A Closer Look at TransCanada's Unusually High Dividend Yield

Despite paying higher dividends each year since 2000, North American pipeline giant TransCanada (TRP) has seen its share price slump nearly 20% in 2018. As a result, TRP's dividend yield sits at 5.3%, near its highest level since the financial crisis.

The midstream industry has been under pressure since the price of oil began tumbling in 2014. Many firms in this space are structured as master limited partnerships (MLPs) and have faced the most strain due to unfavorable regulatory developments, rising interest rates, and souring investor sentiment.

However, TransCanada is a corporation, not an MLP, so many of those headwinds are less relevant to its performance. With the stock's yield sitting high compared to its history, let's take a closer look at TransCanada's dividend safety and long-term outlook.

Why TransCanada has Underperformed

Some of the factors weighing on TransCanada are outside of management's control. Specifically, the midstream industry has been in a bear market for more than four years.

Weakness has largely been driven by a perfect storm of factors, many of which have hit MLPs the hardest:

The crash in oil prices (fell 76% from mid-2014 to early 2016, weakening the outlook for energy producers / midstream customers)

Several market corrections (more costly to issue equity growth capital)

interest rates rising off their lowest levels in history (these are capital intensive businesses that rely heavily on debt financing)

The breaking of the traditional midstream MLP business model (due to an inability to fund growth through selling equity at very low unit prices)

However, as a corporation, TransCanada is not an MLP and thus has not been affected by the industry's necessary shift towards simplified corporate structures (eliminating incentive distribution rights and, in some cases, corporate conversions).

The only exposure TransCanada has is its ownership stake in its own MLP, TC Pipelines (TCP). TransCanada owns around 25% of this partnership's common units, as well as all of its incentive distribution rights.

The company essentially used TC Pipelines as a financing vehicles. TC Pipelines would issue new units and debt to periodically buy some of TransCanada's assets, providing its parent with capital it could use to invest in the next growth project.

Unfortunately, TC Pipelines was negatively affected by a rule change made by the Federal Energy Regulatory Commission (FERC) in March 2018, which resulted in TC Pipelines cutting its distribution and being unable to profitably fund its growth projects since its unit price was in the dumps.

Fortunately, TransCanada's exposure to TC Pipelines is less than 10% of its total EBITDA. However, the firm has had to find alternative sources of financing (more on that later).

TransCanada seems likely to eventually buyout its MLP in an accretive share-funded deal. Given that TransCanada's market cap is 18 times that of TC Pipelines, and the MLP is trading at 5.7 times forward cash flow, TransCanada rolling up its MLP is likely to be beneficial to the company and increase distributable cash flow per share.

Another reason that TransCanada has likely sold off is the recent bear market in oil prices. Crude has fallen over 30% from its recent highs, including a 22% crash in November, the fastest monthly decline since 2008. The market might be worried that another oil crash is forming.

However, while the Organization of the Petroleum Exporting Countries (OPEC) and the International Energy Administration (IEA) are expecting slower oil demand growth next year, OPEC and Russia (who joined forces in 2016 and reaffirmed their partnership through the end of 2019 at the G20 summit) have said they won't allow another oil crash to happen.

In fact, OPEC and Russia just announced that they will be cutting oil production by 1.2 million barrels per day (bpd), representing about 1.3% of global oil production. That offsets the recent 1.2 million bpd increase they enacted ahead of Iranian sanctions which U.S. import waivers have caused to not disrupt the global oil market as previously feared.

What's more, Alberta's government has orchestrated a 300,000 bpd production cut in that Canadian province, largely due to the price difference between Canadian crude and global oil hitting record highs (due to a lack of pipeline takeaway capacity).

While no one can forecast the prices of commodities with any consistency, a 1.5 million bpd decrease in production means that, even with U.S. shale production expected to continue growing strongly in the coming years, it seems unlikely that oil prices will fall anywhere close to their $26 per barrel lows reached in early 2016.

But what about the biggest worry that income investors have, which is that TransCanada's fundamental dividend growth thesis might be broken?

