A Review of Kraft Heinz's Dividend Safety and Struggling Turnaround

Whenever a dividend stock's price plunges to multi-year lows, investors naturally want to know if the market is signaling that something is deeply wrong, such as if the business model has weakened enough to potentially put the dividend at risk.

That's been the case with food giant Kraft Heinz (KHC), which has fallen over 40% from its early 2017 peak while the S&P 500 has climbed more than 15% during that time.

Let's take a closer look at Kraft Heinz's struggles to evaluate the safety of its dividend and whether it is appealing as a long-term investment.

Why Kraft Heinz is Struggling

The key reason why the market dislikes Kraft Heinz right now is that, like many food companies, the firm has been struggling to adapt to changing consumer tastes. Specifically, packaged and highly processed foods are falling out of fashion as consumers increasingly opt for healthier foods, organic products, and less processed selections.

With product lines such as Oscar Mayer hot dogs, Kraft Mac & Cheese, Cool Whip pie topping, Kool-Aid drink mixes, and Lunchables snacks, much of Kraft Heinz's portfolio finds itself in the crosshairs of the healthier eating trend.

In fact, for the last 10 years, outside of mergers and acquisitions, Kraft's sales have been essentially flat. Up until last quarter, company-wide organic sales had also declined for six consecutive quarters.

Besides healthier eating, Kraft Heinz's management, which was put in place by Brazilian private equity firm 3G Capital, has added to the firm's challenges. 3G, like most private equity shops, is known for its ability to "improve" a company's performance by cutting costs and squeezing out efficiencies.

3G CEO Jorge Paulo Lemann, who helped put together the merger between Kraft and Heinz and assembled the current management team, has said that he's been surprised that consumer packaged goods continues "being disrupted."

The trouble is that 3G's approach to cost cutting has come at the expense of spending sufficient amount of money on advertising to support Kraft Heinz's core brands. While most food companies spend 5% to 10% of revenue annually on marketing and new product development, for example, under 3G Kraft Heinz has invested just 2% to 3% of its sales on these crucial areas since 2015.

As a result, organic growth (excludes acquisitions) has actually fallen by 1% per year over the past three years. Management has said it will increase marketing in the future, but so far that hasn't happened.

Perhaps more concerning is that during this time Kraft has actually made great strides to shift its product mix towards today's healthier and more natural foods. For example, it eliminated artificial preservatives, coloring, and flavoring from its famous macaroni and cheese and launched new, healthier frozen food brands such as Devour (frozen snacks) and SmartMade (frozen meals).

Meanwhile, the company's lean advertising budget has shifted more towards digital where management assured investors the company would be able to leverage data analysis into stronger brand awareness and, ultimately, better top and bottom line results.

