Compass Minerals (CMP) has been in business for more than 170 years and has increased its dividend each year since it began making payouts in 2004.

Despite its appealing long-term track record, and the recession-resistant nature of its salt and fertilizer businesses, CMP's stock price has slumped over 50% since reaching an all-time high in 2014.

As a result, the stock's dividend yield sits near 7%, its highest ever level. Management has kept the dividend frozen since March 2017, and many investors are wondering if a big cut could be around the corner.

Compass Minerals has had an "Unsafe" Dividend Safety Score for more than a year, so let's take a closer look at the factors weighing on the stock to understand if the firm's dividend could find itself on the chopping block in the near future. Why Compass Minerals is Struggling Compass Minerals' impressive dividend track record was built around the company's ownership of the largest and lowest cost salt mine in the world (Goderich mine in Ontario), as well as an extensive logistics network that gave it logistical advantages in its core Midwest region. But road salt, which used to account for 80% of the firm's revenue in 2015, is a slow-growing business (volume growth of about 1% per year over time).

In 2013, Fran Malecha joined Compass Minerals as its CEO. Malecha had spent 13 years at Viterra, a global agribusiness company, and decided to launch Compass Minerals company on an ambitious growth plan composed of two strategies.

The first was diversifying away from salt and into plant nutrition, reducing some of the firm's dependence on cold winter weather. This was achieved primarily through the large acquisition of Produquímica, a Brazilian specialty plant nutrition and chemical company. The company also bought Wolf Trax, a micronutrients supplier, that same year.

Malecha's other big growth initiative was a four-year, $500 million investment program. This included expanding its potash business (fertilizer), which benefited some of the lowest production costs in the industry. The plan also included spending $225 million to improve its mining capacity (which was expected to lower operating costs 25%) with a specific focus on its Goderich facility.

While the company's diversification strategy has technically worked, with de-icing salt now accounting for only about 60% of sales, Compass Minerals has also been bedeviled by operational issues as well as lower salt volumes due to several years of warmer than usual winters. While salt volumes have rebounded in 2018 (up 16%), salt prices have not (down 3%).

More worrisome to Wall Street is that the Goderich salt mine's issues, which began with a ceiling collapse in September 2017, have continued to persist. That ceiling collapse was supposed to lower production for just six weeks. Instead, production issues have persisted into the third quarter of 2018, including an 11-week workers strike back in July of 2018.

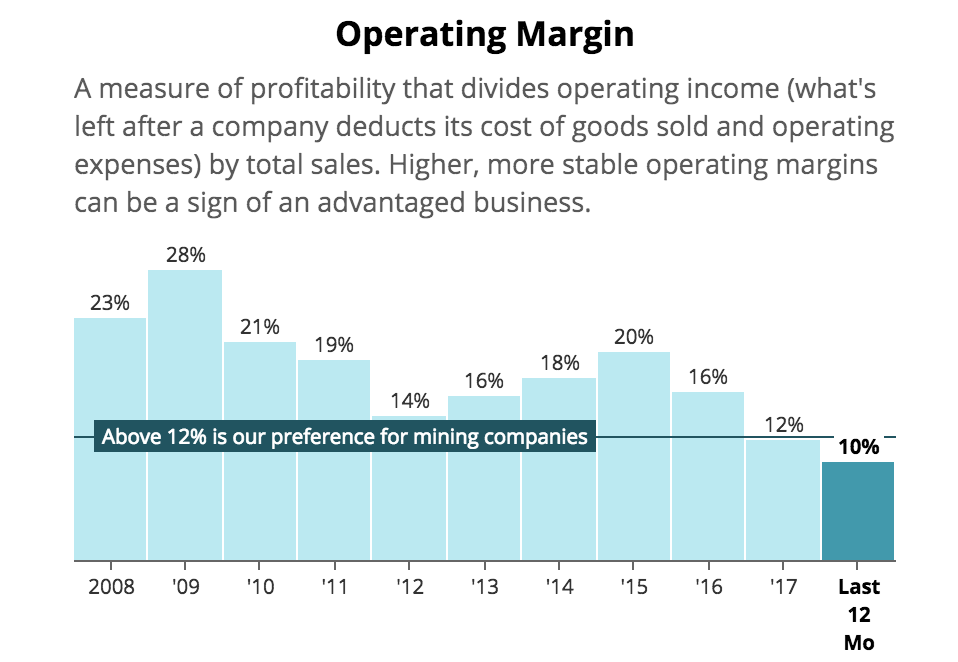

These challenges at Goderich (final investments won't be complete until early 2019) are why, despite just announcing an 18% increase in contracted pricing for salt, management expects operating margins in salt to remain flat (after falling significantly in recent years). In fact, overall operating margins for the company have fallen by 50% in the past three years.