TransCanada's Dividend Outlook Remains Solid

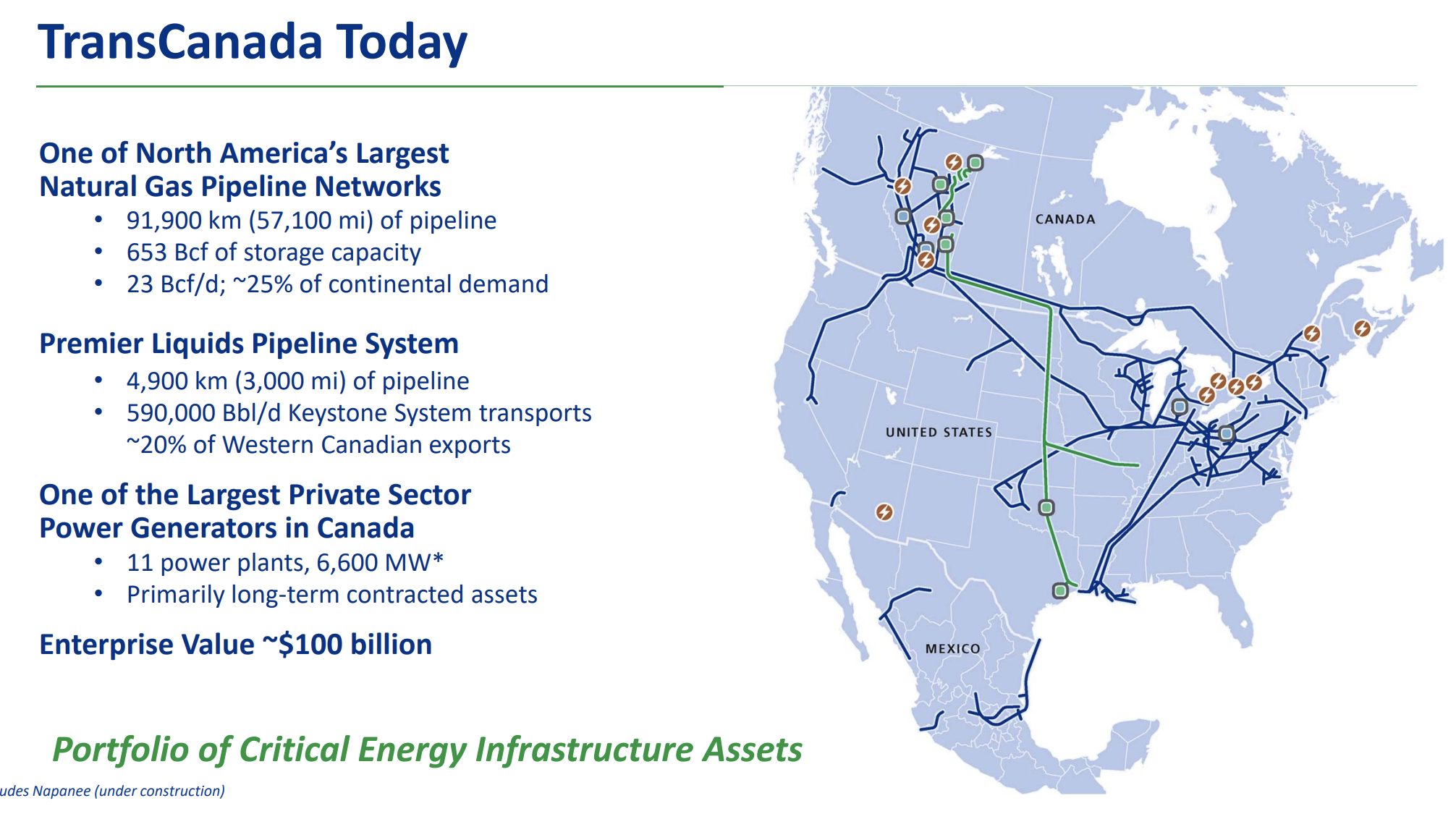

TransCanada was founded in 1951 and is North America's second largest midstream company (behind Enbridge).

