Abbott: 47 Consecutive Years of Dividend Increases

Founded in 1888, Abbott Laboratories (ABT) is one of the world’s largest medical companies, with a portfolio of leading offerings in diagnostics, medical devices, nutritionals and branded generic pharmaceuticals. Abbott spun off its research-based pharmaceuticals business AbbVie (ABBV) in January 2013 and has four main business units today:

Cardiovascular and Neuromodulation (33% of sales, 41% of profits): medical devices to treat structural heart issues, such as stents, pacemakers, and implantable defibrillators, as well as products to monitor heart failure and blood glucose levels.

Diagnostics (26% of sales, 25% of profits): diagnostic systems and tests sold to hospitals, clinics, blood banks, labs, and physicians' offices. Includes chemical systems to diagnose cancer, cardiac diseases, fertility issues, HIV, and infectious diseases, as well as therapeutic drug monitoring and instruments to test DNA and RNA.

Nutritionals (25% of sales, 22% of profits): pediatric and adult nutritional products such as Similac, Ensure, PediaSure, and Pedialyte.

Established Pharmaceuticals (16% of sales, 12% of profits): a broad line of generic drugs sold outside the U.S. in emerging markets. Abbott's drugs treat a wide variety of conditions including pain, fever, inflammation, migraines, dyslipidemia (high cholesterol), gynecological disorders, pancreatic insufficiency (diabetes), and hypertension (high blood pressure).

Abbott’s revenues are widely diversified across segments, and the company sells more than 10,000 different products. This creates more stable and predictable cash flow compared to standalone drugmakers.

In addition to product diversification, Abbott’s business is truly global, with 65% of sales coming from outside the U.S. and 41% of revenue generated in faster-growing emerging markets where healthcare spending is outpacing the growth of GDP.

Abbott is a dividend aristocrat when adjusted for the AbbVie spin-off. The company has paid consecutive dividends for 95 straight years and raised its dividend for 47 straight years.

Business Analysis

All of Abbott’s businesses have some unique competitive advantages. Nearly 50% of the company’s total sales are made directly to consumers, for example. These products primarily reside in Abbott’s adult and pediatric nutrition segment and its branded generic drugs.

These businesses operate more like consumer packaged goods companies than traditional healthcare businesses in some ways. They benefit from Abbott’s decades’ worth of marketing spending to build up brand recognition and the firm's deep distribution relationships that help the company maintain prime shelf space where its products are sold.

The company’s extensive investments in R&D to understand consumer preferences play an important role as well. By remaining at the cutting edge of healthcare innovation, over 50% of Abbott's 2018 sales were from products introduced in the past six years, according to its annual report.

With over 130 years of operational history, Abbott has developed strong market share positions in many areas of its business. Abbott is the world’s No. 1 player in adult nutrition and is the U.S. leader in pediatric nutrition. The company’s 50 consumer nutrition brands are No. 1 or No. 2 in 25 countries. The global pediatric nutrition market is about $35 billion in size and expected to grow steadily as rising incomes in emerging markets drive demand for safe and trusted child nutrition products.

Within branded generics, Abbott has leading positions in India, Russia, and several Latin American countries. Abbott’s moat in this business is driven in part by the company operating in largely oligopolistic business segments. There are generally just three or four major players it must compete with in most markets, reducing pricing pressure.

In fact, Abbott’s generic drugs business is 100% focused in overseas markets. Since many of these regions have weak distribution networks, the company has a big advantage thanks to its strong relationships with local pharmacies and physicians' offices, where trusted brands are critical to gaining and maintaining market share.

Abbott’s solid brand recognition allows it to generate healthy margins, and because none of its drugs are patented, it doesn’t face patent expiration risk and the kind of ferocious competition that is a major concern for most patented drug makers.

The company’s medical devices and diagnostics businesses are a bit more challenging to maintain because they require heavier R&D investments to adapt to the industry’s faster pace of change. However, Abbott has still managed to hold leading market share in numerous key categories, such as LASIK, blood screening, cataract surgery, and amino-acid diagnostics.