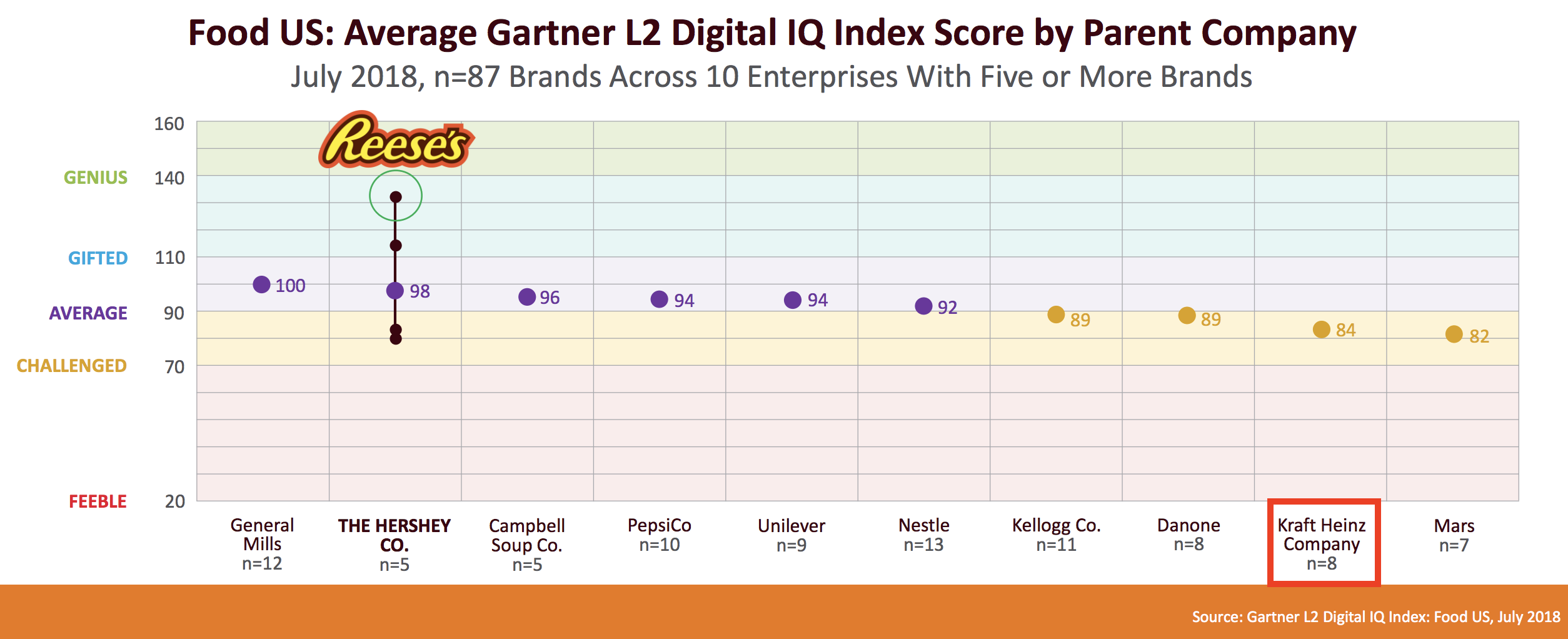

However, the latest Gartner digital brand awareness survey (July 2018) shows that Kraft Heinz's online brand awareness trails that of its peers. In fact, it's ahead of only struggling candy maker Mars.

Source: Hershey Investor Presentation

Most alarming of all is that the company's strong brands, the cornerstone of its success over the past 149 years, appear to be losing their pricing power with consumers.

In the most recent quarter, for example, the company reported 2.6% organic sales growth. However, that gain was composed of 3.5% volume growth offset by a -0.9% decrease in prices. In the U.S. (about 70% of company-wide revenue), organic sales were up just 1.8%, consisting of strong 3.8% volume growth but offset by a 2% decrease in pricing.

For decades, Kraft investors could count on the company's strong brands to command rising prices over time, usually far above the cost of any inflation (from rising commodity prices for example).

