EQT Midstream Partners, LP (EQM) is a master limited partnership formed by EQT Corp (EQT) to own, operate, and expand its gas gathering, storage, processing, and transportation assets in the Marcellus and Utica shale regions of Pennsylvania, West Virginia, and Ohio. The firm's assets provide midstream services to EQT, other energy producers, and utilities to support energy development and production.

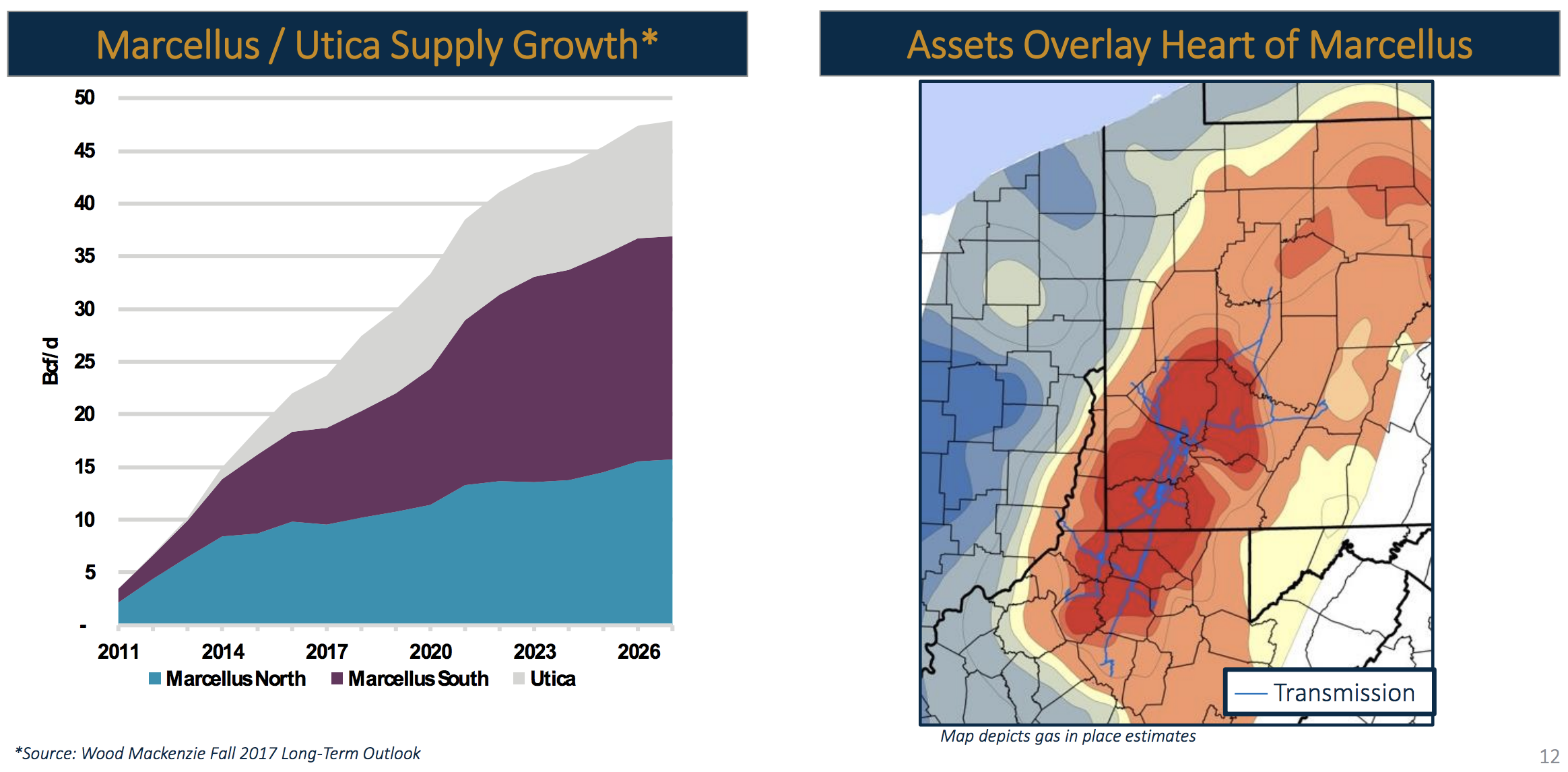

The combined Marcellus and Utica region is the largest and lowest cost gas formation in the U.S. and is expected to see very strong production growth over the coming decades. Today EQT Midstream is the third largest transporter of natural gas in America and owns:

