Invesco Remains Under Pressure as Investment Industry Evolves

Asset manager Invesco (IVZ) has seen its shares plunge over 50% in 2018, resulting in its dividend yield soaring to a record high of 6.9%. Although the company has increased its dividend each year for more than a decade, the stock's recent performance is causing many income income investors to feel anxious.

Let's take a look at why the market is so worried about Invesco and whether those fears mean the dividend could be at risk of a cut.

Why Investors are Bearish on Invesco

There are several reasons why Invesco shares have been pummeled so badly this year. First, understand that asset managers generate most of their profits (80% for Invesco) from fees charged for managing clients' money.

These fees are usually assessed as a percentage of assets under management (AUM), so the industry is naturally very sensitive to the broader stock market's performance. With two corrections in 2018, the environment for investment managers has not been ideal.

Another reason for the broader slump in asset managers is due to the market's worries over the continued growth in passive mutual funds and ETFs, which have lower expense ratios and continue stealing share from active managers.

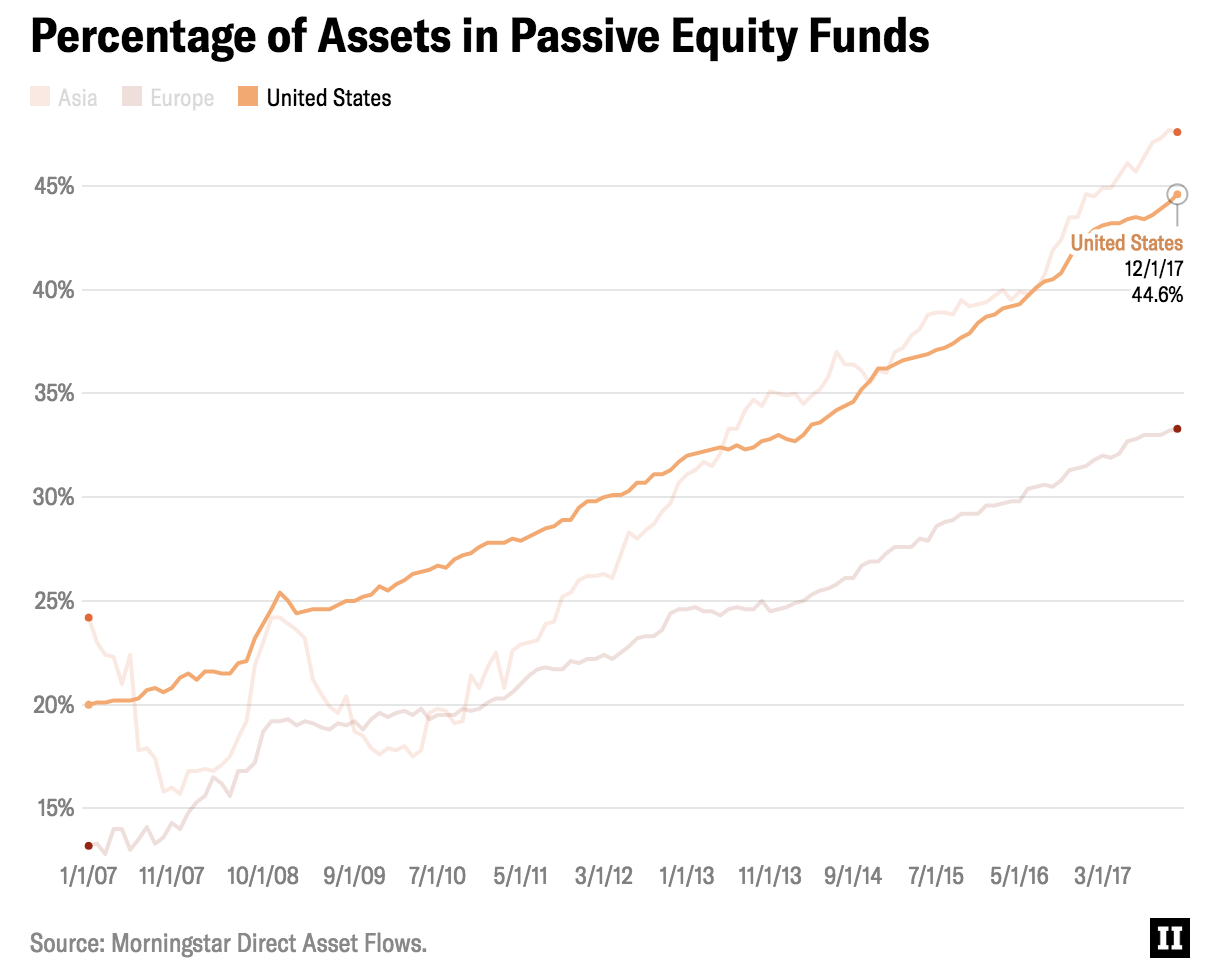

Since 2007, the percentage of U.S. assets in passive equity funds has more than doubled from 20% to about 45% at the end of 2017, according to Morningstar data cited by Institutional Investor.