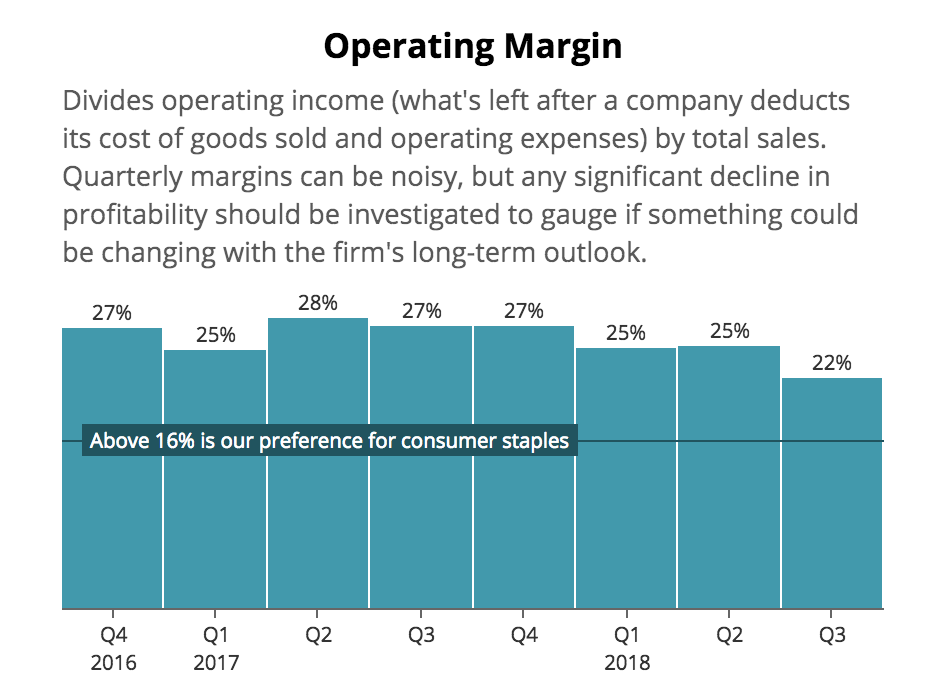

However, today Kraft is only seeing slightly positive sales growth due to cutting its prices. As a result, higher commodity and shipping costs are eroding its operating margin, which fell to 22% in the third quarter from 27% a year earlier; adjusted EBITDA declined 14% year over year as a result.

Source: Simply Safe Dividends

So while a return to organic sales growth appeared to be good news at first glance, the devil was in the details. Returning to positive top line growth at the expense of bottom line profits is hardly inspiring, and investors have become even less convinced that Kraft Heinz can get both pieces to move higher together.

CFO David Knopf told analysts on the conference call that the company expects "a much better balance of top and bottom line growth going forward," because the quarter's margin compression was due to temporary challenges.

From stepped up commercial investments to additional cost inflation, one-off supply chain costs, and a decision to prioritize customer service with additional hiring, management had a laundry list of "temporary" cost challenges that are expected to fade in the quarters ahead. Management also indicated they would consider raising prices next year.

Here's what Mr. Knopf said on the company's third-quarter earnings call:

"All that to say, we're not going to provide precise numbers around it but we expect both EBITDA growth and our absolute level of profitability to improve significantly beginning in Q4 and into next year versus what we saw this year and in the first half."

However, investors remain worried that Kraft Heinz's best days (and pricing power) could be behind the company as its brand-based competitive advantages are slowly eroded by trends such as healthier eating and online grocery shopping.

Should profitable growth remain elusive, there are several implications for Kraft Heinz's dividend safety and long-term growth prospects.

