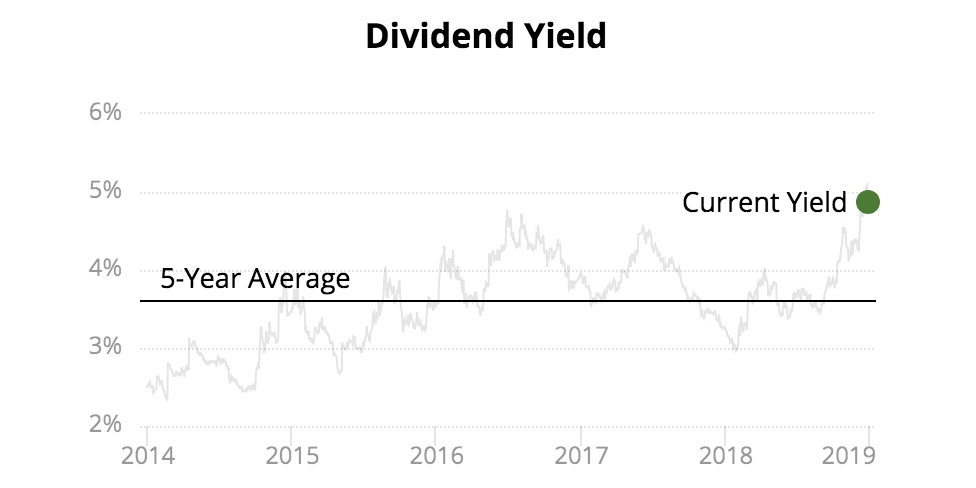

Shares of LyondellBasell (LYB) have slumped nearly 30% since late August, performing much worse than the S&P 500's loss of 14%. The stock's dividend yield now sits near 5%, its highest level since Lyondell began paying dividends in 2011.

Source: Simply Safe Dividends

With analysts projecting a double-digit earnings decline in the year ahead, the price of oil plunging again, and management open to making a large acquisition, let's take a closer look at Lyondell's dividend safety.

Drivers Behind Lyondell's Weakness Lyondell is one of the largest commodity chemicals and polymer manufacturers in the world. The company's products are used in a wide variety of consumer and industrial goods, including plastics and foam found in electronics, cars, construction materials, and agriculture products.

Demand in many of these end markets is sensitive to the health of the global economy. The market's selloff in recent months has at least partially been driven by increased concerns over a slowdown in economic growth, and cyclical company's such as Lyondell tend to perform poorly in these environments.

Furthermore, Lyondell's profitability is very sensitive to the prices of oil and natural gas. Natural gas (power source) and natural gas liquids such as ethane (feedstock) are core petrochemical inputs for Lyondell's domestic operations, which have benefited from the U.S. shale boom.

To demonstrate how sensitive the business is to these critical inputs, Lyondell estimates that its company-wide EBITDA would change by $380 million (a 5% move) due to a 20-cent change in the price per gallon for ethane, which tends to be highly volatile and traded around 40 cents per gallon this summer.

Meanwhile, the price of petrochemicals such as ethylene and propylene is often tied to the global price of oil, which is a key feedstock used by many international rivals who have a higher cost of production compared to their American counterparts.

Simply put, Lyondell benefits the most when the price of oil is high (maximizing selling prices in export markets) and the price of natural gas is low (minimizing input costs).

Unfortunately, crude oil prices plunged from $85 per barrel in early October to about $53 per barrel today, reducing the selling price of many of Lyondell's products. Natural gas prices also spiked from $3.30 MMbtu (million British thermal units) in October to more than $4.60 in November before settling back near $3.10 most recently.

As a result, the profitability of Lyondell's largest segment, Olefins & Polyolefins Americas, which accounted for 42% of EBITDA in 2017, could be squeezed.

No one can predict where the natural gas-oil price spread will go, especially over the short term. However, thanks to the company's strong manufacturing presence in the cost-advantaged U.S., Lyondell's operations seem likely to remain a solid cash flow generator in the long term.