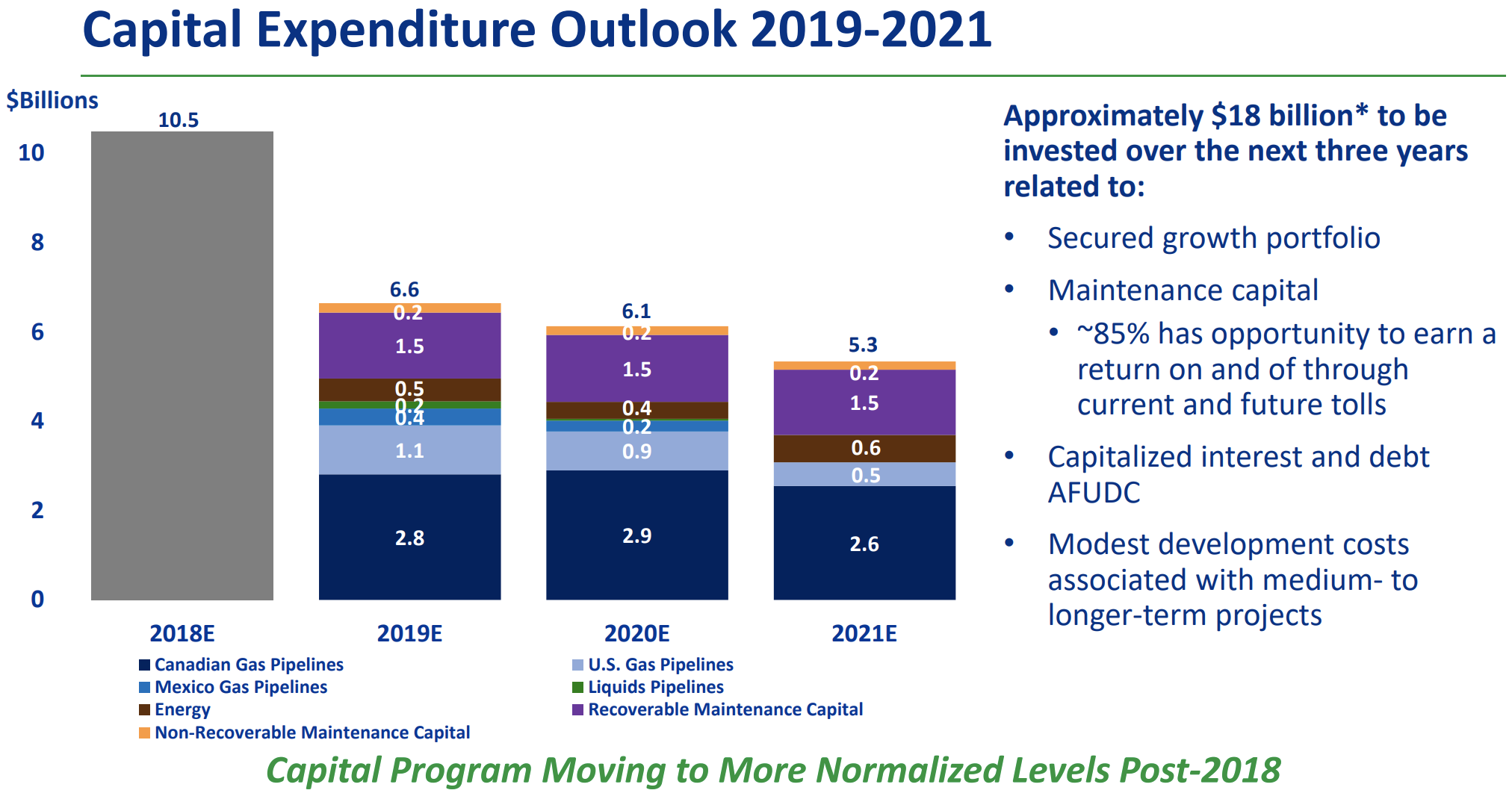

Over the last 18 years, TransCanada has spent $64 billion expanding its network of oil & gas pipelines, storage capacity, and regulated utilities. The firm's midstream network now carries 25% of the continent's natural gas and 20% of Canada's oil export capacity.

Source: TransCanada Investor Presentation

TransCanada's business model is built around maximizing recurring cash flow. Approximately 95% of its cash flow is either regulated (10.1% return on equity for its utilities), or under long-term (10- to 20-year) fixed-rate and volume committed contracts.