Kraft Heinz's Dividend Profile is Somewhat Delicate

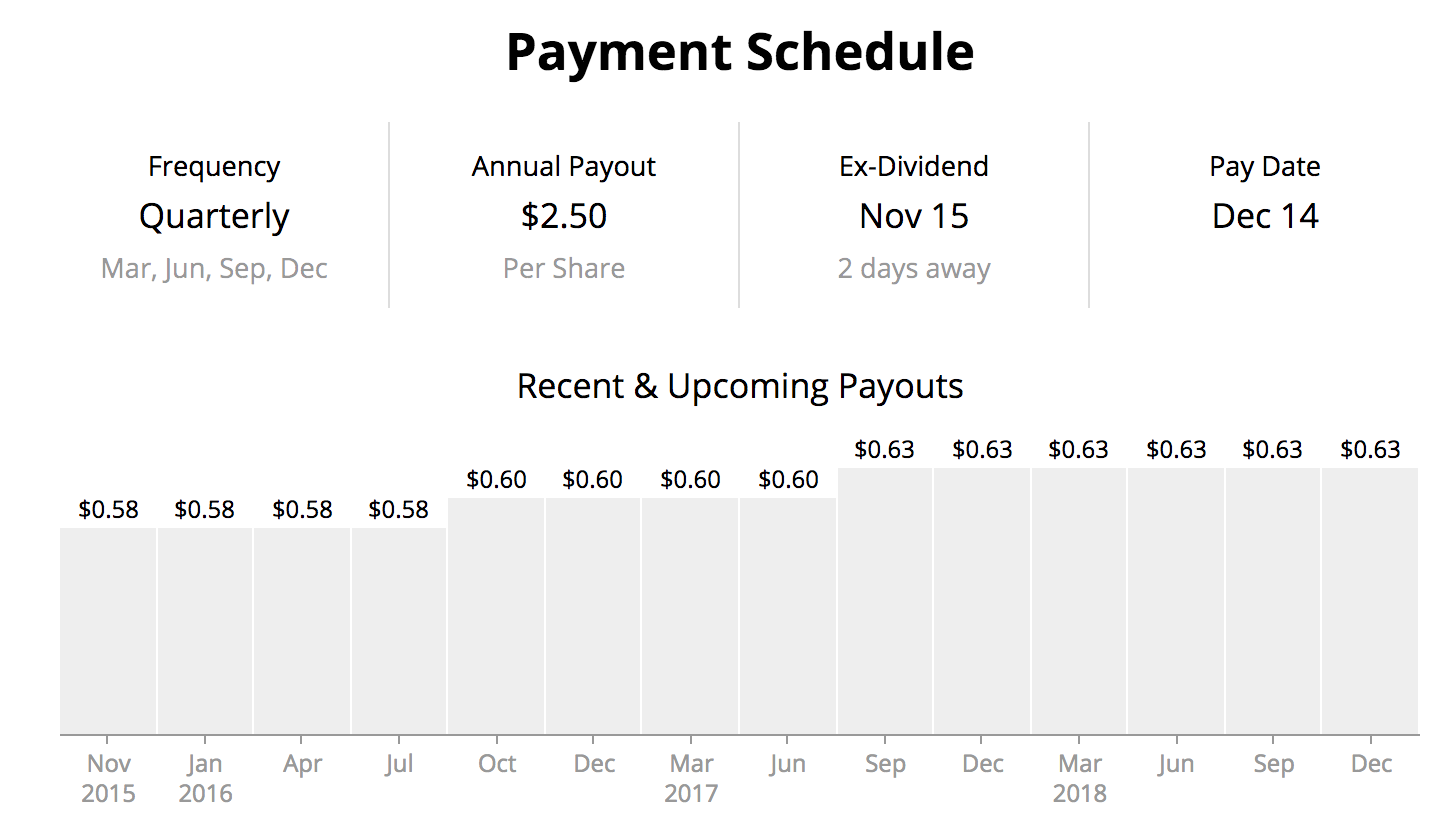

A dividend increase signals management's confidence in the business. However, Kraft Heinz's payout has remained frozen for six consecutive quarters, and the company's Dividend Safety Score of 41 sits at the bottom rung of our "Borderline Safe" category:

Source: Simply Safe Dividends

These can be murkier situations to evaluate, and Kraft Heinz is no exception given some of the growth challenges it is dealing with today.