Source: Simply Safe Dividends

What's more, the firm's specialty nutrition business, which was supposed to smooth out cash flow over time, has also suffered from a weaker than expected global agricultural market in the last few years.

While that side of the business is finally showing signs of strong growth (15% revenue growth in the third quarter of 2018 and a 45% increase in operating earnings), the company has been plagued by major challenges in Brazil, including strong currency fluctuations over the past year.

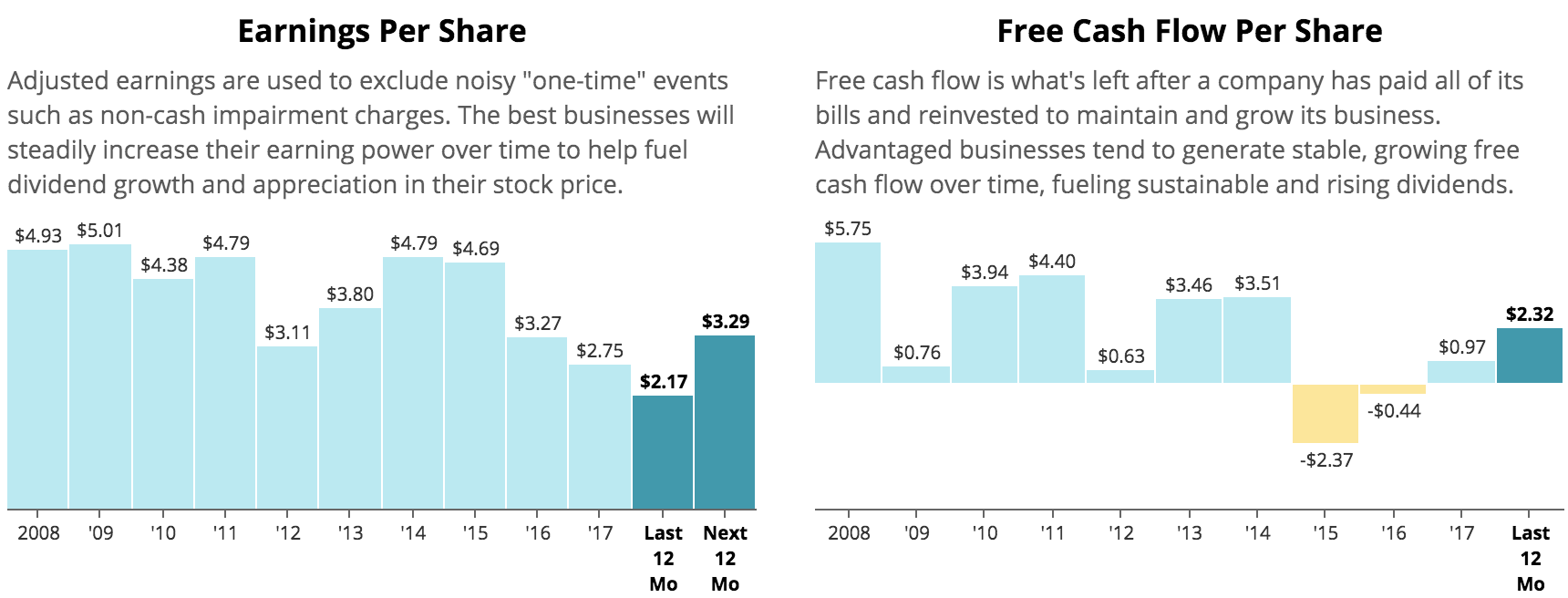

Simply put, Compass Minerals has struggled with its ambitious diversification and growth efforts, which have run into a brick wall of execution and commodity price challenges. As a result, the firm's adjusted earnings and free cash flow per share have declined 55% and 34%, respectively, since Malecha's big investment strategy was launched four years ago.

