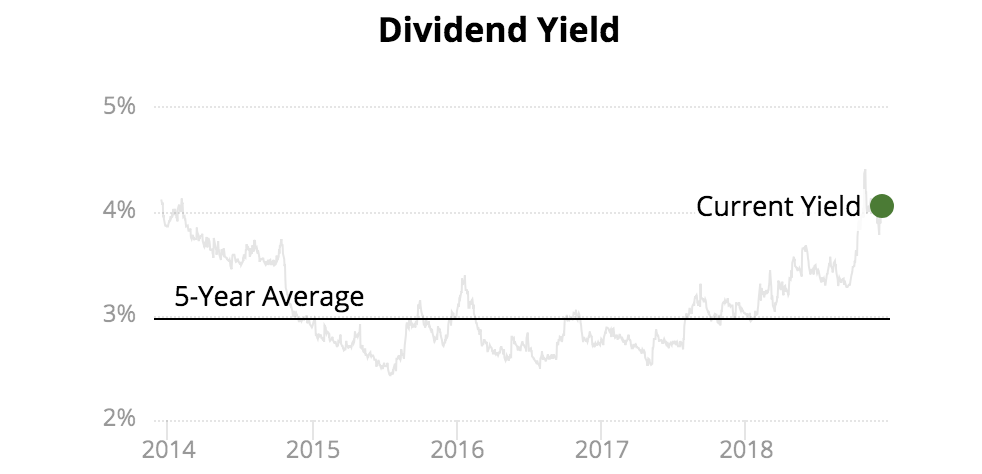

With a 4.1% yield, Leggett & Platt (LEG) is one of the highest-yielding dividend aristocrats in the market, trailing only AT&T (T), AbbVie (ABBV), and Exxon Mobil (XOM).

While the company has increased its dividend for 47 consecutive years, shares of Leggett & Platt are down more than 20% over the past year. As a result, the stock's dividend yield has increased to an unusually high level compared to its historical trading range.

Source: Simply Safe Dividends

If nothing has changed with a company's long-term prospects or dividend safety, a relatively high yield can be a signal that a business is attractively priced.

Leggett & Platt's situation is a little more complicated due to the $1.25 billion acquisition of Elite Comfort Solutions management announced last month.

Not only is this deal being funded with debt, which will result in a spike in the company's leverage metrics, but Leggett & Platt also announced plans to "modestly" change its dividend payout target to 50% of earnings (from 50-60% of earnings previously).

Let's take a closer look at this deal to understand the implications it has for the firm's dividend safety and long-term outlook.

Leggett & Platt's Dividend Expected to Remain Safe and (Slowly) Growing

Acquiring Elite Comfort Solutions (ECS) will approximately double the amount of debt Leggett & Platt holds. If companies stretch their balance sheets too far and run into cash flow problems, the dividend can be at risk of a cut to create more flexibility for debt reduction.

Fortunately, this risk seems very low for Leggett & Platt. Prior to the deal, the company's net debt to EBITDA leverage ratio sat at 2.4, a comfortable level that helped earned the firm a solid investment grade credit rating.

Source: Simply Safe Dividends

Once the deal closes in January 2019, we estimate Leggett & Platt's net debt to EBITDA ratio will rise to around 4.0 to 4.5. While that's higher than we like to see as conservative investors, management has plans to aggressively pay down debt and return to a leverage ratio of no more than 2.5 by the end of 2020:

"The company is committed to maintaining a strong, investment grade profile and expects to quickly deleverage (to a target level ratio of debt to trailing 12-months EBITDA of approximately 2.5x) by suspending share repurchases, reducing other acquisition spending, and using part of the combined company's operating cash flow to repay debt."

Looking at the numbers, the combined company is expected to generate $550 million in annual operating cash flow. We estimate capital expenditures needed to maintain and grow the business will total around $170 million, leaving $380 million for debt reduction and dividends.

Leggett & Platt's dividend consumes around $207 million per year, so close to $175 million should be available to chip away at the firm's estimated $2.5 billion debt load following the acquisition. As the combined company's cash flow continues growing, more funds will be available each year to pay down debt.

Keeping dividend growth to an absolute minimum will maximize the amount of retained cash flow that can reduce debt. For that reason, earnings growth will outpace dividend growth over the next few years, resulting in Leggett & Platt's payout ratio floating down from 60% today towards 50%.

Despite lowering the company's payout ratio target, management's support for the dividend remains extremely strong. Here is what the firm's CFO said on the conference call:

"With all of these factors considered, we are modestly changing our dividend payout target to approximately 50% of earnings from 50% to 60% of earnings, previously. However, let me quickly reiterate that we strongly maintain our commitment to long-term dividend growth and, certainly, expect to extend Leggett & Platt's 47-year dividend growth track record."

Simply put, Leggett & Platt's acquisition of ECS does not appear to threaten the firm's dividend safety, and management remains as committed as ever to continuing the firm's dividend growth streak. Investors just shouldn't expect much more than low single-digit payout increases for the next couple of years.