Source: Institutional Investor

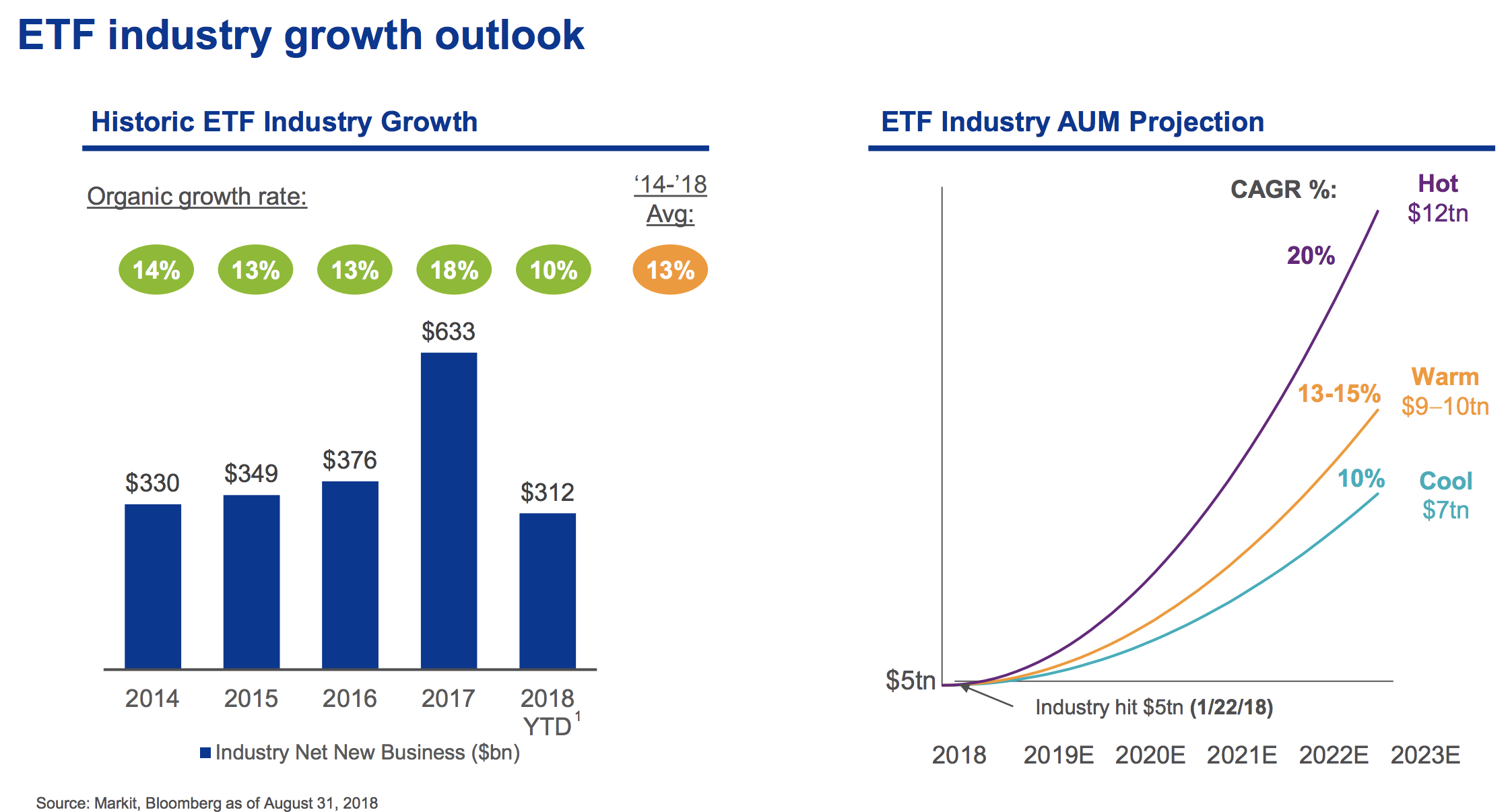

Since the ETF industry is expected to grow 10% to 20% per year over the next five years, that will only further worsen fears about asset manager fee compression and a "race to the bottom" on ETFs. In fact, Fidelity recently unveiled two ETFs with zero expense ratios, and according to CNBC, these funds raised $1 billion in assets in their first full month of operation.

Source: BlackRock Investor Presentation

Passive funds make up 26% of Invesco's AUM (mostly its popular PowerShares ETF brand, which includes the QQQ Nasdaq ETF), meaning that the vast majority of its revenue is derived from higher-cost active funds which are becoming increasingly out of favor with investors.

After the Oppenheimer deal closes (more on this in a moment), about 23% of Invesco's AUM will be from ETFs; the firm will be the fourth largest passive fund manager in the world.