Source: Simply Safe Dividends

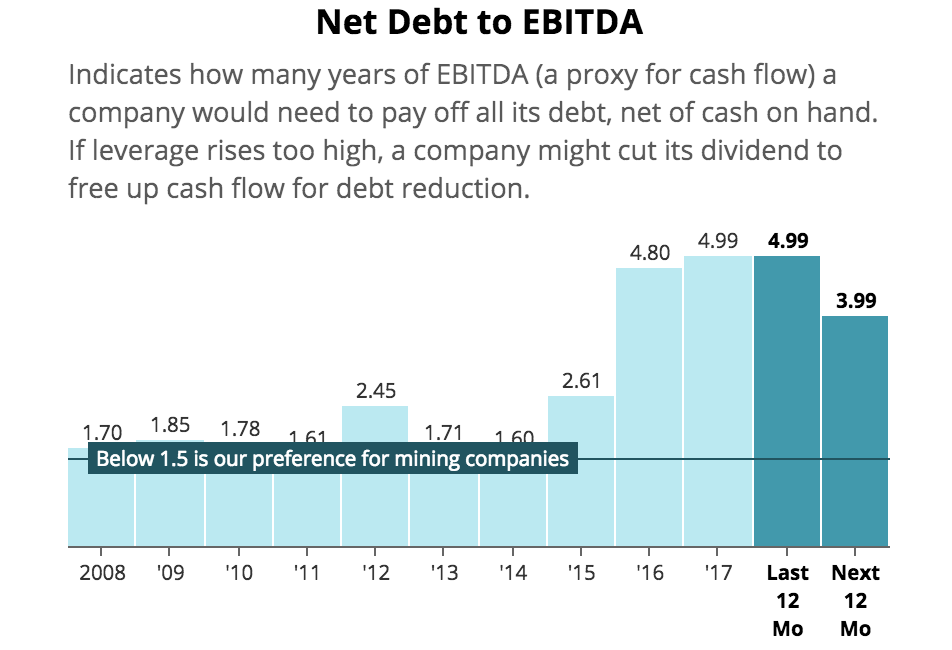

Worse, the debt the company took on to fund Malecha's acquisitions and growth plans (over $700 million in the past four years) tripled the firm's net leverage ratio (net debt/EBITDA) to dangerously high levels.

Source: Simply Safe Dividends

While the company appears to be making progress in terms of finishing up its substantial expansion plans, Malecha took investors by surprise in November 2018 when he announced he was stepping down as CEO immediately. Richard Grant, who has been a director with Compass for 14 years, will become the interim CEO until the company finds a new permanent leader.

Major management changes, especially unexpected ones like this, worry Wall Street when a company has been struggling for years. New management is often an excuse for a company to announce a major shift in its capital allocation strategy, including sometimes cutting the dividend.

How likely is Compass Minerals to suffer that fate? Unfortunately, the company's dividend profile doesn't look good.

Is Compass Mineral's Dividend Safe? Because of the cyclical nature of its industry, it's important for all mining stocks, even those with unique cost advantages like Compass Minerals, to maintain modest payout ratios and strong balance sheets.

This allows them to weather prolonged periods of low commodity prices or operational setbacks without the dividend threatening the financial health (and flexibility) of the company.

