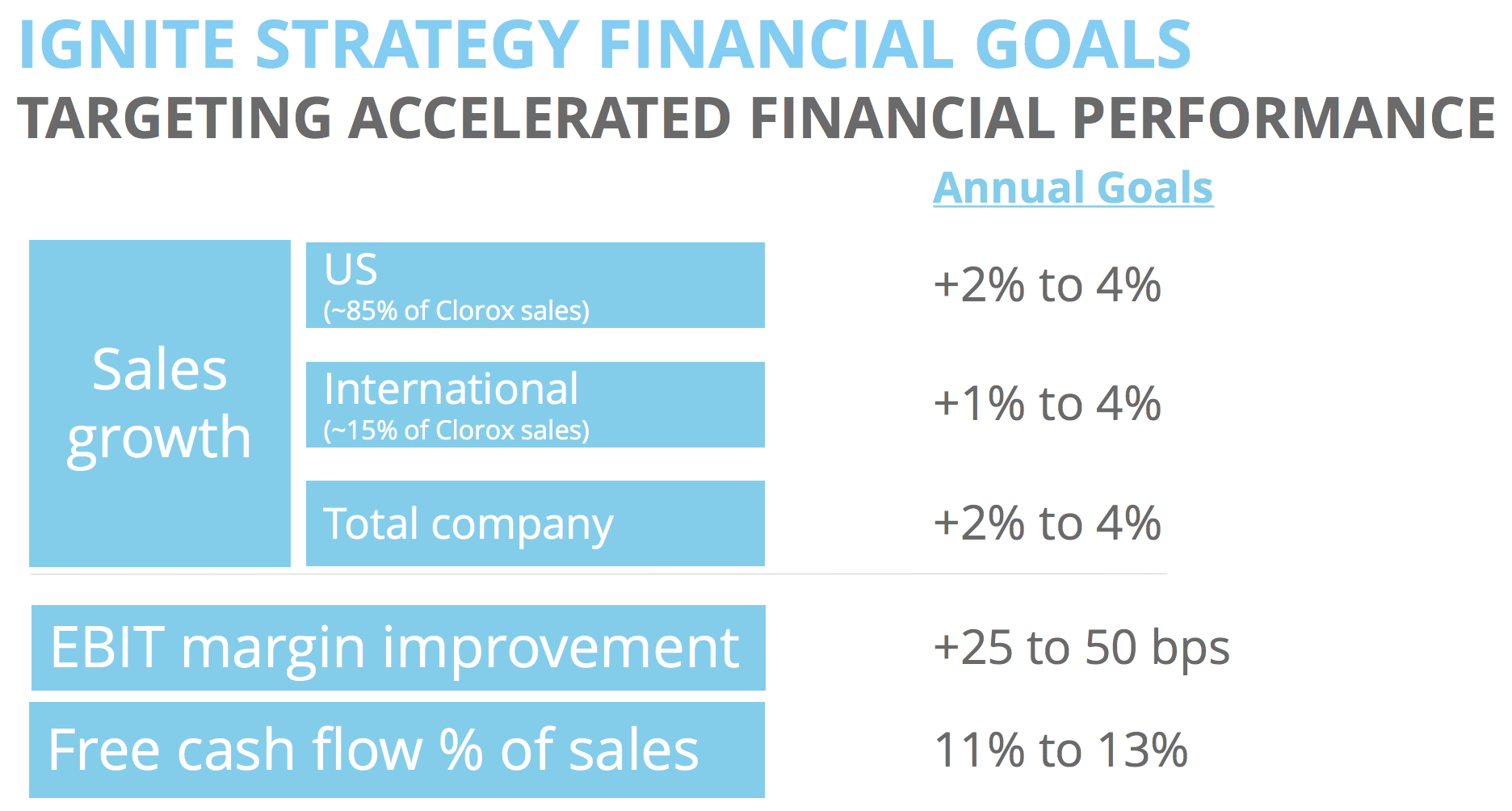

About 85% of sales are from the U.S., with international countries accounting for the remaining 15%. Approximately half of the firm's foreign sales are in fast-growing emerging markets in Latin America.

Clorox has increased its dividend for 42 consecutive years, making it a dividend aristocrat.

Business Analysis As a large consumer products company, Clorox's primary competitive advantages are its strong portfolio of brands, shelf space with retailers, marketing expertise, and product innovation.

With the Clorox brand dating back more than 100 years, Clorox has benefited from being one of the first brands in consumers’ minds for many of its key product categories.

In fact, management estimates that Clorox branded cleaners are found in 90% of U.S. households. When you walk down the aisle of your favorite retailer and see Clorox's household brands, you trust they will deliver quality.