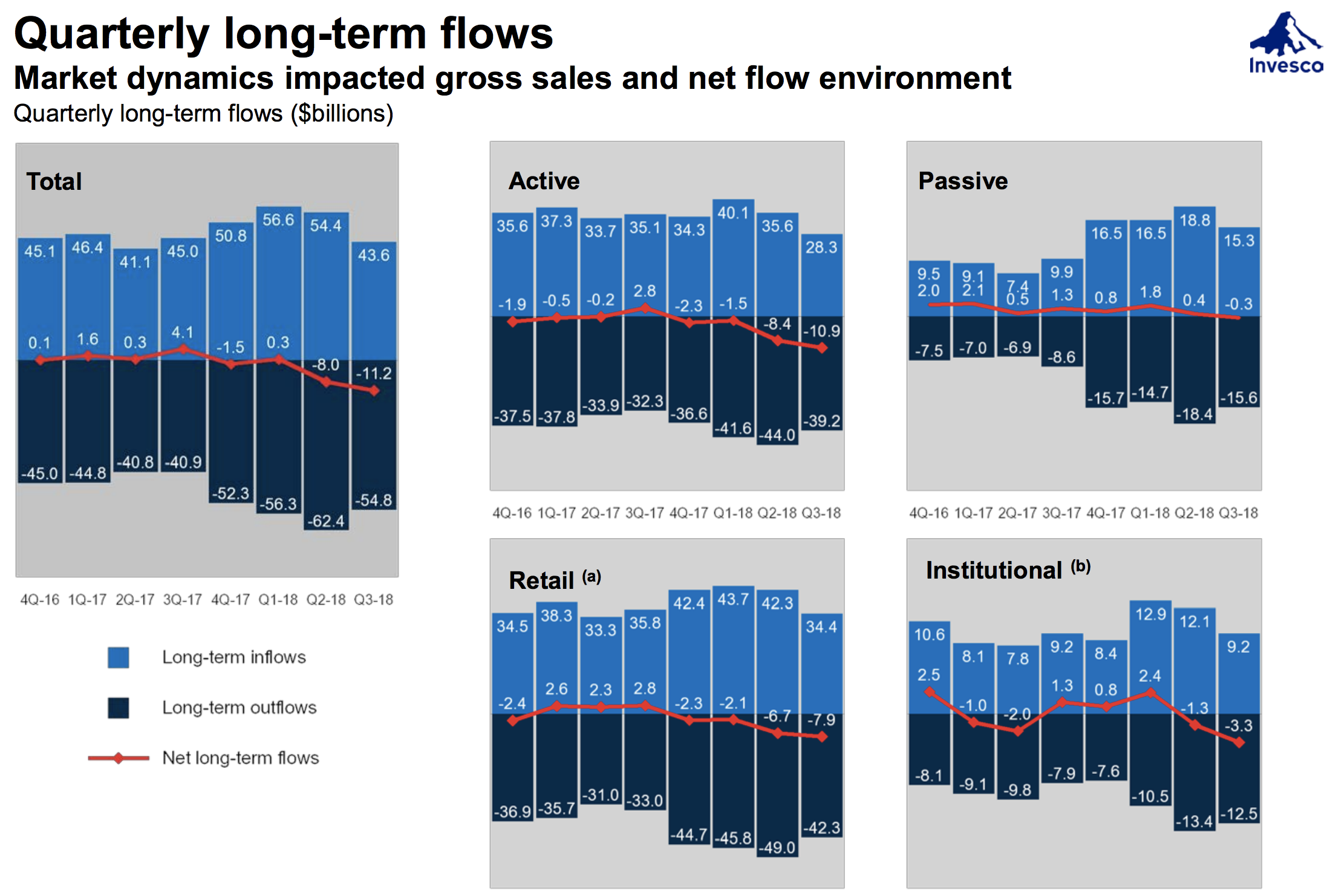

Unfortunately, investors are concerned that Invesco's strong historical organic growth might be coming to an end thanks to more than $19 billion in net outflows over the last two quarters (and management warning that more are to come).

What's more, the company's 0.47% average expense ratio (at the start of 2018) is likely to continue shrinking due to the popularity of passive funds which usually have fees of 0.1% or less.