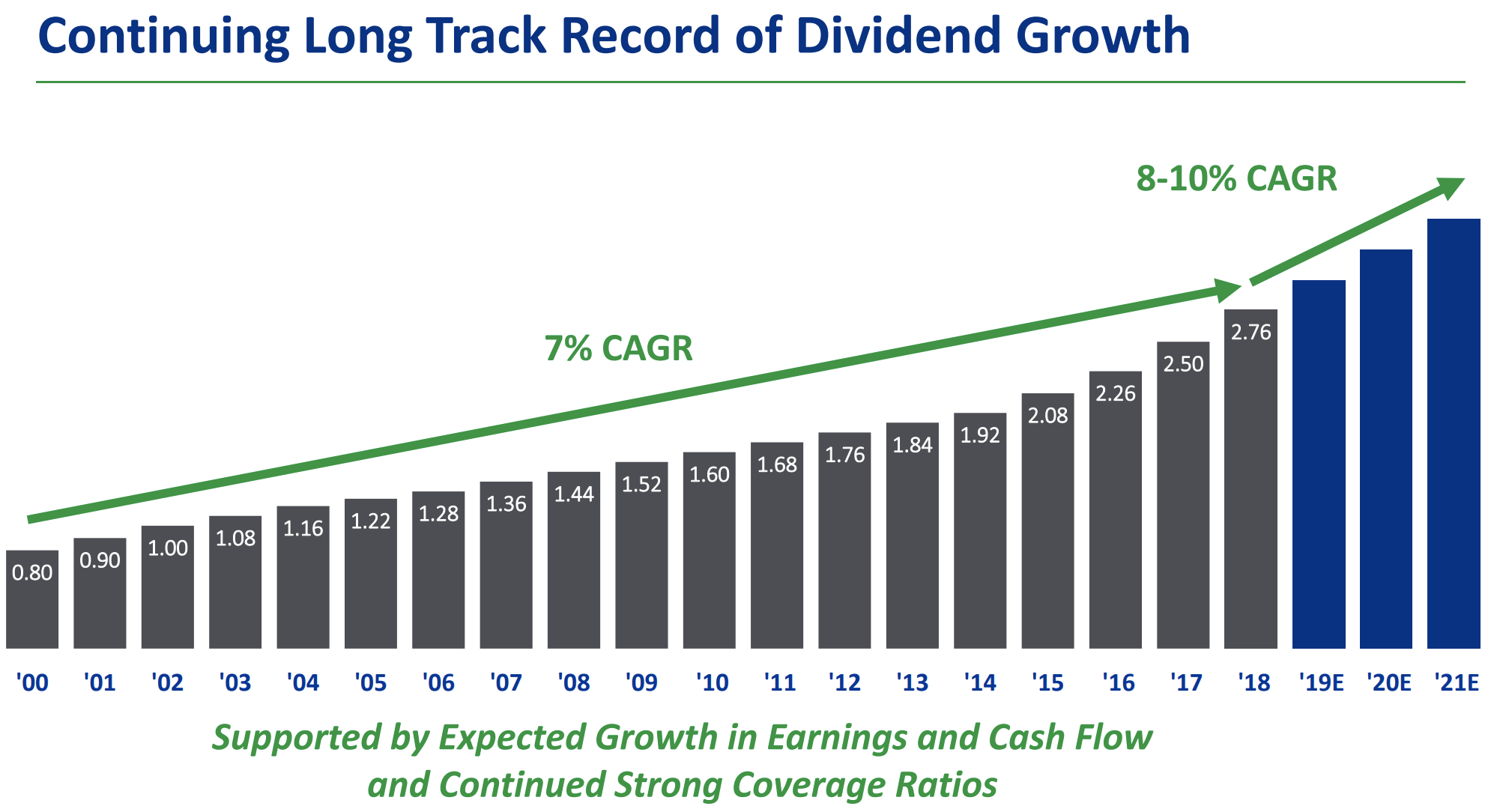

Thanks to its stable and commodity insensitive distributable cash flow (similar to free cash flow for midstream companies), TransCanada has managed to deliver impressive dividend growth for 18 consecutive years. Management even plans to accelerate the company's dividend growth rate over the next three years as well.

Source: TransCanada Investor Presentation

Since 2000, TransCanada's safe and growing dividend (even during recessions and oil crashes) has allowed it to deliver 12% annualized total returns, more than doubling the S&P 500's 5.6% annual return over that time.