950 miles of regulated interstate gas pipelines

2,130 miles of high- and low-pressure gathering lines

43 billion cubic feet of storage capacity

140 miles of freshwater pipelines (water is used in fracking oil & gas wells)

Source: EQT Midstream Investor Presentation

In 2017, EQT Corp acquired Rice Energy for $6.7 billion to become the largest U.S. gas producer. That acquisition also brought with it Rice Midstream Partners which was Rice Energy's own midstream MLP. Rice Midstream Partners essentially served the same purpose EQT Midstream does for EQT Corp.

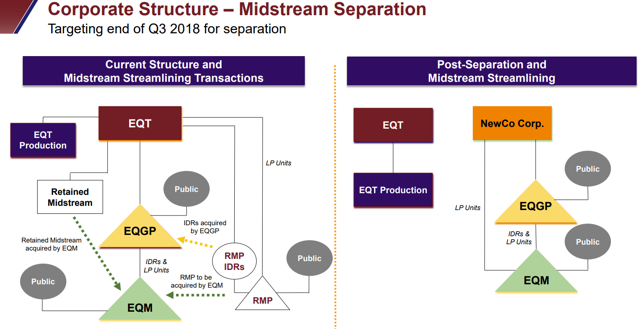

In early 2018, EQT Corp announced a major corporate restructuring meant to better focus its two different business lines (upstream and midstream) and simplify its structure.