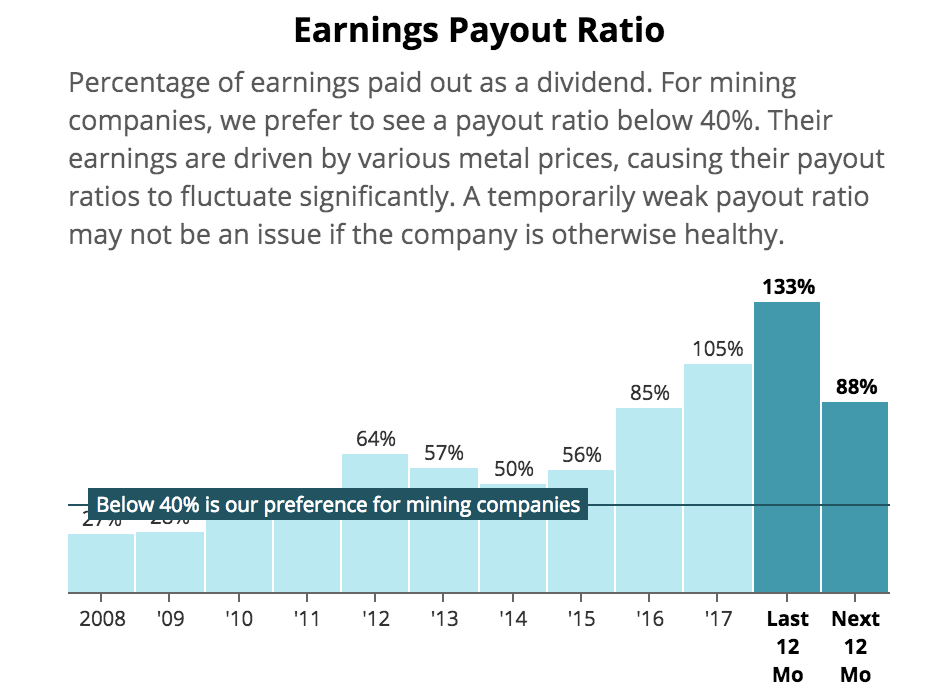

Compass Minerals' earnings payout ratio over the past year sits at 133%, well above our preferred level and indicating the dividend has not been covered by the company's profits. While some improvement is expected over the next year, a projected payout ratio near 90% still leaves the business with very little flexibility, especially if its salt business is challenged by another warm winter, or if fertilizer prices head south.

Source: Simply Safe Dividends

Compass Minerals' elevated payout ratio is all the more concerning in light of its levered up balance sheet. Management has already missed its previously announced deleveraging plan to achieve a leverage ratio of 4.3 by the end of the year. The company also seems at high risk of missing its 2019 and 2020 leverage targets of 3.3 and 2.7, respectively.

Not surprisingly, the company's credit rating sits at BB-, firmly in junk territory and making future borrowing costs much higher (when debt comes due and needs to be refinanced).

Compass Minerals' dividend costs the business about $100 million per year, which given the unsustainable payout ratio and strong need to deleverage ($1.3 billion in book debt), means that the new CEO might very well see a large dividend cut as a necessary way to free up cash to strengthen the balance sheet.

While some of the company's woes seem to be behind it for now as growth spending winds down and macro headwinds hopefully moderate, it's hard to feel comfortable owning a business whose financial position has deteriorated to such a precarious level.

We actually used to own shares of Compass Minerals in our Conservative Retirees portfolio. However, we sold the stock in November 2017 at a price of $66 per share. Here are the comments I made in our November 2017 newsletter:

CMP is a stock I have been looking to exit for several months, largely because I felt its range of potential outcomes had widened well beyond my comfort zone. The company's substantial capacity expansion projects and elevated debt load increased the stock’s risk over the past two years since I initiated my position.

We are now getting to a point where the bulk of investments are behind the company and free cash flow will substantially rise over the next few years, but mild winter weather, depressed agricultural markets, and operational challenges (including the temporary mine closure announced in September) have created additional headwinds.

CMP raised its dividend by 4% earlier this year and has around $220 million of available borrowing capacity under its revolving credit facility (compared to $94 million in annual dividend payments). The facility doesn't expire until July 2021, and fortunately the bulk of the company's debt isn't due until 2021 or later as well.

This year will obviously be very lean, so improving winter weather and agriculture market conditions will become all the more important. I don't think the dividend is at risk of an imminent cut, but the margin for error certainly looks to have narrowed again.

There is meaningful upside if CMP's end markets recover and its growth projects deliver their expected returns over the next several years, but the range of outcomes has widened after the company took on substantial debt last year and aggressively expanded its capacity.

I am ready to exit the stock since I prefer more predictability in my portfolio, which is rather concentrated and has goals of generating safe, growing income and preserving capital.

Unfortunately, my fears appear to have played out. The company's high debt load, coupled with continued macro and company-specific challenges, have put Compass Minerals' dividend on thin ice. With a new CEO coming in, increasing the odds of a capital allocation policy reset, the firm's payout could find itself on the chopping block next year.

Concluding Thoughts Compass Minerals is a classic example of a once great dividend growth stock that has fallen on hard times. The ill-timed, debt-funded investment plans of its former CEO, when combined with falling commodity prices and over a year of operational challenges at its key salt mine, have resulted in Compass Minerals struggling to support a dividend that makes its deleveraging efforts more difficult.

With a new CEO coming soon, there is a greater risk that the dividend, which in recent years has been living on borrowed time, may finally be cut to free up much-needed cash to pay down the firm's uncomfortably high debt levels.

While a dividend cut is not a guarantee, conservative income investors, especially retirees looking to live of dividends and preserve capital, should probably avoid this indebted company as it works to figure out its new direction.