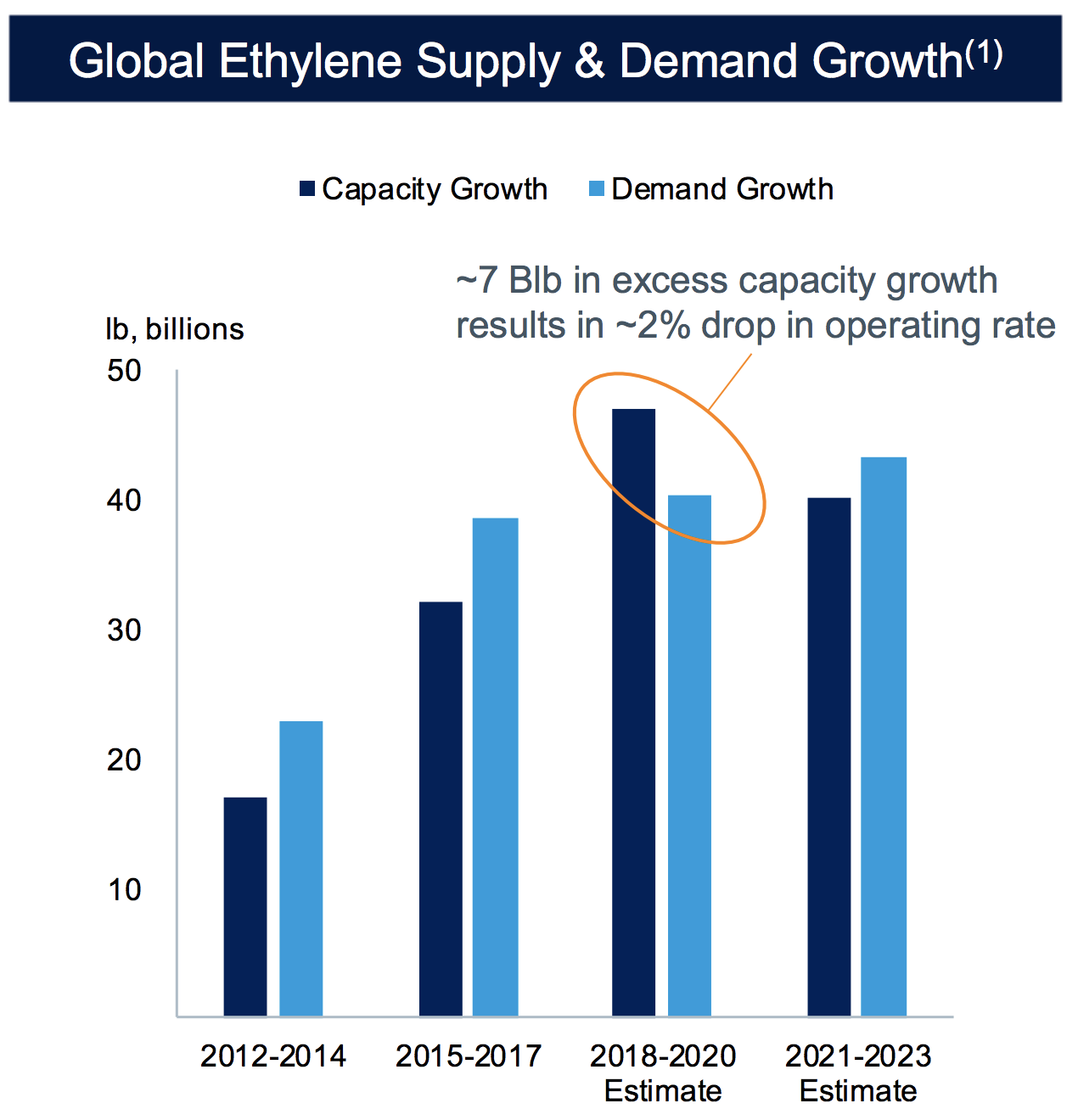

But investors' worries extend beyond recent volatility in energy markets. Lyondell has benefited from high capacity utilization rates for years as demand for its chemicals and polymers grew faster than industry supply.

Unfortunately, that dynamic is now expected to reverse for the next few years. As seen below, large rivals such as DowDuPont and Shell are adding capacity to take advantage of tight operating conditions.

As a result, ethylene capacity growth is expected to outpace demand growth, which will result in margin pressure over the next couple of years. Pressure could be more pronounced if the economy takes a step back during this time.