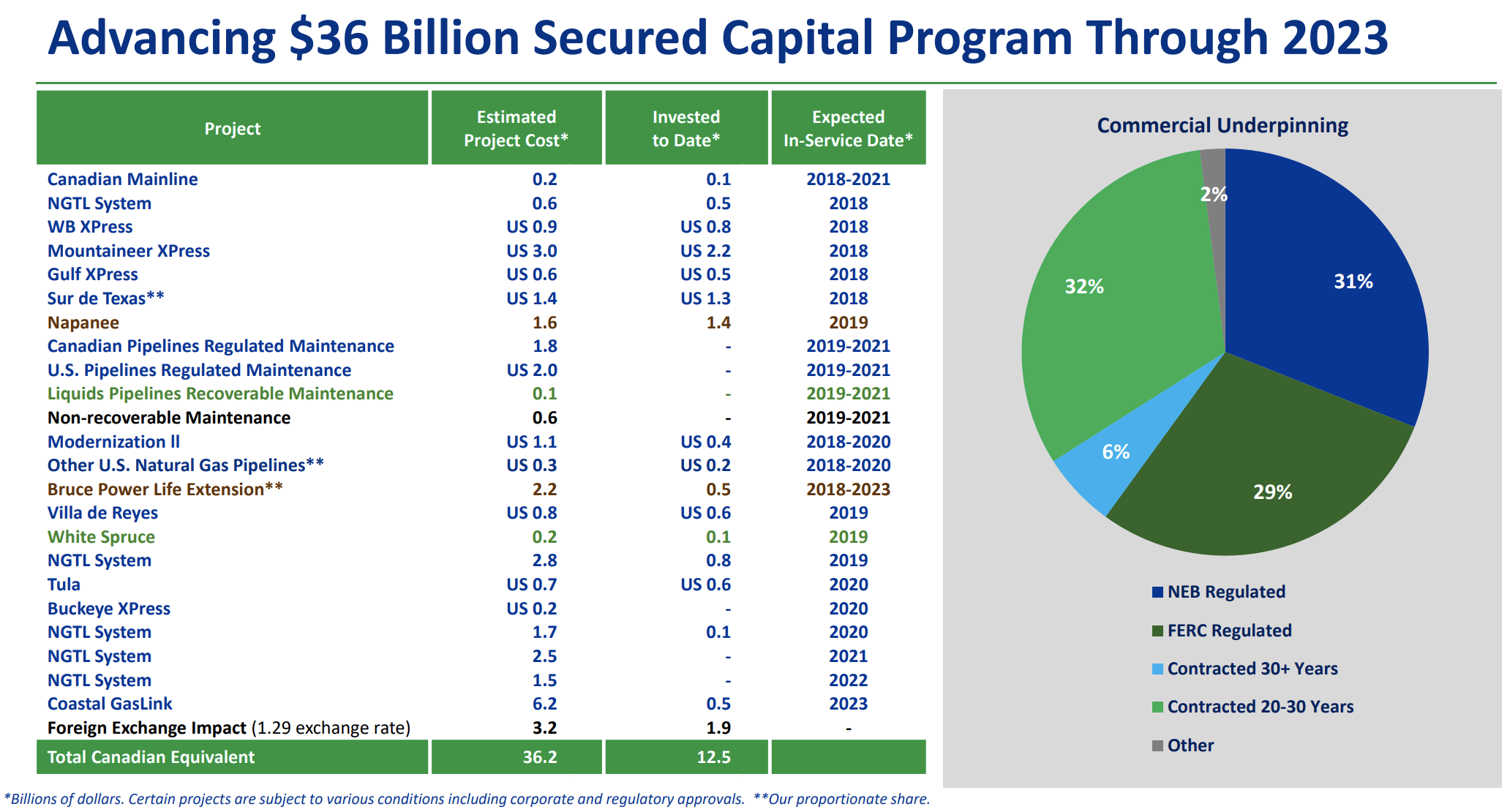

Today TransCanada has a $27 billion growth backlog, the largest in the industry. And including its shadow backlog (projects that have yet to obtain contracts but that are expected to), TransCanada's growth backlog is over $35 billion in size, enough to grow its asset base by about 40% in the years ahead.