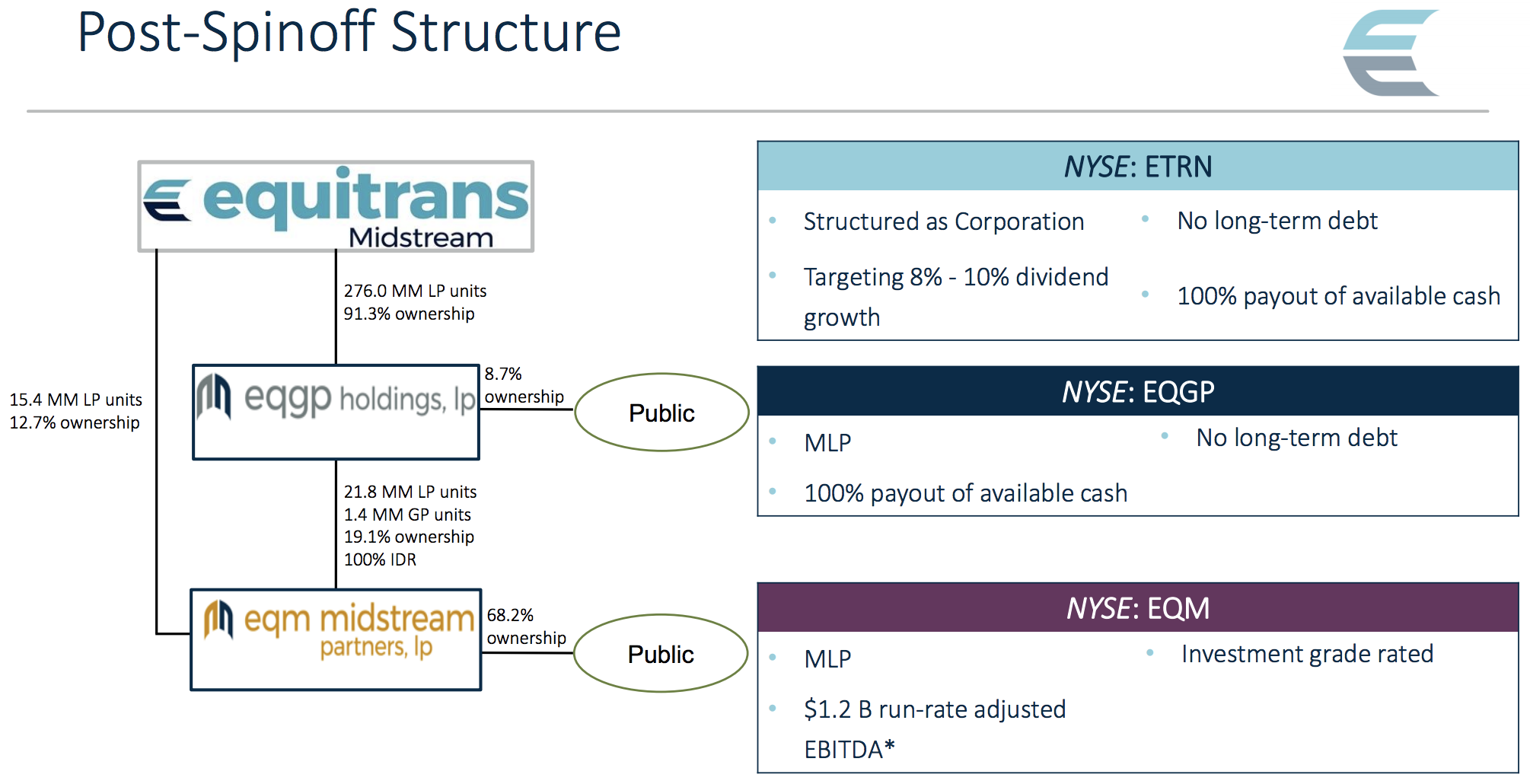

Specifically, EQT would spin-off a new corporation called Equitrans Midstream (ETRN) designed to separately own its midstream assets, including its stakes in EQM Midstream and its general partner EQT GP Holdings (EQGP).

Equitrans Midstream began trading on November 13, 2018, and is designed to pay out 100% of its distributable cash flow as a dividend that grows at 8% to 10% per year.

Source: EQT Midstream Investor Presentation

As part of restructuring, EQT Midstream purchased Rice Midstream in a $2.4 billion all-stock deal. The MLP also would pay $1.15 billion (mostly debt-funded) and issue 5.9 million units to acquire the remainder of EQT Corp's midstream assets, consisting mostly of gas gathering infrastructure in Ohio.

Finally, EQM would buy 25% of Gulfport Energy's (GPOR) Strike Force Gathering system for $175 million. This was the part of the Ohio system that EQT Corp didn't already own.

Meanwhile, EQT GP Holdings would pay $970 million and 36.3 million units to acquire Rice Midstream's incentive distribution rights, or IDRs. These grant it up to 50% of Rice Midstream's (and now EQT Midstream's) marginal cash flow as it grows it distributions over time.

On May 23, 2018, EQT Midstream closed on the acquisition of Rice Midstream, and on October 1 it officially bought EQT Corp's Ohio gathering assets.

There are a lot of moving parts here, but as the graphic below shows, an important goal of these actions is actually to reduce organizational complexity.

Source: EQT Midstream Investor Presentation

Business Analysis EQT Midstream was originally designed to raise external capital (debt and equity) from income investors attracted to its generous and fast-growing distribution. The firm would use those proceeds primarily to acquire cash-generating assets dropped down from EQT Corp. The firm's payout would be supported by a stream of highly stable and recurring cash flow that was insensitive to commodity price volatility.

EQT Midstream's cash flow is underpinned by long-term "take-or-pay" contracts. Pipelines enjoy an average contract duration of 15 years, and gas gathering deals are locked down for an average of eight years. Approximately 93% and 45% of gas transmission and gas gathering contracts are volume committed, respectively.

