Archer-Daniels-Midland: Uninterrupted Dividends Since 1931

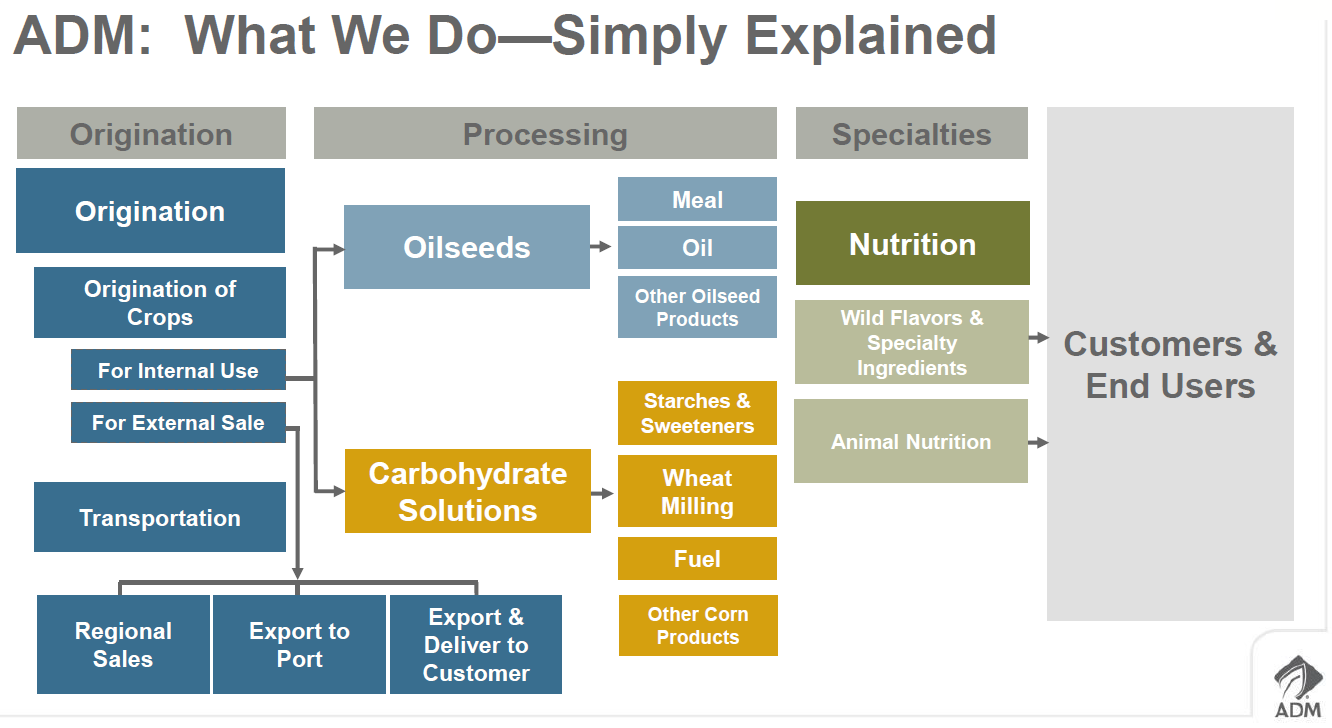

Founded in 1898, Archer Daniels Midland (ADM) generates most of its revenue from procuring, transporting, and processing corn, oilseeds, wheat, and other commodities which are turned into products for food, beverage, animal feed, chemical, and energy uses around the world.

The firm's end products include vegetable oil, protein meal, flour, corn sweeteners, starch, ethanol, and other food and feed ingredients.

Source: ADM Investor Presentation

ADM is gradually diversifying away from low-margin, capital-intensive businesses like corn processing and into higher-margin areas such as nutrition. ADM entered the nutrition business in 2014 and believes this division has potential to generate 25% of firm-wide operating profits by 2024.

The company organizes its business into three segments:

Ag Services &Oilseeds (75% of sales, 60% of operating profit): ag services utilities ADM's global grain elevator and transportation networks to efficiently buy, store, clean, transport, and resell agricultural commodities as food, feed ingredients, and raw materials for the ag processing industry. The oilseeds business originates, transports, crushes, and processes soybeans and other soft seeds into protein meals and oils used in food, animal feeds, renewable fuels, and industrial products.

Carbohydrate Solutions (16% of sales, 24% of operating profit): converts corn and wheat into starches and sweeteners (10% of firm-wide sales) and bioproducts (5%). Sweeteners include high-fructose corn syrup (HFCS), which is used in products such as soft drinks, cereals, and bread because it is more affordable than sugar. Starches are also used in food production and as feedstocks for ADM’s bioproducts operations (ethanol).

Nutrition (9% of sales, 16% of operating profit): consists of human nutrition (specialty ingredients and flavors used by food manufacturers), animal nutrition (antibiotics, probiotics, enzymes, supplements, etc., for healing and preventing animal diseases), and health & wellness (food safety, personalized nutrition / genomics, biomaterials, etc.).

Approximately 45% of the firm's revenue is from the U.S., with most of the rest coming from Europe, the Cayman Islands, and other foreign countries.