Source: Invesco Earnings Presentation

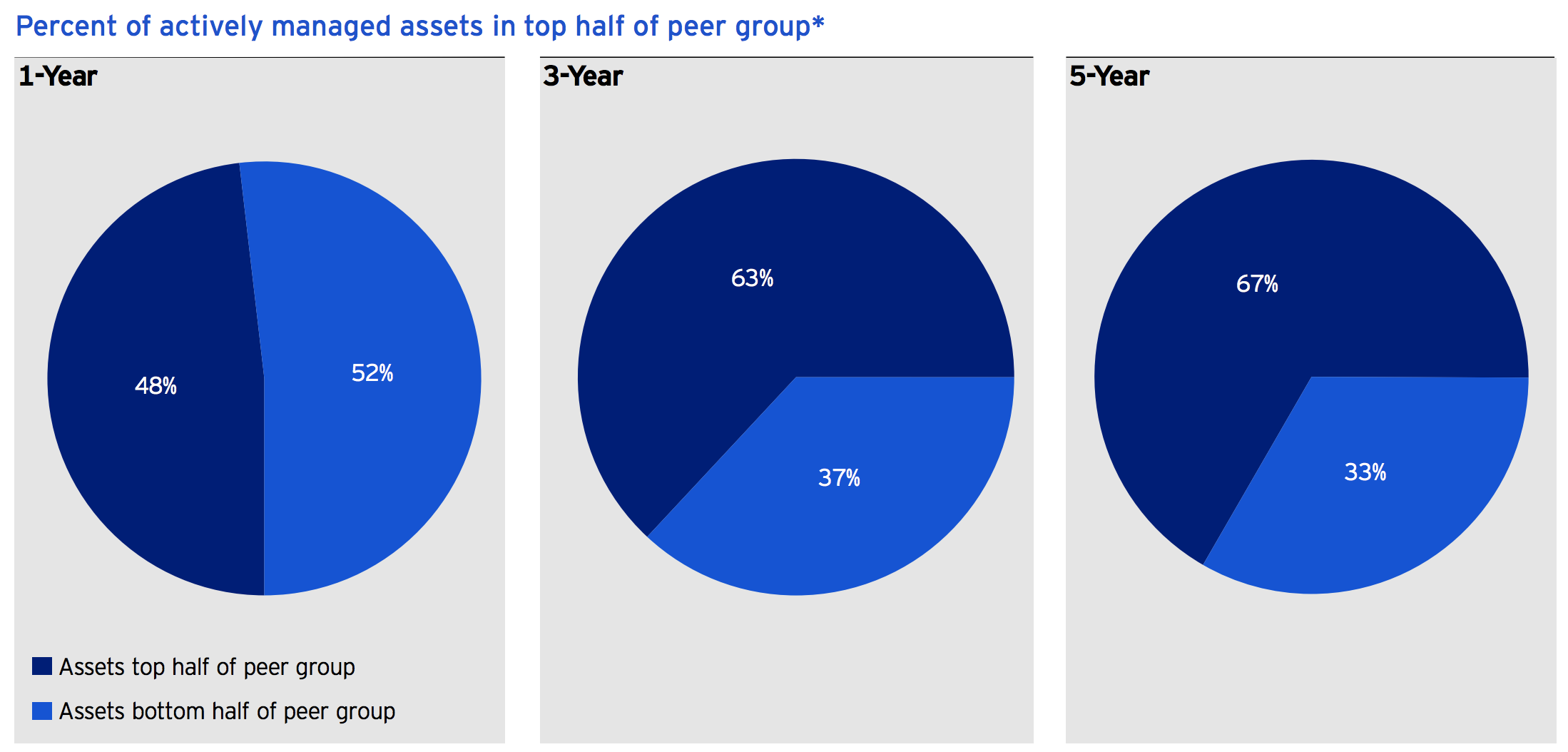

Part of the recent uptick in net outflows is due to Invesco's active funds performing poorly relative to its peers in the past year. Over the last five years the majority of Invesco's active funds outperformed other active funds, but that winning streak has been weakening in recent years, with less than half of its assets in the top half of their peer group this past year.

Should passive management continue taking share, active managers with the weakest performance and highest fees will find themselves most vulnerable to losing business.

Source: Invesco Earnings Presentation

Another important reason for the market's pessimism about Invesco is the firm's October 2018 announcement that it will be buying OppenheimerFunds from MassMutual in a $5.7 billion deal.

Given that Invesco's market cap is less than $8 billion, this is a truly significant deal and comes with large amounts of complexity and execution risk.

While Oppenheimer has about $220 billion in high-margin AUM (average expense ratio 0.61%), which will thus boost Invesco's AUM by 22% to $1.2 trillion and make it the 13th largest asset manager in the world (6th biggest in the U.S.), the company might be paying a high price out of desperation.

Invesco is paying for the acquisition (expected to close during the second quarter of 2019) with a lot of common and preferred stock. The new equity it's issuing (81.9 million shares) amounts to 20% share dilution for existing investors, which will naturally put some downward pressure on the share price.

The rest of the deal is funded by issuing $4 billion in perpetual, non-cumulative preferred shares with a 21-year non-call period and a fixed rate of 5.9%. This means that Invesco is going to be required to pay $236 million in preferred dividends each year to these new investors before it pays common equity holders.

Another way to think about these preferred shares is that Invesco is locking in a fairly high cost of capital, higher than its BBB+ credit rating might indicate had it chosen to try to finance the deal with debt. The total extra dividend cost (preferred and common) due to this acquisition comes to $333 million per year, or a 68% increase to the company's $487 million in trailing 12-month dividends paid.

