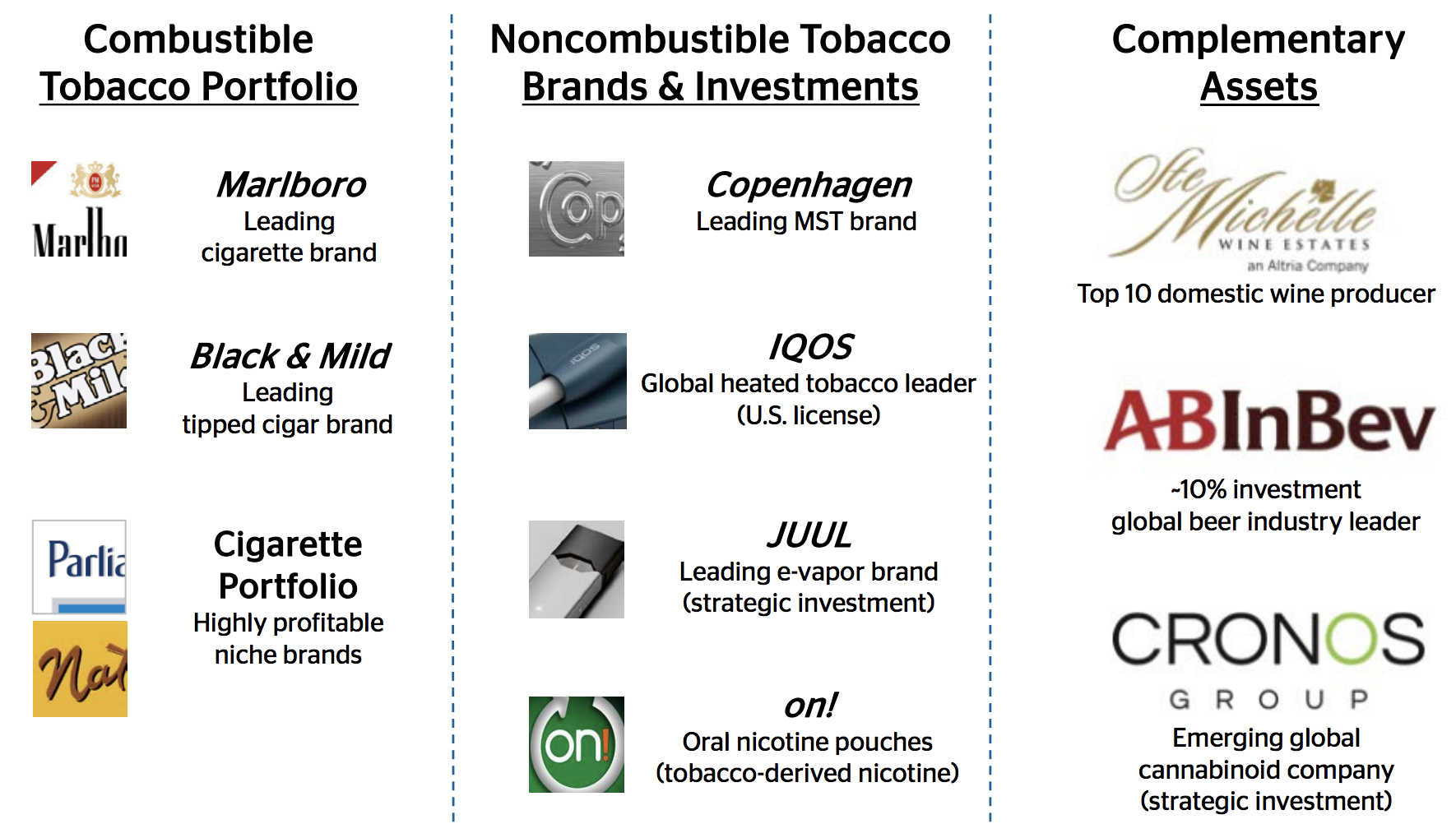

Founded in 1919, Altria (MO) is America’s largest tobacco company. The business split into three separate firms in 2007 and 2008 (Altria, Phillip Morris International, and Kraft), with Altria retaining all domestic tobacco operations. Altria has exclusive U.S. rights to sell cigarettes primarily under the Marlboro, Parliament, Virginia Slims, and Benson & Hedges brands.