Source: Lyondell Investor Presentation

The good news is that this incremental capacity will be absorbed over time as the world's demand for plastic continues growing, especially in developing economies such as China.

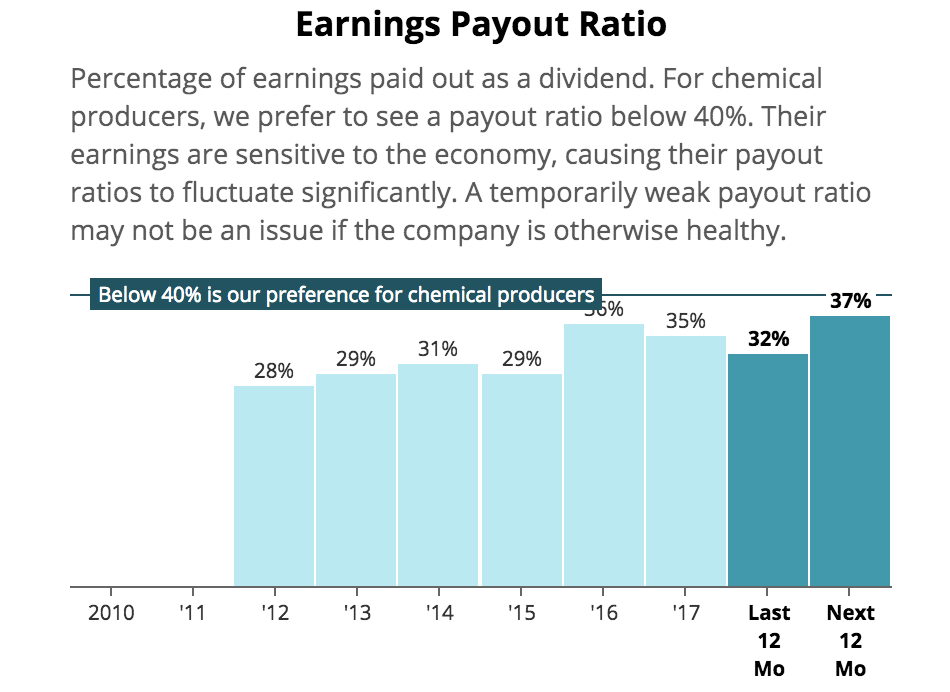

Furthermore, while Lyondell's earnings are expected to decline by 12% over the next year, you can see that the company's payout ratio remains healthy and below our preferred level of 40% for chemical manufacturers.