Archer-Daniels has paid uninterrupted dividends since 1931 and raised its annual dividend for more than 40 consecutive years, making it a dividend aristocrat.

Business Analysis The basic investment thesis for food companies such as ADM is simple: everyone has to eat.

Demand for corn-based products and meat, which is highly grain intensive (that's what most livestock is fed), will likely rise over time as the global population expands and emerging markets' middle classes increasingly consume more Western-style diets.

Simply put, ADM's core operations – procuring, storing, processing, and selling agricultural commodities – solve a timeless problem and have staying power.

ADM's core business is also very capital intensive, creating somewhat high barriers to entry. For example, the company has the largest grain terminal and shipping network in the country and maintains hundreds of processing plants and storage facilities around the world.

These capabilities allow ADM to typically be the lowest cost and fastest provider of its commodities and processed products to many customers’ facilities, where it delivers directly.

Replicating ADM’s physical footprint and logistical knowledge, as well as its 1,400 semi-trailers, 28,000 railcars, 2,300 barges, and container ships used to transport its products, would be very difficult. With razor-thin operating margins in this commodity industry, there is no room for inefficiencies.

While ADM's existing businesses will continue generating cash flow for a long time to come, the company’s management team recognizes that the company’s high sensitivity to external risk factors isn’t ideal.

Drought conditions, currency exchange rate volatility, ethanol regulation changes, volatile crop prices, and trade wars are just some of the uncontrollable factors that ADM's core business can face.

As a result, ADM is gradually shedding low-return operations and moving into areas of higher value in an attempt to structurally improve its profitability, reduce its capital intensity, and remove some of the price sensitivity of the business.

Starting in 2012, management initiated a long-term turnaround plan that involved two main strategies. First, ADM would sell off non-core businesses (i.e. those with the lowest margins) and reallocate the capital into acquiring a number of higher-margin businesses, specifically those in specialty foods products.

During this period, ADM divested about $2.5 billion in businesses that didn't fit its portfolio and invested around $7.5 billion in creating its Nutrition segment. Major deals included a $3 billion purchase in July 2014 of natural ingredient company Wild Flavors and a $1.8 billion acquisition of animal nutrition solutions business Neovia in January 2019.

Unlike agricultural processing and transportation, these businesses enjoy higher customer loyalty due to the unique value they provide, have low capital intensity and stronger profitability, and deliver more predictable growth. They also expand ADM's addressable market.

Source: ADM Investor Presentation

Nutrition accounted for 10% of ADM's 2018 operating profits, and management believes this business has potential to account for at least 25% of the firm's profits by 2024. Importantly, ADM believes it has all of the technology it needs to get there already, so further large acquisitions are not part of the growth plan.

Overall, ADM's gradual business transformation looks appealing, and its set of hard assets is very difficult to replicate. When combined with management's conservative capital allocation plans, the company has been able to increase its dividend for more than 40 consecutive years, despite its cyclicality.

However, the business still depends on a number of uncontrollable macro factors.

Key Risks While ADM is generally a fundamentally solid income stock, there are still several concerns for investors to consider.

First, the firm operates in a highly competitive field. ADM's core business essentially acts as a middleman between farms and consumers, so it does not have much pricing power.

As a result, the company's short-term earnings are driven mostly by factors outside of its control, including the weather, commodity prices (especially the prices of soybeans, corn, and oilseeds), shifting consumer food preferences, and government agricultural policies.

Management is working to reduce ADM's exposure to businesses with the greatest sensitivity to uncontrollable macro factors (including shopping its ethanol operations), but this volatility will likely always be part of the company.

A longer-term risk is U.S. agricultural policy, specifically corn subsidies and ethanol mandates, which have resulted in corn becoming ADM's largest and most important product over time.

According to a 1995 report by the libertarian think tank Cato Institute:

“ADM has cost the American economy billions of dollars since 1980 and has indirectly cost Americans tens of billions of dollars in higher prices and higher taxes over that same period. At least 43 percent of ADM’s annual profits are from products heavily subsidized or protected by the American government. Moreover, every $1 of profits earned by ADM’s corn sweetener operation costs consumers $10, and every $1 of profits earned by its bioethanol operation costs taxpayers $30.”

A lot has changed since 1995, including ADM’s mix. However, government subsidies are still a help for the company. Any future reversal of these subsidies could leave ADM in an uncomfortable position, having to once again restructure parts of its business model.

ADM's long-term growth strategy provides a final risk to consider in that management may be stepping outside its circle of competence. The company's historical expertise is in commodity foods and logistics, not necessarily the specialty nutrition businesses it's purchased in recent years.

Management is banking on these nutrition businesses improving ADM's margins and delivering more predictable earnings. Given their importance to ADM's long-term thesis, it's important that the firm can find success in these markets.