In other words, EQT Corp (as well as third-party gas producers) reserve capacity on the EQT Midstream's systems, and the MLP gets paid regardless of the volume of gas that's actually shipped.

Around 80% of the firm's contracts are with investment grade counterparties, meaning a low risk of default risk even if energy prices crash again. And some of its newest contracts are actually for 20 years, ensuring cash flow predictability remains strong.

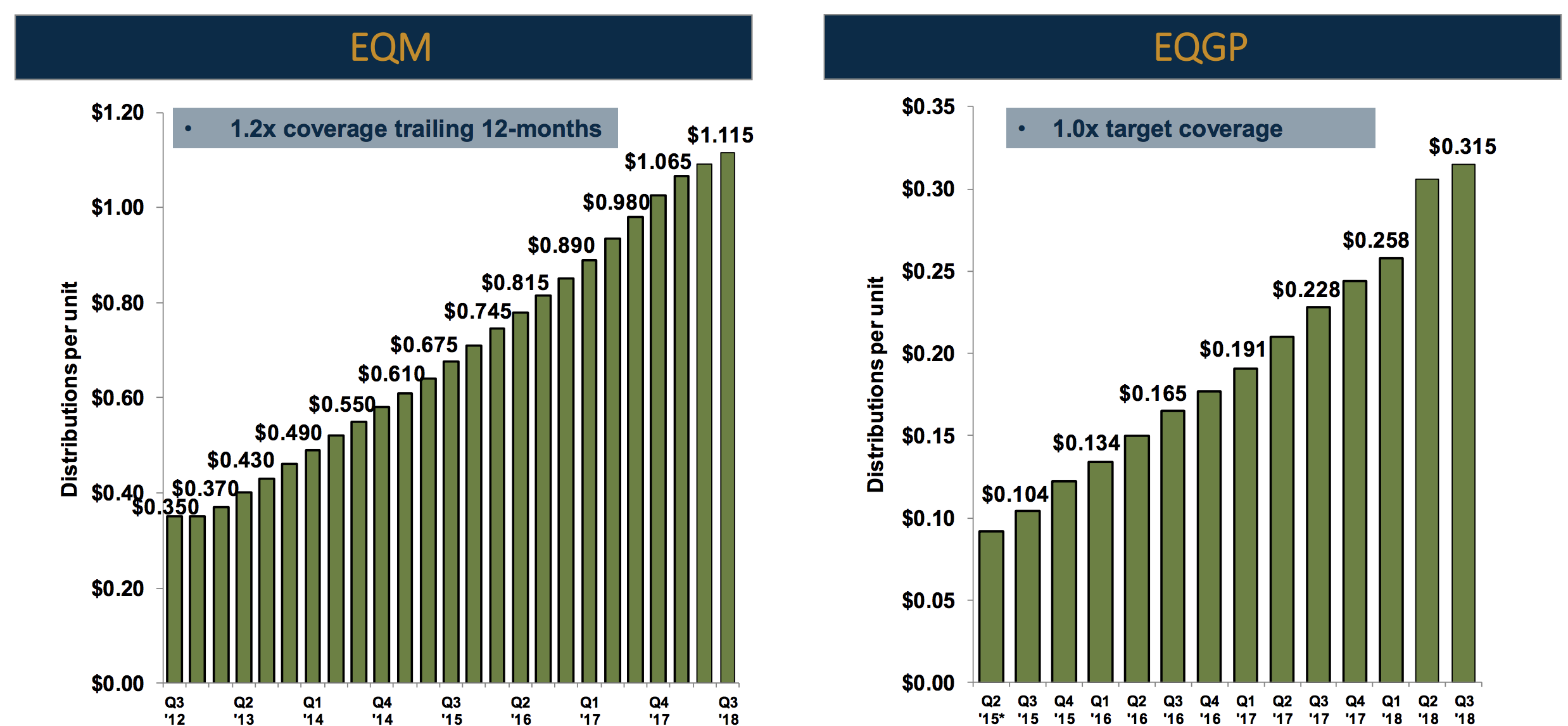

Thanks to the firm's stable cash flow profile, EQT Midstream, as well as its general partner EQT GP Holdings, have delivered impressive payout growth at some of the fastest growth rates in the industry (over 20% per year and on a quarterly basis), even during the crash in oil and gas prices between mid-2014 and early 2016.