Source: TransCanada Investor Presentation

In addition, management is working on reviving its old Keystone XL pipeline. That $8 billion project was started in 2008 but suspended in 2015 when President Obama pulled regulatory authorization.

President Trump has reinstated the Keystone XL pipeline, and now the company is attempting to get the project completed by 2022. A recent court ruling has forced another U.S. environmental impact study (likely causing a one-year delay), but investors need to keep in mind two things.

First, TransCanada's growth plans do not include Keystone XL. That project merely serves as a potential cherry on top, but one that could boost the company's growth backlog by up to 30%. Second, the company has already obtained firm 20-year volume committed fixed-rate contracts for 93% of its capacity.

Even if Keystone XL were to once more get blocked by regulators, TransCanada should have more than ample cash flow growth from its remaining backlog to deliver on its 8% to 10% planned dividend growth through 2021. That's because the company's completed projects by 2021 are expected to increase cash flow by 28% (9% annual growth). Keystone XL, if ultimately approved, would likely be completed in 2022 and further enhance TransCanada's cash flow growth rate.

From a financing perspective, TransCanada's management says it has a "sizable portfolio of saleable assets" that the firm would be willing to part with to fund part of the Keystone XL program, or to avoid share count grow in the future. The company could also bring on joint venture partners to provide funding.

Even in a worst case scenario, the Keystone XL pipeline does not appear to pose a threat to TransCanada's dividend. For now, it remains a waiting game to see if TransCanada is willing to push forward with construction given the approval uncertainties Keystone XL faces.