Overall, Clorox has more than 20% market share in its addressable markets and is around three times the size of its next largest branded competitor. The company focuses on attaining large market shares in mid-sized product categories, which helps it avoid going head-to-head as much with giants such as Procter & Gamble.

For example, Clorox dominates in areas that historically larger consumer staples giants didn't prioritize, including bleach, charcoal, disinfecting wipes, water filters, premium trash bags, and toilet bowl cleaners.

This niche focus has helped Clorox become an industry leader around the world with No. 1 or No. 2 market share products accounting for nearly 80% of its sales.

Source: Clorox Investor Presentation

The non-food consumer products space also tends to be sticky and less subject to change. According to IRI Market Advantage, 85% of American household needs are consistently filled with the same 150 items, and 60% to 80% of new product launches fail.

In other words, Clorox maintains a durable and sticky market position, and new entrants tend to struggle to win over consumers who are happy with incumbents’ offerings.

However, to ensure it stays relevant, the company is constantly conducting consumer research to help it launch innovative products and sharpen its marketing campaigns. Clorox routinely invests around 12% of sales back into advertising and new product development, or about $700 million annually.

While many large consumer products companies have struggled with growth in recent years, Clorox's product innovation has historically delivered 2-3% incremental sales growth annually, according to management.

Clorox's global distribution networks are another strength. Clorox can expand the types of products sold under its brands or acquire new brands and sell them throughout the world very efficiently. In contrast, upstart rivals typically can't afford the slotting fees that retailers charge to try out or maintain new products.

More distribution is moving to online channels, making it easier for new brands to reach consumers, but Clorox is investing heavily here as well to keep its brands relevant. In fact, nearly 10% of the company's revenue is from e-commerce.

Looking ahead, the company expects to grow its sales by 2% to 4% per year and improve operating (EBIT) margins by 25 to 50 basis points annually. If successful, Clorox's dividend has potential to grow by at least a mid-single digit pace.

Source: Clorox Investor Presentation

With strong brands, extensive distribution channels, relevant marketing campaigns, leading market share positions, and large and fragmented markets, Clorox should remain relevant for years to come.

That being said, like any company, Clorox faces several risks that could make it challenging for management to achieve the firm's long-term growth objectives.

Traditional brands are being tested more than ever before to maintain their perception as superior products with justifiably higher prices. Previously loyal customers have shown an increased willingness to try other products.

On the retailer side, Costco is perhaps the most notorious example. Its private label Kirkland Signature brand generates about $40 billion in annual revenue, nearly seven times as much business as all of Clorox's brands combined.

If Clorox is unable to differentiate its brands with the right mix of product innovation, marketing, and distribution, then the firm's margins and growth could come under pressure. Especially as major retail customers such as Walmart sell more of their own store-brand goods and push back on Clorox's price increases.

Clorox believes that two thirds of its product portfolio enjoys stable or growing household penetration, suggesting its brands continue performing well overall. However, this is the most important risk for investors to monitor going forward.

Besides dealing with shifting consumer preferences and purchasing habits, Clorox could face challenges identifying additional mid-sized product markets that it can dominate, reducing its long-term growth potential.

After all, the consumer-packaged-goods industry is a fairly mature market. Taking share isn't easy, and finding attractive acquisition targets at reasonable prices is equally taxing.

With low growth rates, large incumbents can quickly find themselves treading water – some brands are growing, others are shrinking. This is what P&G struggled with for years until more recently.

While Clorox is much smaller than P&G ($6 billion in sales versus nearly $70 billion), it’s possible that some of its larger product categories eventually find themselves in similar situations, especially considering the company’s concentration in the slower-growing U.S. market (85% of revenue).

For now, Clorox is holding its ground fairly well. The company continues putting up low-single digit sales growth across its portfolio and has done a nice job expanding into adjacent product categories and geographies while delivering effective marketing campaigns.

However, investors need to realize that this business seems unlikely to grow its earnings and dividend at much more than a mid-single digit pace over the long term.

Closing Thoughts on Clorox Few companies have been as reliable as Clorox. The business generates excellent free cash flow, sells recession-resistant products, and has reliably increased its dividend every year since 1977.

Thanks to management's continuous investments in advertising, R&D, and strategic bolt-on acquisitions, Clorox's brands have withstood the test of time and seem likely to remain core household purchases for many years to come.

While private label, relations with large retailers, shifting consumer preferences, and mature product categories will always remain threats, there isn’t much to dislike about Clorox's fundamentals. The company represents one of the best-managed names in the consumer products industry.