Source: EQT Midstream Investor Presentation

More importantly, that distribution growth has not come at the cost of payout safety. Historically, EQT Midstream Partners has maintained a distribution coverage ratio of about 1.3, which is the equivalent of about a 77% payout ratio. Given the steady cash flow this type of business generates, that's a reasonably healthy level.

The Rice Midstream merger did lower EQT Midstream's distribution coverage ratio to 1.2 on a trailing 12-month basis due to equity dilution (more on that later), but the payout remains covered by distributable cash flow.

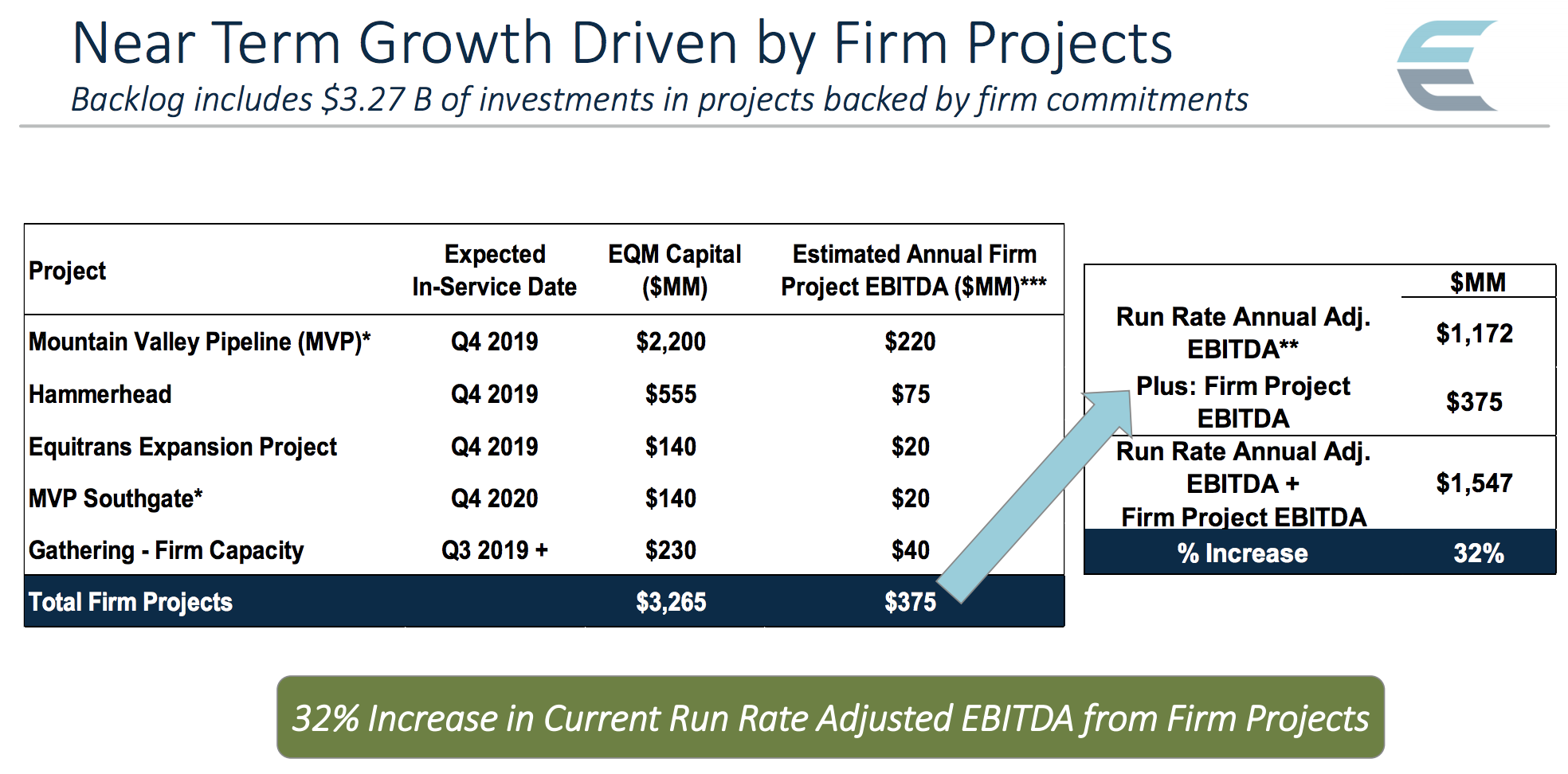

EQT Midstream aspires to raise its distribution coverage ratio to safer levels in the future thanks to its collection of organic growth projects, which currently amount to $3.3 billion in expansion opportunities.

By the end of 2019 management expects these projects to deliver 32% growth in cash flow, and by 2021 additional projects coming online should boost cash flow by 54% from 2018's full-year levels, assuming all goes as planned.

Source: EQT Midstream Investor Presentation

Unlike some struggling MLPs, EQT Midstream does not appear to be in a liquidity trap, meaning it's still able to profitably grow without putting undue financial strain on the business. A key reason is the firm's strong balance sheet (investment grade credit rating), reasonable maximum leverage target of 3.5 to 4.0, and $3 billion credit facility.

With about $3 billion in current debt, this means that EQT Midstream can safely borrow up to several billion dollars more without exceeding management's long-term leverage target.

In other words, EQT Midstream will be able to effectively self-fund its organic growth projects with only low cost debt and retained cash flow. The MLP sees no need to issue equity for "the foreseeable future."

Here's what management stated on EQT Midstream's last earnings call:

"We are currently forecasting a $1.8 billion of adjusted EBITDA in 2021 which is more than 50% higher than our current run rate adjusted EBITDA up about $1.2 billion. Importantly we can fund this steep EBITDA ramp through the combination of retained cash flow and debt with no need to access the equity markets for the foreseeable future."

Beyond 2021, EQT Midstream is likely to continue to see strong growth thanks to the large-scale energy boom America is currently enjoying.