While Oppenheimer adds $1.2 billion in net revenues (expected to boost Invesco's earnings per share by 18% and 27% in 2019 and 2020, respectively) to help cover the higher dividend cost, there is plenty of uncertainty regarding the sustainability of the combined company's cash flow. From a potential market downturn to continued share losses at the hands of lower-cost passive products, there is a lot of downward pressure on both businesses.

Invesco might also be suffering right now because while the firm has a good track record of growing organic AUM (1.7% annually over the last 10 years), its profitability has been historically below its peers.

For example, in recent years Invesco's operating margin has averaged around 25%, while T. Rowe Price (TROW) and BlackRock (TROW) have margins exceeding 40% thanks in part to their larger economies of scale.

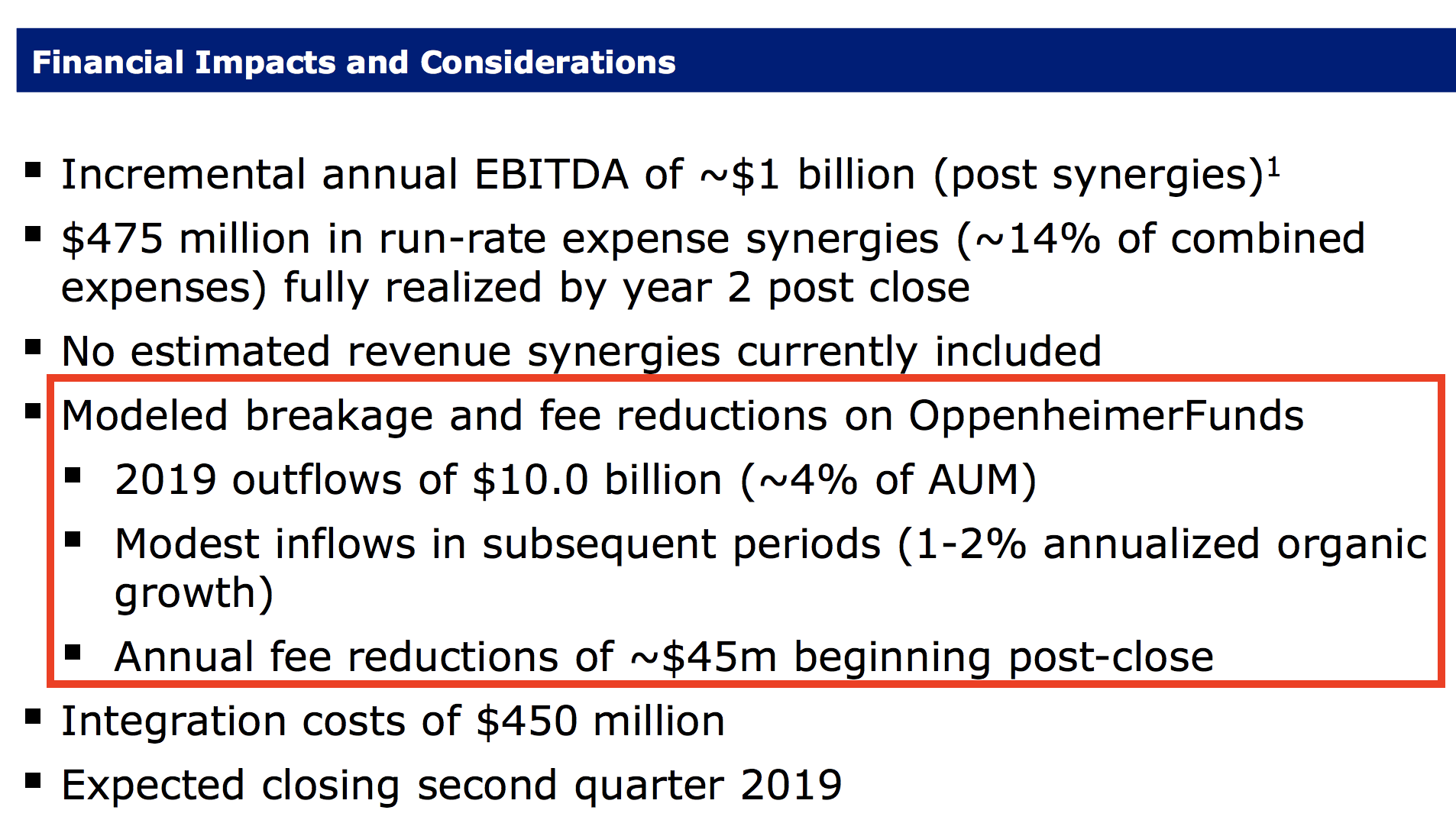

One of the justifications for the Oppenheimer acquisition is to boost Invesco's scale to improve its profitability profile. Once management's anticipated cost synergies are completed ($475 million by 2020), Invesco expects its annual EBITDA to increase by $1 billion per year.

However, since Oppenheimer is primarily in the business of actively managed funds, Invesco might have paid a rich price for a business which could now be in secular decline. Essentially, one melting ice cube could be buying another (and potentially near the top of a nine-year bull market).

In addition, Oppenheimer has had some major fund managers announce retirements recently, which highlights the risk of management talent (for individual funds) leaving post-merger.

As a result, while Invesco's profitability might potentially be boosted in the short term, its AUM organic growth rate seems very likely to take a hit going forward due to the secular shift away from active management.

Let's take a closer look at what all of this means for Invesco's dividend.

Is Invesco's Dividend Safe?