New entrants have a hard time challenging Abbott because of the high amount of government regulation in these markets (e.g. pharmaceuticals, medical devices), the steep investment costs needed to develop competitive products (Abbott invests 6-8% of its revenue in R&D), the need for global distribution networks, and the protection provided by patents and trademarks.

Through organic reinvestment or bolt-on acquisitions, Abbott can also quickly adapt to changing healthcare trends to remain relevant, plugging new products into its extensive distribution network.

Acquisitions have long played a role in Abbott's long-term growth strategy. The company's CEO Miles White, who has been with Abbott for 35 years, has an above average track record on the 30-plus deals that have taken place during his tenure.

One of his best deals came in 2001 when Abbott paid about $7 billion to acquire a division from chemical company BASF that included its treatment for rheumatoid arthritis. As you might have guessed, this blockbuster drug is now called Humira and has fueled much of AbbVie's success (spun off from Abbott in 2013).

More recently, Abbott made headlines with its 2017 acquisitions of St. Jude Medical for $23.6 billion (the company's largest deal ever) and diagnostics company Alere for $4.5 billion.

St. Jude helped Abbott's medical device business achieve the same level of market leadership the company holds in its other businesses, providing Abbott with a slew of cardiovascular-related devices. Abbott now has a presence in nearly every aspect of cardiovascular care with No. 1 or No. 2 positions across numerous large and high-growth cardiovascular device markets.

The deal also put Abbott into a new market – neuromodulation – with breakthrough products that can make a life-changing difference for people with chronic pain, as well as movement disorders, such as Parkinson’s disease.

Alere was acquired to significantly advance Abbott's global diagnostics presence. The company meaningfully broadened Abbott's point-of-care testing business, making it the world's leading diagnostics player in this fast-growing market.

Bulking up its scale and breadth of products makes Abbott a more attractive partner for cost-conscious hospitals and health care providers, which generally prefer dealing with a small number of large vendors.

Abbott's management team has also demonstrated sound judgement with divestitures. For example, in February 2015 Abbott sold its developed market generic pharmaceuticals business to Mylan (MYL) in a $2.3 billion deal. Generic drugs are a very large market, but their prices and profitability have come under pressure in developed markets. This deal enabled Abbott to focus on higher margin businesses with stronger moats.

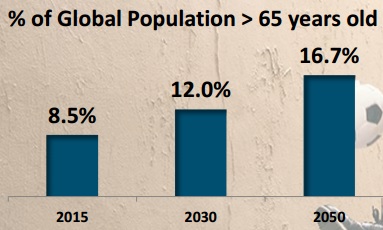

Looking ahead, Abbott’s growth runway appears long, courtesy of the aging global population. From cardiac monitors (used to detect irregular heartbeats) to deep-brain electronic stimulators (used to slow the progress of Parkinson disease), Abbott's portfolio has many products needed to combat aging-related diseases.

Source: Abbott Investor Presentation

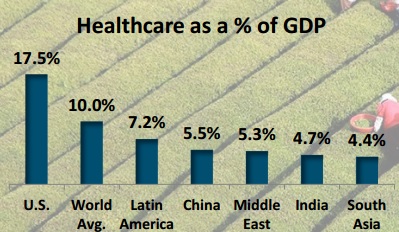

In addition, Abbott's strong presence in some of the world’s fastest growing economies, where healthcare spending remains below the global norm, means that its diversified business lines have potential to generate steady growth for decades.

Source: Abbott Investor Presentation

Abbott's earnings and dividend have grown at a low double-digit pace since the AbbVie spin-off, and a similar rate of growth seems likely to continue. Abbott has also done a great job paying down debt following its acquisitions of St. Jude and Alere, strengthening its balance sheet, solidifying its healthy BBB+ credit rating, and providing the company with more flexibility for future deals.

But despite Abbott’s numerous attractive qualities, income investors need to be aware of several risks.

Key Risks

Like all medical companies, Abbott faces a few key risks.

Due to its heavy global diversification, the company is exposed to currency risk in any given year. A rising U.S. dollar hurts Abbott's reported sales and earnings growth rates in international markets. Fortunately, currency fluctuations tend to cancel out over time and don't impact the company's long-term outlook, but investors should be aware of the noise they can cause any given quarter.