The company also markets cigars, chewing tobacco, and table wines and owns a 10% stake (valued at about $15 billion) in Anheuser-Busch InBev (BUD), the world’s largest beer company.

Source: Altria Investor Presentation

In recent years, Altria has invested into non-combustible reduced-risk products to adapt its long-term business model for an eventually smoke-free world. In late 2018, the company announced its largest diversification efforts to date:

A $1.8 billion investment for 45% of cannabis company Cronos (CRON)

A $12.8 billion investment for 35% of vaping company Juul Labs

Altria also has an exclusive license to sell Philip Morris's heat-not-burn tobacco product IQOS in the U.S.

Overall, Altria’s mix remains dominated by its core cigarette business, which accounts for nearly 90% of total sales and 85% of operating income, with almost all of the rest coming from its smokeless division (dipping tobacco). Wine represents just 3% of sales and 1% of operating income.

Adjusted for its 2007 and 2008 spinoffs, Altria has increased its dividend for 50 consecutive years.

Business Analysis

“It costs a penny to make. Sell it for a dollar. It’s addictive. And there’s fantastic brand loyalty.”

This quote from Warren Buffett about the advantages of the tobacco industry explains why Altria has been such a great high-yield dividend stock for so long.

Starting with brand loyalty, the company’s Marlboro brand has been the largest-selling cigarette brand in the U.S. for more than 40 years and commands over 40% market share today.

Marlboro accounts for more than 80% of Altria's overall smokeable volumes and competes in the premium-price category. Studies have shown that premium brand smokers are less likely to quit, further strengthening Altria's brand equity.

Coupled with the addictive nature of nicotine, Altria has historically enjoyed excellent pricing power to offset the 3% to 4% annual volume declines in cigarettes that have been the long-term industry trend in America.

Meanwhile, more of America's 40 million adult smokers have moved to the e-vapor category, driving an acceleration in the U.S. cigarette industry volume decline rate.

As you can see, in 2019 shipments fell at their fastest rate in at least five years, and going forward Altria expects the annual decline rate to remain between 4% and 6% through at least 2023.

Source: Altria, Simply Safe Dividends

With about 85% of its operating income derived from combustible tobacco products, trends in Altria's core cigarette business will remain the biggest driver of the company's ability to pay its dividend for the foreseeable future.

Unfortunately, unlike Philip Morris which has invested more than $6 billion since 2008 to develop its own smoke-free products, Altria was largely caught off guard by the rise of vaping and other nicotine products with perceived lower risk.

In a seemingly desperate move to respond to mounting long-term headwinds for cigarettes, in late 2018 the company invested $14.6 billion to buy minority stakes in Juul, the leading U.S. vaping company, and Cronos, a cannabis business.

Altria believes these businesses, along with its U.S. license to sell Philip Morris's IQOS heat sticks, will buoy its long-term growth prospects as more smokers choose noncombustible products with the potential to reduce harm.

In fact, the U.S. cannabis market has potential to exceed $25 billion by 2025 (for context, the U.S. tobacco market is worth around $100 billion), and over half of U.S. adult smokers have already tried e-vapor products, according to Altria.

Management hopes Juul and Cronos can leverage Altria's massive distribution network (dominant shelf space at many retailers), well-known brands, and extensive experience working with regulators to help them establish leading positions in their markets.

If all goes as planned, management expects Altria's adjusted EPS to grow 5% to 8% between 2020 and 2022 while the company maintains a reasonable 80% payout ratio to keep its 50-year dividend growth streak alive.

However, investors remain concerned about the dynamic U.S. tobacco market.

Key Risks

Like its big tobacco peers, Altria has historically paid out the bulk of its earnings as dividends, reflecting the high margins, recession-resistant demand, and slow pace of change enjoyed by the industry.