Source: Simply Safe Dividends

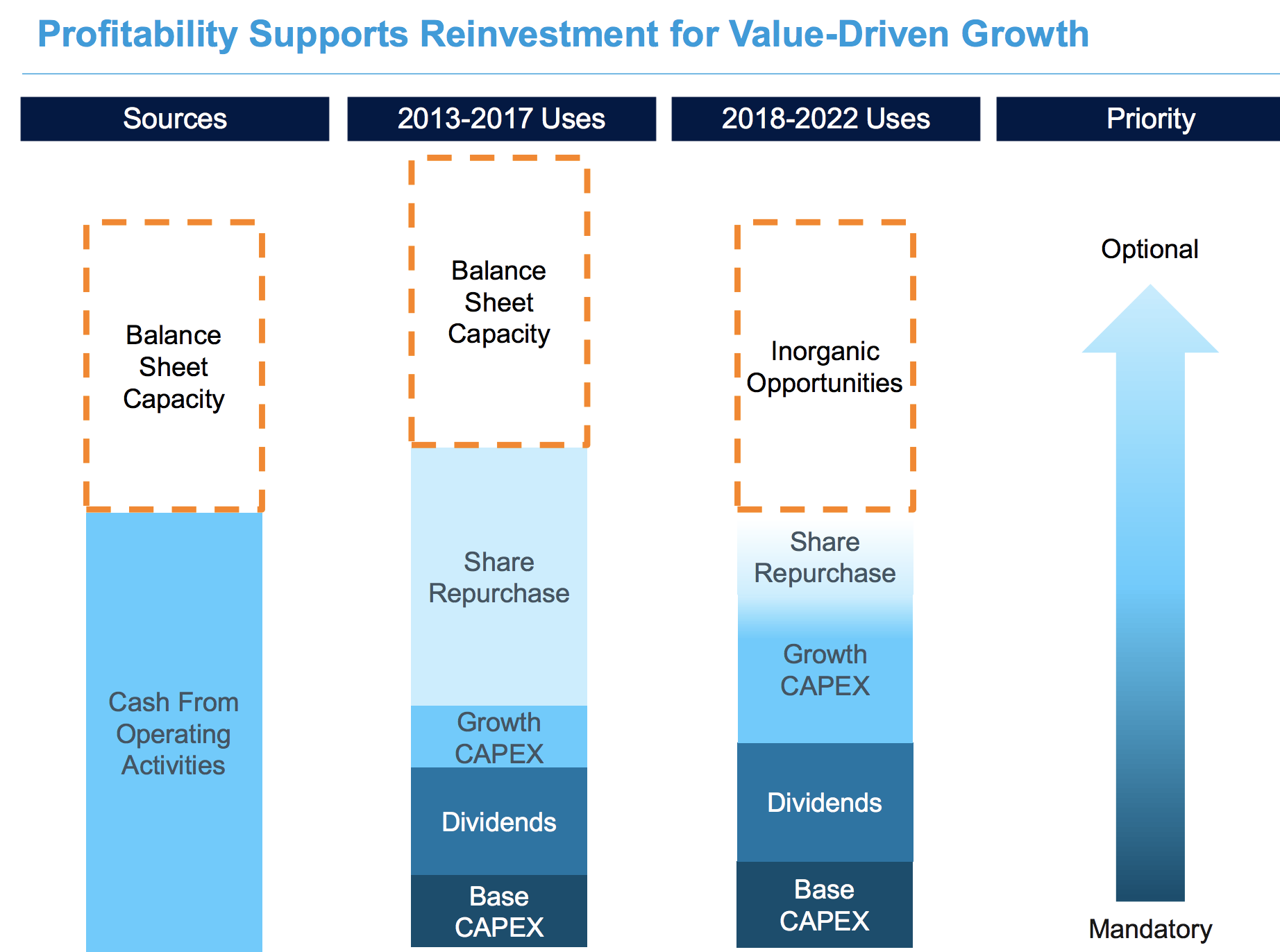

Even if demand were to drop more than expected, Lyondell's dividend appears to have a reasonable margin of safety. The firm's capital expenditure needs to maintain its business are also quite modest and well covered by the chemical maker's cash flow from operations, providing nice financial flexibility. Management's capital allocation plans remain largely unchanged for the years ahead.

Source: Lyondell Investor Presentation

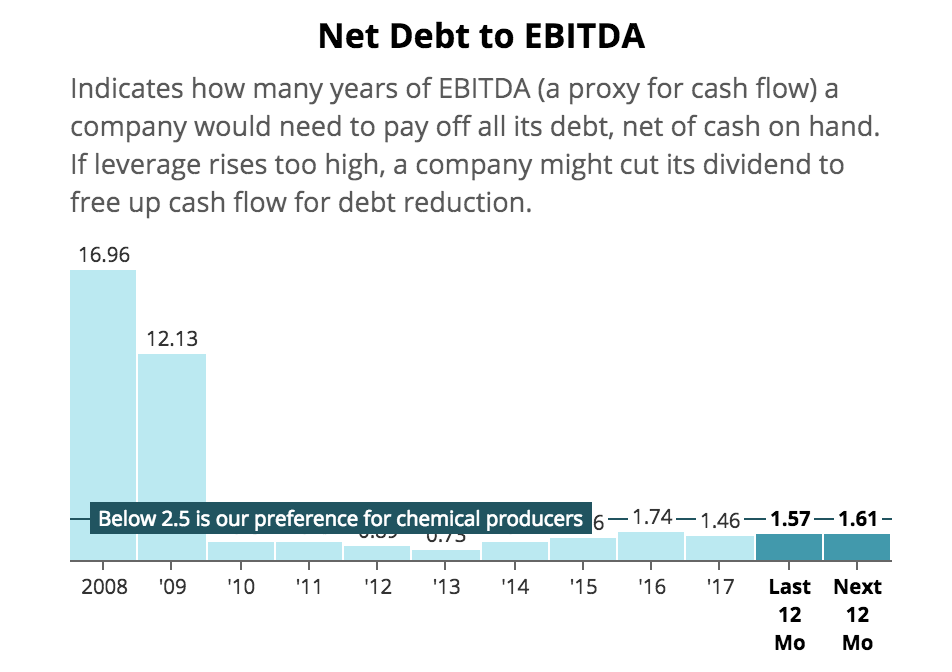

Importantly, management has taken a conservative approach to debt, earning Lyondell a solid BBB+ credit rating from Standard & Poor's. Following the financial crisis, which forced the company into bankruptcy due to the high amount of debt Bassell took on in 2007 to acquire Lyondell Chemical for $20 billion, the firm significantly improved its balance sheet.