A more fundamental risk is that while the company operates as one of the big four medical device makers (chief rivals are Stryker, Medtronic, and Johnson & Johnson), which limits competition and helps boost margins, each of its competitors is well capitalized and has an excellent track record of innovation over time.

In other words, if a rival comes out with a revolutionary new device, it can win market share quickly and force Abbott to go back to the drawing boards to improve its own product offerings.

But due to concerns over rising costs, there is also risk that healthcare providers will move to multi-line contracts, meaning bulk purchases of medical equipment that their patients need.

Since Abbott’s medical prowess is mainly in cardiac and diabetes equipment, this could give it a competitive disadvantage. Even the St. Jude acquisition won’t help offset this risk much because that purchase was mainly designed to strengthen its cardiac device business (although it did add neuromodulation for pain control as well).

Governments and private payers are also desperate to drive down healthcare costs. This can result in price controls and regulation in some countries (mostly outside the U.S.) and has meant reduced pricing power for some of the company's biggest segments in recent years, especially medical devices.

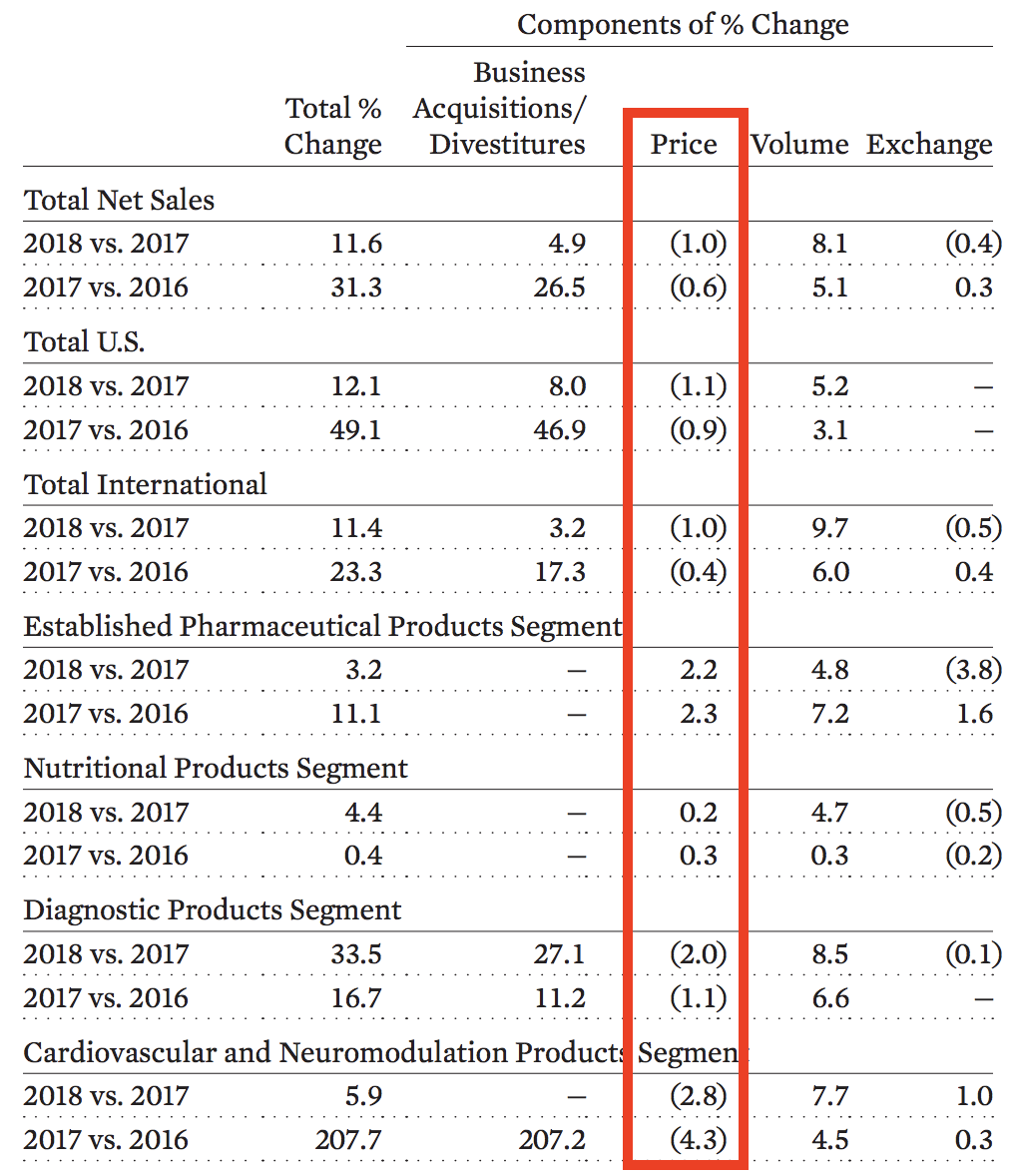

Fortunately, as you can see below, strong volume increases have allowed Abbott to more than offset price declines to maintain steady top line growth.

Source: Abbott Annual Report

Just keep in mind that the U.S. is a major market for Abbott, and in America we have frequent proposals to slash healthcare costs including potentially via a single-payer healthcare option ("Medicare-For-All" is a great example). While such a major change seems unlikely to occur, if the U.S. moved to a government-run healthcare system, then virtually all healthcare companies would likely face major pricing pressure.

Even without a single-payer system, the healthcare industry is rapidly consolidating in order to achieve larger economies of scale so that health insurance providers and healthcare systems can squeeze greater discounts from medical suppliers like Abbott.

Finally, in terms of company-specific risks, Abbott's acquisitive growth strategy needs to be discussed. The company's large deals to acquire St. Jude and Alere stretched Abbott's balance sheet, will significantly affect its future, and got off to somewhat rocky starts.