The first thing that should be noted about the Oppenheimer deal is that management actually expects the acquisition to be highly accretive to EPS in both 2019 and 2020 (by 18% and 27%, respectively).

In other words, the extra cash flow generated from the new assets is expected to more than cover the higher dividend costs for the company (and even result in a lower payout ratio).

Furthermore, according to management, the Oppenheimer acquisition should ultimately generate 19% returns on invested capital, which is more than double the company's current return of 8%.

Even if the stock market were to take a big hit, reducing the fee revenue earned by Oppenheimer, the deal is expected to be accretive and deliver a healthy internal rate of return. Here's what management stated recently at a conference:

"One thing I would also mention is we've done stress tests on this, obviously, so if you saw a fairly significant market drop, you know, would you still say this is a great deal? And we have found that even though the [internal rate of return] does get sort of cut by about 3 percentage points, so you get around to 16, 17, you know, accretion is still very strong and so it absolutely holds together in even this, sort of, really bad market scenario where we were looking at some 35% market drop all in day one, so, which, hopefully does not happen. But, ultimately gives us comfort that financially this deal holds together under all these stress tests."

To be fair, not all of Invesco's business is in the crosshairs of passive management. The firm is one of the six largest wealth management players in the country, has meaningfully operations abroad where passive is somewhat less of a threat today, and continues developing more of its own ETF products.

The hard part is understanding how all of these drivers come together, but analysts expect Invesco to generate about 3% to 4% annual revenue growth going forward. Earnings are expected to grow somewhat faster thanks to cost synergies from the Oppenheimer deal, as well as overall improved economies of scale.