Lyondell's leverage ratio remains quite conservative, again providing flexibility in the event the economy were to slow. The firm also had $5.3 billion in liquidity at the end of the third quarter, more than three times the amount of its annual dividend commitment ($1.6 billion).

Source: Simply Safe Dividends

Simply put, based on the information we know today, Lyondell's dividend appears to remain on solid ground, even after accounting for less favorable operating conditions as demand growth potentially slows and new industry capacity comes online.

With that said, investors should be aware that Lyondell is considering making an offer to acquire a majority stake in Braskem (BAK), a Brazilian petrochemical business. Braskem's product lines are similar to Lyondell's, with the main difference being its geographic footprint.

Specifically, 29 of Braskem's 40 plants are in Brazil, so if this deal were to occur, Lyondell would gain more exposure to faster-growing emerging markets.

Braskem is not a small business by any means. Including debt, a deal for Braskem could likely top $20 billion. For comparison's sake, Lyondell's market cap is just north of $30 billion today.

A deal this large would add complexities to Lyondell's business and increase its financial risk profile. If Lyondell acquired all of Braskem with cash and debt, we estimate the combined company's net debt to EBITDA ratio would increase to around 2.6, slightly about the level we like to see for chemical producers but still manageable.

However, if the global economy entered a recession shortly after the deal, putting even more pressure on the ethylene market after new supply entered the market, Lyondell would face greater pressure due to its leverage.

But with both Lyondell and Braskem committed to maintaining investment grade credit ratings and still generating solid cash flow, it seems unlikely that the dividend would be cut.

With all that said, an acquisition of Braskem is far from a sure thing at this stage. Braskem is primarily owned by Odebrecth, a construction business which holds over half of the voting shares, and state oil firm Petrobras. It's hard to say how much of the business they would be willing to part with, and at what price and deal structure (cash versus equity, etc.).

For now, Lyondell's management deserves the benefit of the doubt. It seems very unlikely they would make a move that could ultimately jeopardize the dividend. We will continue monitoring the situation to reassess the firm's dividend safety profile in case a formal deal emerges.

Overall, Lyondell's share price weakness in recent months appears to be driven by concerns over a potentially peaking commodity cycle, the fall in oil prices, fears about economic growth slowing, and perhaps uncertainties caused by management's interest in buying Braskem.

These issues do not appear to threaten Lyondell's dividend safety, thanks largely to the firm's conservative management team and solid financial health. Investors who can stomach some volatility and are comfortable with these uncertainties could consider giving Lyondell a closer look. Either way, the concluding remarks from our April 2018 thesis remain valid today:

Conservative income investors are usually best off avoiding almost all commodity companies, especially those with big debt loads, capital-intensive operations, and a high dependence on uncontrollable macro factors.

However, even despite its bankruptcy in 2009, LyondellBasell looks like an interesting dividend growth stock to pay attention to. The company's exposure to low-cost natural gas in the U.S., the efficiency of its assets, its healthy balance sheet, the shareholder-friendly management team, and the secular growth of the petrochemicals industry over the coming decades are all attractive qualities.

However, investors interested in the stock must remain aware that earnings and dividend growth could slow in the years ahead as new industry supply enters the market, challenging today’s tight operating rates and favorable margins.

If demand were to unexpectedly slow or the oil-gas spread contracted during this time, the stock could really get hammered (and perhaps become really interesting for value-focused income investors).

All things considered, LyondellBasell could be an appealing candidate to consider in the cyclical materials and industrials sectors as part of a well-diversified dividend growth portfolio. Investors just need to respect the company's volatility and sensitivity to factors outside of its control, sizing their positions accordingly.