Soon after Abbott's acquisition offer in early 2016, Alere came under investigation for corrupt sales practices in international markets, as well as some accounting issues. Alere failed to file financial statements, had to recall a major product because it didn't work, and lost Medicare reimbursement. Abbott wanted to back out of its agreement to acquire the business but ultimately settled to complete the deal at a somewhat lower price.

Meanwhile, St. Jude, the company's largest acquisition ever, received a safety warning from the Food and Drug Administration about its heart pacemaker devices, which connect to monitors and mobile devices over the internet. A voluntary recall was issued for 465,000 of its "smart" pacemakers to have them receive firmware updates to keep them safe from hackers.

Simply put, large acquisitions such as St. Jude Medical and Alere create financial and execution-related risks. They represent major capital allocation bets, and management’s strategic rationale needs to be proven right. Abbott has done a great job paying down debt used for those deals to maintain a strong balance sheet, but it will likely take several years to gauge the success of both acquisitions.

Overall, many of Abbott’s key risks are balanced out thanks to the company’s cash flow diversification and numerous opportunities for long-term growth (i.e. the company isn’t overly dependent on any single thing to go right).

Each of Abbott’s four unique segments has different risks and growth opportunities, and the company’s geographical diversification reduces overall regulatory risk in any given market as well. While the healthcare industry's overall risk profile is complex, Abbott's size, track record, and diversification appear to make it one of the lower-risk options in the space.

Closing Thoughts on Abbott Laboratories

Abbott has proven itself to be one of the best long-term dividend growth stocks over the years, which is backed up by the company's impressive track record of paying consecutive quarterly dividends since 1924. And Abbott has raised its dividend for 47 straight years, putting it among the elite of all U.S. dividend payers.

With that said, management needs to deliver meaningful value from Abbott's major acquisitions of St. Jude and Alere. However, the company deserves the benefit of the doubt, given the firm's solid track record on M&A growth over the decades.

Overall, Abbott's shareholder-friendly corporate culture, highly diversified business model, strong balance sheet, and recession-resistant cash flow appear to position the company to take advantage of several important secular trends, especially in emerging markets. Meanwhile, Abbott's dividend appears to remain on very solid ground while offering close to 10% annual growth potential, making it an appealing candidate for long-term dividend growth investors.