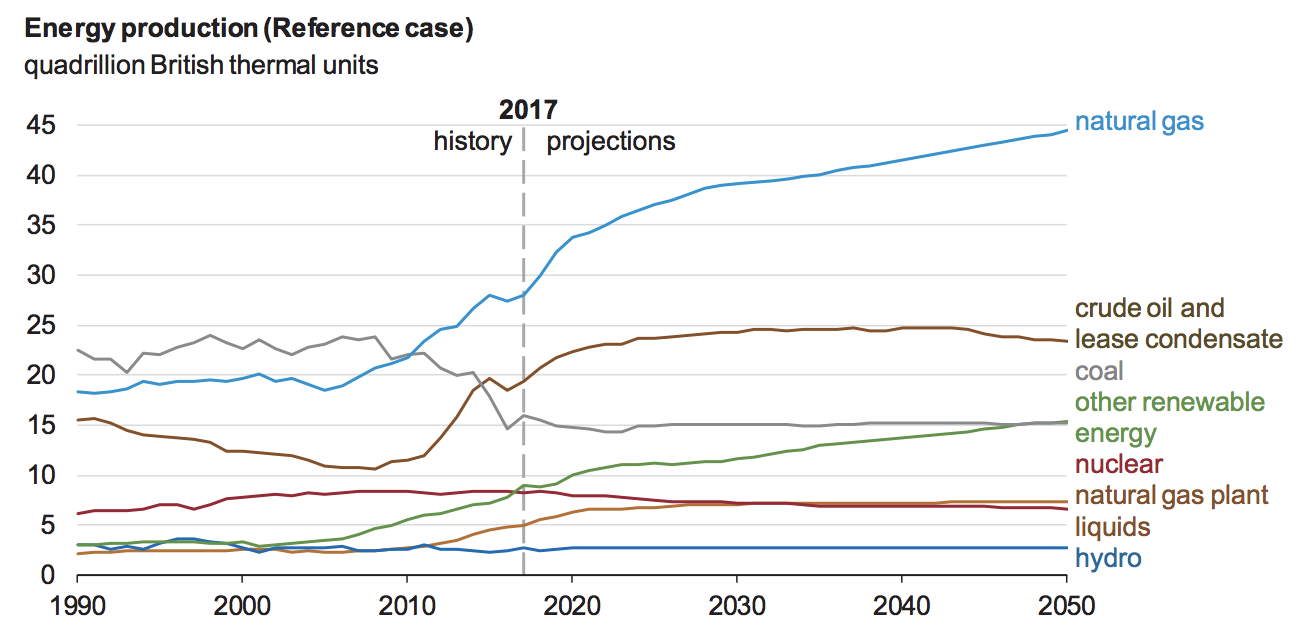

U.S. natural gas production is expected to continue rising through at least 2050, per the U.S. Energy Information Administration, mostly driven by the Marcellus/Utica shale where EQT Midstream operates.

Increased gas supply is needed to meet the growing demand for both the U.S. switching from coal to gas-fired power plans, as well as gas exports to fast-growing emerging markets such as Mexico, China, and India.

Source: U.S. Energy Information Administration

As gas production grows, the Interstate Natural Gas Association of America forecasts that by 2035 the U.S. will need nearly $800 billion worth of new midstream projects constructed to support the energy boom.

Around $400 billion of that spending is expected to be focused on natural gas projects, which EQT Midstream is presumably well situated to exploit.

If EQT Midstream's tollbooth-like business model is so stable and its long-term growth potential so great, then why has its stock suffered so much in recent years?

Unfortunately, the firm's has a very complex profile, which has soured many investors on the traditional MLP business model in general, and EQT Midstream in particular. Key Risks While EQT Midstream's underlying cash flow is highly stable due to the long-term and volume-committed nature of its contracts with EQT Corp, there are still real risks to consider with this MLP.

After all, EQM's unit price has plunged about 35% in 2018 and are down roughly 50% from its all-time high (before the oil crash began in mid-2014).

The first reason for the stock's weakness has been the complex nature of the corporate restructuring. The market hates uncertainty and complexity, and due to the MLP bear market EQT Midstream's use of stock to buy Rice Midstream was dilutive to existing investors.

As a result, its distribution coverage ratio (DCF/distributions) fell from its previous long-term average of 1.3 to 1.11 today. While that's technically still a sustainable coverage ratio, there's much less margin for error.

In addition, EQT Midstream's low unit price and continued existence of IDRs have made it less appealing to investors, especially compared to numerous rivals who have simplified their structures and eliminated costly IDRs in recent years via GP and MLP mergers, IDR buyouts, or corporate conversions. IDRs increase an MLP's cost of capital because so much of marginal cash flow from new projects ends up going to their general partners.

With its unit price so low, EQT Midstream is unable to fund its growth projects with accretive equity, which is a key component of the traditional MLP business model.

Due to the firm's inability to access equity markets (possibly ever again), on its most recent conference call the firm's new CEO Tom Karam told analysts the MLP's goal is to "deliver consistent distribution growth, strengthen our coverage ratio, and live within our means without issuing equity."

While reducing the firm's dependence on fickle stock market sentiment to profitably fund its growth projects is welcome news, this brings up two important points that investors need to know.

First, as part of the restructuring, EQT Midstream's management changed, with new executives coming in. Under the new team's goals, slower distribution growth is likely because EQT Midstream can only increase its distribution coverage ratio (and thus retain more cash flow to fund growth) if it increases its distribution slower than the rate at which its cash flow grows.

Currently, management's three-year guidance is for 14.5% annual DCF growth which means that earlier guidance for 15% to 20% distribution growth is now unsustainable.