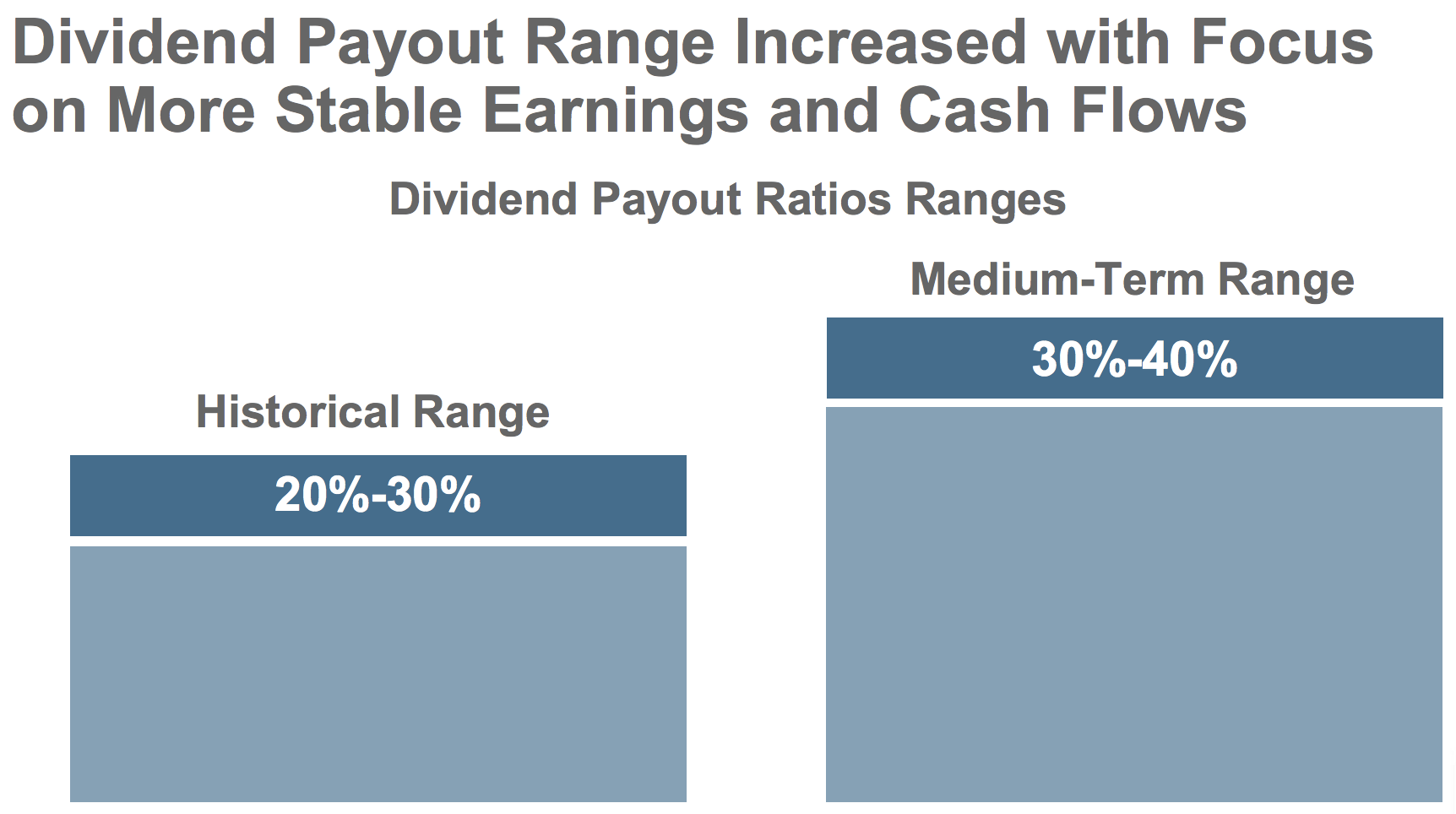

After all, the company's earnings are virtually unchanged compared to a decade ago. With ADM's payout ratio at the high end of management's target range, which already reflects the more stable cash flow the firm expects from its mix shift, low single-digit dividend growth seems likely unless earnings growth accelerates.

Source: ADM Investor Presentation

Thus prospective investors need to ask themselves if the company's slightly above average dividend yield is worth their patience when dividend growth is likely to be barely ahead of inflation over the next few years.

Overall, ADM’s ties to macro factors such as global crop prices make strong and sustained earnings and dividend growth more challenging. The company's move into specialty nutrition products is appealing, but it will take time for these businesses to become more meaningful drivers.

Closing Thoughts on Archer Daniels Midland ADM, despite its dividend aristocrat status, depends on a number of factors outside of the company’s control – corn and soybean prices, ethanol regulations, government subsidies, trade wars, and long-term consumer food trends.

While management appears to be making the right capital allocation moves to gradually diversify the company into higher-returning areas that are less susceptible to swings in commodity prices, these actions also suggest that management is less optimistic about some of ADM's existing operations.

Simply put, ADM's path to long-term profitable growth probably won't be linear. On the bright side, the company's dividend appears to remain very safe, the balance sheet is in great shape, and the firm's capital allocation policy remains conservative with no major M&A expected going forward.

However, investors considering the stock need to acknowledge the company's sensitivity to macro factors and be content with a moderate pace of dividend growth until ADM hopefully begins delivering more sustainable earnings growth when its nutrition segment is larger.