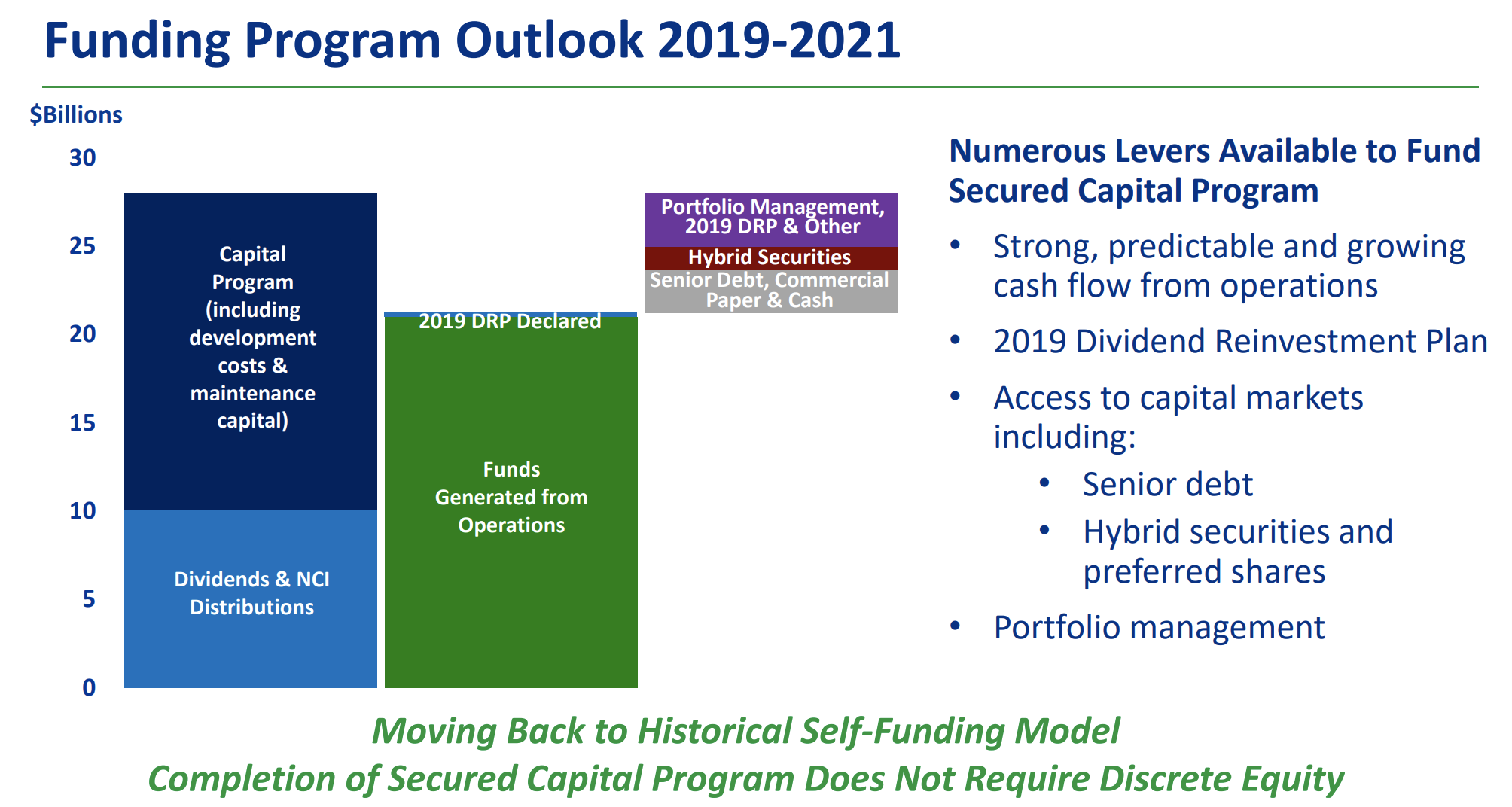

Perhaps most importantly for TransCanada's dividend safety is the company's conservative self-funding business model. The firm targets a long-term distributable cash flow payout ratio of just 40%, meaning 60% of internally generated cash flow (highest level in the industry) will be retained to fund its growth ambitions and dividend without the need for any equity issuances.

In other words, TransCanada's organic growth plans should have zero sensitivity to its share price, reducing financing risk. The company plans to fund the majority of its growth with retained cash flow and leverage that with modest amounts of low-cost debt, non-core asset sales, and proceeds from its dividend reinvestment plan.

Source: TransCanada Investor Presentation

TransCanada's ability to access debt financing also appears to be at low risk thanks to the company's steady deleveraging efforts and favorable debt maturity schedule. Less than $6 billion of long-term debt is due through 2021, an amount that is easily covered by the firm's $10 billion of undrawn credit lines alone.

While TransCanada's leverage ratios remain relatively high compared to other conservative midstream players, the trend is headed in the right direction.

Source: TransCanada Investor Presentation

By the end of next year, TransCanada's debt/EBITDA ratio is expected to fall below 5, and the company's strong contracts and counterparty profile (nearly all cash flow from investment grade companies and utilities) has allowed the firm to retain a stable BBB+ credit rating. That's tied for the highest in the industry with other midstream blue-chips like Enbridge (ENB), Magellan Midstream Partners (MMP), and Enterprise Products Partners (EPD).

Given the company's plans to retain 60% of distributable cash flow going forward (despite growing the dividend at a fast pace), TransCanada's leverage ratio is likely to continue gradually declining over time due to its modest plans for future debt issuances and declining capital expenditures.

Source: TransCanada Investor Presentation

TransCanada's cash flow and dividend growth outlook remains solid beyond just the next few years as well. Rising North American oil & gas production, supported by both domestic consumption and strong export demand, is expected to continue for decades, driving higher demand for midstream infrastructure.

Source: TransCanada Investor Presentation

The point is that TransCanada's dividend profile, both in terms of safety and long-term growth potential, appears to remain intact. As the company continues improving its balance sheet and bringing its various growth projects online, its business should only find itself on more solid ground.

Concluding Thoughts

A multiyear bear market for midstream stocks is enough to try the patience of even the most committed long-term investor. TransCanada's underperformance in 2018 is largely a function of negative industry sentiment, the market's seemingly overblown fears about a possible future oil crash, and uncertainty surrounding the Keystone XL project.

However, TransCanada's fundamentals appear not only supportive of its dividend and among the strongest in the industry, but they should continue improving in the years ahead.

Thank's to the firm's large growth backlog, conservative self-funding business model, and solid and improving balance sheet, TransCanada appears to remain well positioned to profit from North America's ongoing energy boom.

And with 95% of cash flow derived from regulated or contracted assets, TransCanada should be able to continue delivering on its planned 8% to 10% annual dividend growth regardless of what commodity prices, the economy, or interest rates are doing.

For dividend growth investors interested in the midstream space, TransCanada appears to remain one of the higher quality options, even despite some of the uncertainties facing the Keystone XL pipeline.