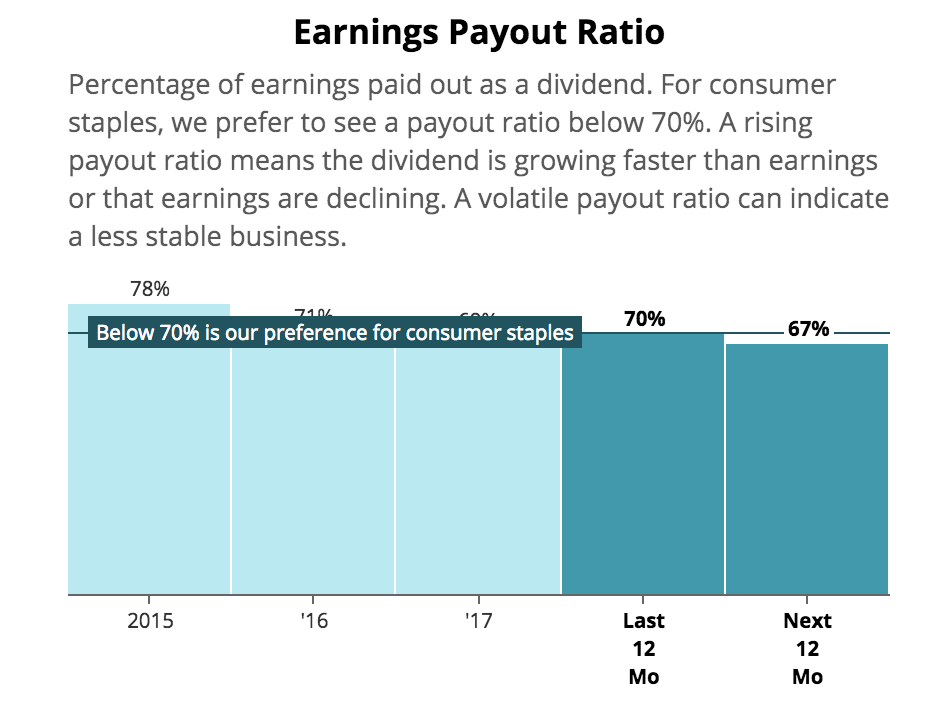

For starters, the company's earnings payout ratio sits near 70%, which is at the high end of what we prefer to see for most consumer staples businesses.

Source: Simply Safe Dividends

While that normally wouldn't be much of a concern given the stability of these businesses, a relatively high payout ratio doesn't leave Kraft Heinz much retained profit it can use to invest in growth initiatives and improve its balance sheet.

Looking at free cash flow, which represents the actual cash a company has generated after investing to maintain and grow its business, the picture hasn't been pretty this year.

Through the first three quarters of 2018, Kraft Heinz generated $2.2 billion of adjusted cash flow from operating activities and invested approximately $600 million in capital expenditures, leaving free cash flow of $1.6 billion.

However, during that same period the company doled out $2.4 billion in dividends, resulting in an $800 million funding gap.

In fairness, Kraft Heinz's year-to-date free cash flow has been temporarily suppressed by a handful of cost challenges (higher commercial investments, supply chain issues, commodity cost inflation, significant customer service hiring) that are expected to drop off.

The question is whether management's expected improvement in cash flow will be significant enough to begin covering the dividend again while providing a comfortable amount of retained cash flow. Unfortunately, Kraft Heinz wouldn't give more specific guidance about just how much EBITDA growth management expects in 2019.

Cash flow growth is becoming a bigger deal as Kraft Heinz appears to be falling further behind with its food portfolio and maintains a lot of debt on its balance sheet, reducing some of its financial flexibility.

In recent quarters, due to the free cash flow deficit previously discussed, the firm has been paying its dividend out of cash reserves. Over the past two years, the company's cash on hand has dwindled from $3.9 billion to just $1.4 billion.

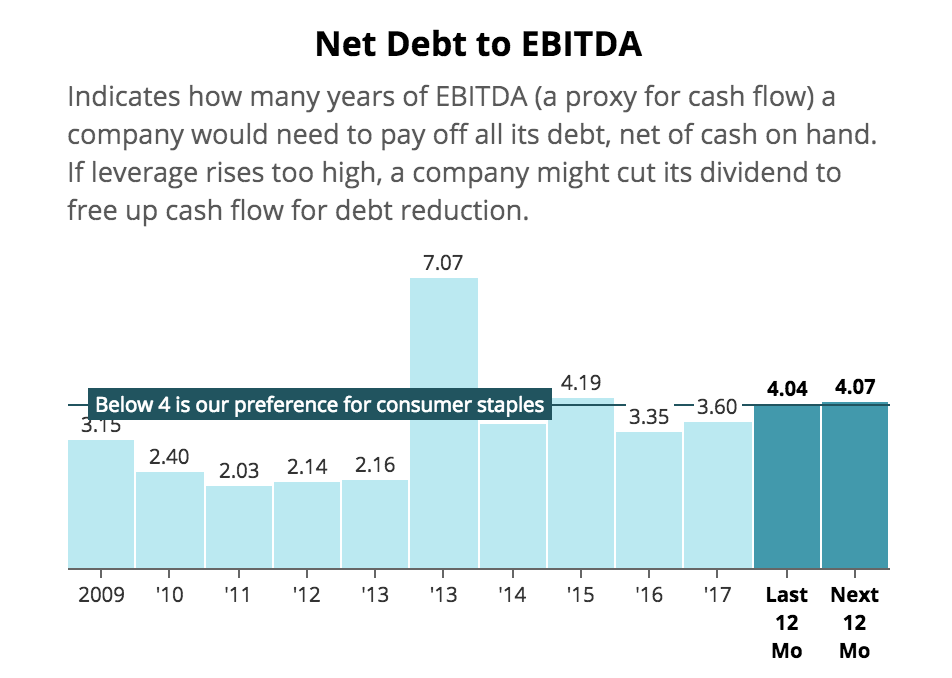

Worse, Kraft Heinz's net debt / EBTIDA (leverage) ratio sits at 4.04, well above the industry average of around 2.6, and is not expected to improve over the next year thanks to the margin pressure and cost challenges the company is facing.