So why is Leggett & Platt acquiring ECS anyway?

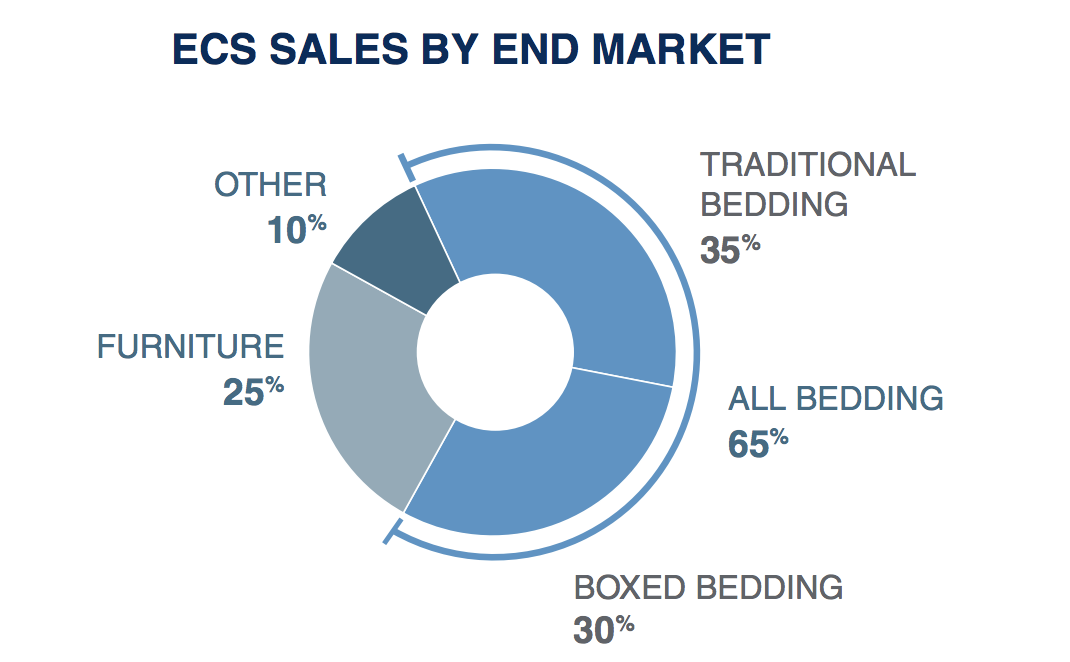

ECS is a leader in high-quality specialty foam used in bedding and furniture markets, which account for more than 25% of Leggett & Platt's product sales today. ECS's $600+ million revenue base is growing at a double-digit rate, and its EBITDA margins are higher than Leggett & Platt's.

Besides its attractive financial profile, ECS's business is concentrated in key growth areas of the future. Premium foam and hybrid mattresses are expected to gain share in the years ahead as online mattress sales grow rapidly (expected to more than double over the next 4-5 years according to Leggett & Platt).

"Boxed bedding" is an emerging trend, especially in the online mattress channel, and ECS derives 30% of its revenue from these products. With compressed mattresses anticipated to be half of the market by 2026 (up from 25% today), demand for ECS's premium foam should continue growing at fast pace.

Source: Leggett & Platt Investor Presentation

In total, ECS will account for approximately 12.5% of the combined company's revenue once the deal closes and is expected to grow "well above" Leggett & Platt's average for the next several years.

From a strategic fit perspective, it's hard not to like this acquisition. It just makes sense as the mattress industry continues moving more online. However, Leggett & Platt will have even more exposure to bedding and furniture, which are sensitive to housing market and employment trends.

The bears could argue that not only did Leggett & Platt pay a steep multiple for ECS's growth (likely north of 10x EBITDA), but the deal comes at an inopportune time with the housing market showing signs of slowing down. (Existing home sales fell from a year earlier for seven consecutive months through September 2018.)

Of course, no one can predict where the housing market or economy will head in the short term. Many of Leggett & Platt's end markets are rather cyclical and driven by consumer spending, so the stock can be volatile as economic growth forecasts change.

While a recession in the next year would be poor timing given the firm's temporarily stretched balance sheet and cyclical sales, it seems unlikely to threaten the dividend or Leggett & Platt's long-term trajectory. The company has no long-term debt maturing through 2021, generates solid free cash flow, and should continue having affordable access to credit markets if the need arises.

Big acquisitions can certainly be risky, but management deserves the benefit of the doubt in this case. Not only is Leggett & Platt an expert in the mattress market (bedding components represented nearly 100% of sales in 1960), but the firm has successfully integrated dozens of acquired businesses over the years.

Investors shouldn't expect much dividend growth over the next couple of years and need to make sure the company's deleveraging efforts go as planned, but Leggett & Platt's long-term outlook and dividend safety appear to remain solid.