One reason is because EQT Corp, the MLP's biggest customer by far, has lowered its long-term gas production growth plans from about double-digit annual growth to "mid-single digit" growth.

While management hasn't provided exact long-term payout growth guidance for EQT Midstream, Equitrans' 8% to 10% dividend growth rate likely provides a good estimate for what kind of growth EQT Midstream investors can expect (since Equitrans gets all its cash flow from EQT Midstream and its GP).

In theory, that would allow the MLP's distribution to keep rising steadily, while also boosting the coverage ratio to much safer levels that lower its reliance on external equity markets for funding its growth.

However, investors should know that, eventually, the MLP will likely have to simplify its structure as many of its peers have done. At the very least, that means EQT Midstream will need to eliminate its IDRs through a stock-funded buyout. Management likely wants the MLP to increase its distribution coverage so it can afford to do a deal like that without jeopardizing the payout.

Another potential simplification approach EQT might take to improve its valuation and trading liquidity is for EQT GP Holdings or Equitrans to buyout EQT Midstream alone, or in conjunction with EQT GP holdings as well.

The resulting corporate conversion could be a taxable event, as well as possibly result in an effective distribution cut for EQT Midstream investors. Basically, Equitrans might buy EQT Midstream, and its GP investors would receive Equitrans shares at some fixed exchange ratio. While management has not indicated that this is likely to happen soon, the low unit price is likely factoring in this risk.

However, even if no corporate conversion comes there is one final risk EQT Midstream investors need to be aware of.

The largest growth project the MLP is working on is the Mountain Valley Pipeline, or MVP. This project was originally expected to be fully in service by the end of 2018 but numerous delays, created by lawsuits challenging its regulatory approvals, have caused management to push that date back to the fourth quarter of 2019. Worse, the project's cost is now 25% higher than previously expected.

While management continues to remain confident that the MVP will eventually be completed, it's always possible the pipeline might take even longer, and cost more, to put into service.

In that scenario, the MLP's cash flow projections could come in under target and force it to slow its distribution growth even further. And in a worst case scenario, the project may end up canceled which would represent a major blow to the MLP's already weakening distribution growth thesis.

The good news is that EQT Midstream's coverage ratio is already high enough to make a distribution cut under this scenario unlikely. However, should the MVP end up scrapped, then the MLP's unit price could take a further beating and its yield remain very high for the foreseeable future.

Such an outcome would only increase the risks of management having to do a corporate conversion or simplification that could result in an effective distribution cut via a merger with EQT GP Holdings or Equitrans Midstream.

Closing Thoughts on EQT Midstream Partners EQT Midstream owns a highly valuable collection of midstream assets that have, up until now, delivered safe and fast-growing payouts to investors. However, the MLP bear market, triggered by the oil crash and then later made worse by rising interest rates and regulatory changes at FERC, has created immense challenges for the traditional MLP business model.

EQT Midstream has managed to adapt well enough thus far to avoid the distribution cuts that so many of its peers have been forced to pursue. The firm's strong balance sheet, reasonable payout ratio, and slower but still steady demand growth from its largest customer EQT Corp have certainly helped.

However, 2018 has been a very challenging year for the MLP, with numerous costly delays with its largest growth project, and a corporate restructuring that Wall Street has punished with a sharp unit price decline.

While EQT Midstream's high yield appears secure today, the longer it struggles with getting the MVP online, the more risk it faces that a perpetually low unit price might force management to once more restructure EQT's midstream operations.

Such an action could come in the form of a merger with EQT GP Holdings or Equitrans that, depending on the terms, could result in an effective distribution cut, not to mention uncertain tax consequences.

Thus, while EQT Midstream could remain a dependable income source for now, investors need to be well aware of these risks and complexities before considering the stock. Conservative investors should probably avoid the stock in favor of safer, simpler alternatives, including self-funding MLPs who have already eliminated their IDRs and face fewer uncertainties (like Magellan Midstream Partners and Enterprise Products Partners).