Source: Simply Safe Dividends

The Kraft-Heinz merger increased the company's debt burden (over $32 billion on the books today), and this year the firm's poor cash flow generation and high dividend payout has not put the business in a position to meaningfully reduce its leverage. In fact, total net debt has increased by over $1 billion thus far in 2018.

Kraft Heinz's debt-laden balance sheet could also eventually threaten its Baa3 credit rating (one notch above junk bond status). For example, while Moody's reaffirmed Kraft Heinz's Baa3 equivalent rating in May 2018, it did note that:

Moody's believes that a portion of the incremental free cash flow generated is likely to be reinvested in internal and external growth initiatives, including possible major acquisitions. As a result, Moody's assumes that further reduction in financial leverage will likely come from earnings growth rather than debt repayment...

The ratings could be downgraded if operating performance deteriorates, or the company pursues major debt-financed acquisitions or shareholder-friendly initiatives.

While companies are loath to cut their dividends, if they believe their credit rating is threatened or they need significantly more capital to improve their long-term prospects, they are far more likely to do so.

Moody's current stable rating on the company's debt is predicated on future earnings growth and no major acquisitions (Kraft Heinz tried to buy Unilever in 2017 for $143 billion) that would add to its already large debt levels.

As a result, the firm's disappointing earnings growth and high debt levels mean that Kraft Heinz is likely limited in its ability to buy back shares or increase its dividend, which helps explain the current dividend freeze.

The good news is that Kraft Heinz still has solid liquidity. In addition to the $1.4 billion of cash it holds, the firm has an untapped credit revolver with $4 billion of capacity that doesn't expire until July 2023. Furthermore, average annual debt maturities through 2022 sit at a manageable $3 billion.

In other words, there does not appear to be a pressing need to conserve cash.

The big question is how committed management will remain to the payout if cash flow growth continues to disappoint and urgency to improve the firm's portfolio of food brands increases (either organically or via a large acquisition).

After all, this team seems willing to make big capital allocation moves if their previous offer to buy Unilever for more than $140 billion is any indication, and it's hard to say how wedded 3G Capital is to the dividend.

With Kraft Heinz's dividend consuming over $3 billion of cash each year, that's a lot of money that could go towards deleveraging, higher marketing and R&D investments, and more acquisitions.

For now, the dividend seems more likely than not to remain safe, but management has little margin for error. Cutting discretionary costs further, achieving stronger growth overseas, and developing healthier products in the U.S. are all important initiatives that need to go well.

And the "temporary" costs that have weighed on recent results need to prove to be temporary, starting when the company reports fourth quarter results in February.

In the meantime, shareholders should expect little to no dividend growth as the company attempts to get closer to management's long-term leverage target of 3.0 and return to profitable growth.

Closing Thoughts on Kraft Heinz

Kraft Heinz still owns some popular brands and enjoys industry-leading profitability thanks to 3G Capital orchestrating aggressive post-merger cost cutting. However, those cost savings have apparently come at the expense of the company's product development and marketing efforts, which has left Kraft Heinz struggling worse than most major packaged food and consumer staples companies.

While management is saying all the right things about shifting the company's product mix to healthier options and using digital advertising to maximize returns on investment, thus far Kraft Heinz's turnaround has been all promise, with little benefit to the top or bottom line.

And given the company's somewhat high payout ratio and large amount of debt, if Kraft Heinz can't start delivering on its turnaround plan quickly (in 2019), then the risk of its frozen dividend being cut could increase.

While the stock's current yield is certainly generous, conservative income investors may prefer to look at other companies with safer dividends, superior growth potential, and less hair from a heavy debt load and struggling turnaround effort.