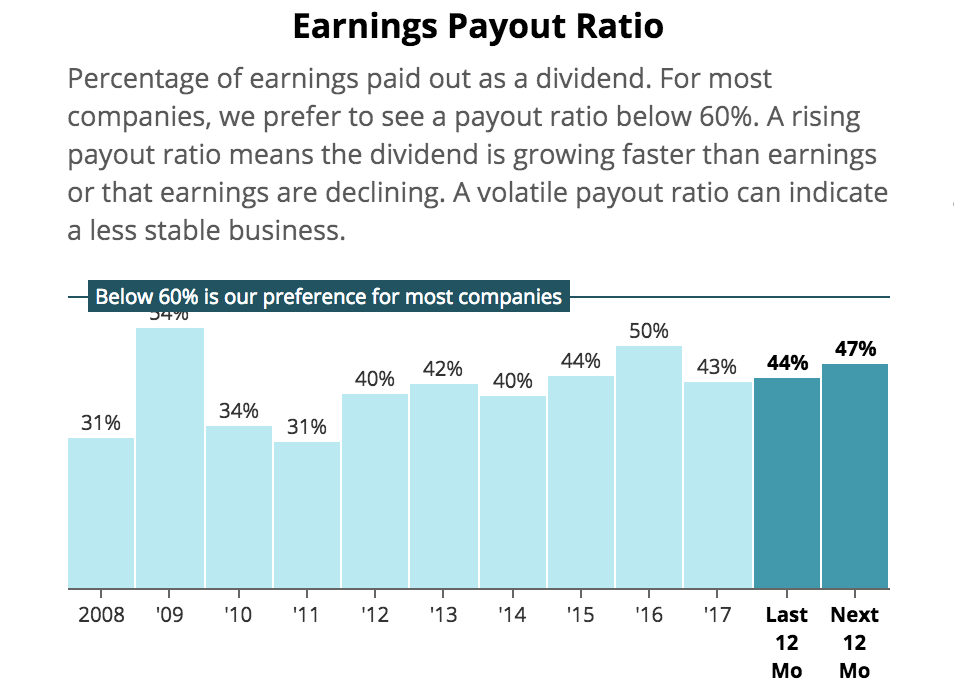

However, it should be noted that asset managers' earnings are highly cyclical due to their dependence on the health of the stock market. Fortunately, Invesco's dividend payout ratio looks reasonable, providing some safety to the dividend even if the market weakens and more significant AUM outflows strike in the next few years.

Source: Simply Safe Dividends

And don't forget that management expects the Oppenheimer deal to increase EPS and free cash flow per share in the next two years. Unless Invesco really botched its medium-term AUM projection models (which factor in continued outflows - see below), that should help keep Invesco's dividend covered by the combined firm's higher cash flow.

Source: Invesco Earnings Presentation

The other important component of dividend safety is the balance sheet since too much debt can sink a dividend even if earnings cover it. Unfortunately, Invesco's balance sheet is not overly impressive.

As you can see, the firm's leverage has been rising. S&P also recently downgraded Invesco's credit rating from A to BBB+ with a stable outlook after the Oppenheimer deal was announced.

Source: Simply Safe Dividends

The good news is that almost all of Invesco's debt is long-term fixed rate, and the company shouldn't have much trouble refinancing its debt in the coming years. As long as the Oppenheimer acquisition performs as expected, Invesco's debt load seems unlikely to threaten its dividend.

However, Invesco shareholders shouldn't expect fast dividend growth. Due to some of the secular headwinds facing the industry, Invesco's dividend growth has been slowing in recent years with the last hike being about 3% earlier this year.

And with management announcing the firm will be starting a two-year $1.2 billion buyback program to offset some of the shareholder dilution it's taking on to fund the Oppenheimer acquisition, slower dividend growth is likely to continue.

In the short to medium term, Invesco's dividend appears to remain safe. However, a lot could change over the next few years. If the stock market experiences a sustained fall, Oppenheimer underperforms, or Invesco's active funds see greater than expected outflows, then the firm's reduced financial flexibility could eventually get its dividend into trouble.

Concluding Thoughts

Invesco's 2018 crash is largely due to a perfect storm of negative factors including two market corrections, worries over the increasing popularity of passive funds, and the company's large and complex Oppenheimer acquisition.

While Invesco's dividend appears to be safe for now, and the company is still expected to generate positive revenue and earnings growth for at least several years, it's also true that Invesco is far from the top quality name in its industry.

Conservative income investors worried about capital preservation are likely better off looking elsewhere for yield. Invesco's decision to spend big and double down on this pressured industry by acquiring Oppenheimer widens the stock's range of potential outcomes.

Large acquisitions are usually dicey, and even more so when they are made to buy a business facing long-term growth challenges. Until management demonstrates the benefits of combining Invesco with Oppenheimer and improves overall asset flows, our preference as conservative investors is to watch from the sidelines.