However, compared to smokers in many other countries, Americans have shown a greater willingness to try smoke-free products, driven in part by more accessible and affordable offerings, plus the aging population.

If the movement away from cigarettes accelerates and causes the industry's favorable price elasticity to break down, then Altria could find itself under pressure.

Besides the rise of alternative products, increased scrutiny from regulators further muddies the tobacco industry's outlook. Since 2009, the U.S. Food and Drug Administration (FDA) has regulated cigarettes and smokeless tobacco products.

The FDA has the power to set standards that "make tobacco products less deadly, less addictive, and less appealing." Over the last decade, adult smoking rates have fallen from nearly 21% to 14%, but the FDA still isn't satisfied.

Regulators continue expressing desires to make cigarettes less addictive, and excise taxes on cigarettes continue increasing, accounting for over 40% of the retail price of cigarettes. (Higher taxes raise cigarette prices and reduce demand.)

Fortunately, the regulatory process is extremely long, so any phased-in nicotine restrictions aren’t likely to hurt Altria over the short term. For example, British American Tobacco (BTI) estimates that the FDA's proposed menthol ban would likely take about nine years to go into effect.

Regardless, investors need to watch future developments in the U.S. cigarette industry to ensure this business remains a predictable cash cow for Altria.

After all, the company's financial flexibility is somewhat limited following Altria's pricey acquisitions of Juul and Cronos, which diversified its long-term growth drivers but also saddled the company with debt.

Altria was in great shape prior to making these deals, helping it maintain an investment-grade credit rating from Standard & Poor's. However, neither of these businesses is likely to generate meaningful cash flow for the company for a long time, and Altria is unlikely to tolerate higher leverage.

Combined with its high payout ratio, which only leaves about $1 billion of free cash flow after paying dividends each year, Altria doesn't have much flexibility if it needs to once again adapt its portfolio of reduced-risk products.

Altria now has exposure to e-cigarettes (Juul), heated tobacco (IQOS), and cannabis to help hedge its bets, but no one knows which nicotine delivery systems will ultimately hold the greatest market share in the future.

For example, the FDA appears ready to crack down on or even ban the vaping industry, issuing an existential threat to the category following rampant teen use. In response to these developments Altria wrote down the value of its Juul investment by $4.5 billion less than a year after its acquisition, demonstrating it paid too much for its stake.

crack down on or even ban the vaping industry

Given all of these uncertainties, in August 2019 Altria announced it was in talks with Philip Morris about combining their businesses. Combining forces would improve Altria's regulatory, geographical, and product diversification while also strengthening its balance sheet.

The companies eventually walked away without a deal, but this engagement demonstrates the urgency management feels to better position the firm for the future. Altria investors need to monitor management's capital allocation priorities going forward, especially as more focus is put on stabilizing Juul. (Altria's Chief Strategy and Growth Officer was appointed as Juul's new CEO in 2019.)

Closing Thoughts on Altria

Despite more than 50 years of declining smoking rates in America, Altria has delivered as a reliable dividend growth investment. Management's ability to adapt to the tobacco industry's various challenges, along with Altria's portfolio of premium cigarette brands, have allowed the company to raise prices fast enough to offset volume declines and keep its earnings (and dividend) growing.

Altria's large investments in Cronos and Juul mark the company's latest effort to adapt to a future where cigarette smoking rates will continue falling, perhaps at an accelerated rate as cannabis, vaping, and heated tobacco products grow.

However, the company paid a rich price for these debt-funded investments, none of which is certain to pay off. Altria was late to the scene to capitalize on these trends in a meaningful way, forcing management to pay dearly for what could ultimately prove to be necessary long-term product diversification.

Overall, Altria still appears to be a reasonable long-term income investment as part of a well-diversified portfolio. However, the company's risk profile has become more complex.

Investors need to continue monitoring regulatory developments and U.S. cigarette volume declines, which remain the most important drivers behind Altria's core business and dividend safety profile for at least the next few years.