Royalty Trusts: Why Most Dividend Investors Should Avoid Them

After nearly a decade of historically low interest rates, many yield-starved income investors have flocked to high dividend stocks.

But there are many different classes of high-yield stocks, some much safer and more appropriate for conservative investors than others.

Let's take a look at one popular high-yield investment class, royalty trusts, to see what investors need to know before investing in them.

Most importantly, learn why their business models and limitations likely make them inappropriate for meeting your income needs, especially in retirement.

What are Royalty Trusts?

The first royalty trust was incorporated in 1956, although the popularity of royalty trusts did not really take off until the 1980s. Around two dozen royalty trusts are listed on U.S. exchanges today, and the reason many income investors are attracted to trusts is their eye-popping yields, which frequently exceed 10%.

At their core, royalty trusts usually own a non-operational interest in oil and gas minerals. Generally, royalty trusts are used as a form of financing in the energy sector, where an energy producer can sell royalty rights from oil and gas well extraction on some of its assets.

The trust then uses that stream of royalty cash flow, which is commonly tied to production volumes, to pay distributions to unit holders (what royalty trust shareholders are called).

Royalty trusts are a type of pass-through entity that is structured similarly to real estate investment trusts (REITs) and master limited partnerships (MLPs). As long as they distribute a certain level of profits to unit holders as distributions, they avoid paying federal income tax.

Their distributions are usually classified as a return of capital, meaning the payouts are a non-taxable event. Instead, the distributions reduce a unit holder's cost basis and thus defer taxes until he sells his position in the trust.

Let's use one of the largest and most popular trusts, BP Prudhoe Bay Royalty Trust (BPT), to review how these entities are structured, the nature of their operations, and the risks that make them inappropriate for most conservative income investors.

The Business Model of Royalty Trusts

A royalty trust isn't actually a company with employees, active management, or any operational activities in energy production. As a result, their financial statements are quite simple. Here's a look at BP Prudhoe Bay's equivalent to an income statement, for example.

Source: BP Prudhose Bay Royalty Trust 10-K

Rather than own hard assets and engage in productive activities, royalty trusts serve as a financing vehicle by owning the income rights to a fixed amount of oil or gas sold by an upstream energy company.

For example, in 1989 the BP Prudhoe Bay Royalty Trust was established by energy giant BP (BP) in order to raise money to drill in Alaska's Prudhoe Bay (North Slope of Alaska). The actual trust is administered not by BP but by the Bank of New York Mellon (BK) who handles the payouts to investors.

The trust's unit holders have the right to a royalty on 16.4246% of the first 90,000 barrels of BP's average daily net production of oil and condensate out of the acreage owned by the trust. The royalties are paid by BP on a quarterly basis.

Like MLPs, royalty trusts pay out the vast majority of their cash flow to investors. However, unlike MLPs, which try to grow their income producing assets over time, trusts start out with a fixed asset base that typically doesn't grow.

In this case, BP Prudhoe Bay's assets are purely the cash flow being generated from BP's Prudhoe Bay unit, up to the first 90,000 barrels per day. Over time, the depletion of the oil and condensates under that acreage will naturally result in falling royalty income.

As a result, the trust is structured to terminate (i.e. liquidate) when either 60% of unit holders vote to do so, or royalty income declines below $1 million per year for two consecutive years.

At that time, BP has the right to repurchase the trust's units from investors at the greater of the trust's current market price or the fair market value of the trust property as determined by an investment banking firm.

If BP chooses not exercise its option to buy back the trust's units, then Bank of New York Mellon, the trustee, will have the ability to liquidate what assets the trust still has, and then distribute the proceeds to unit holders.

The expected date of the trust's termination also fluctuates wildly, depending on oil prices. In 2014 when oil was over $100 per barrel, the end date for the trust was estimated at no longer than 2029.

However, during the peak of the oil crash in 2016, the firm warned investors that royalty payments to the trust might cease as early as 2019.

At the end of 2017, BP Prudhoe Bay estimated that royalty payments would continue through 2019 but drop to zero in the following year. Here's what the trust stated in its 2017 annual report:

"Based on the 2017 twelve-month average WTI Price of $51.34 per barrel, current Production Taxes, and the Chargeable Costs adjusted as prescribed by the Overriding Royalty Conveyance, it is estimated that royalty payments to the Trust will continue through the year 2019, and would be zero in the following year. Therefore, no proved reserves are currently attributed to the BP Prudhoe Bay Royalty Trust after that date.

Even if expected reservoir performance does not change, the estimated reserves, economic life and future net revenues attributable to the Trust may change significantly in the future as a result of sustained periods of change in the WTI Price, the Production Tax or from changes in other prescribed variables utilized in calculations as defined by the Overriding Royalty Conveyance. Such changes could result in the termination of royalty payments prior to 2019."

In other words, unlike most dividend stocks which are perpetual organizations who attempt to grow their cash flow and payouts over time, this trust will have a definite end date. Simply put, BP Prudhoe Bay Royalty Trust (and all trusts) are not "buy and hold forever" investments.

But what about owning a trust for just a few years, collecting those big distributions well before a trust reaches the end of its life? For most investors, that's still a poor idea.

The Biggest Downsides of Royalty Trusts

Unlike REITs or MLPs, which sustain and grow their payouts from stable cash flow that's supported by long-term leases and fixed-fee contracts, the cash flow generated by royalty trusts is extremely volatile and totally at the mercy of wild swings in oil and gas prices.

In other words, the dividend payments backing a royalty trust's high yield are very volatile from one quarter to the next. As a result of these variable payments, which are based on the daily production rate and the price of oil, an investor has no way of knowing exactly how much income he will receive from a royalty trust over the course of a year.

For example, in just the last three years BP Prudhoe Bay Royalty Trust's quarterly distribution has ranged from 7.2 cents per unit (in the first quarter of 2016 when the price of oil fell to $26 per barrel) to $1.47 (in the second quarter of 2015 when oil peaked at $107 per barrel).

Source: Simply Safe Dividends

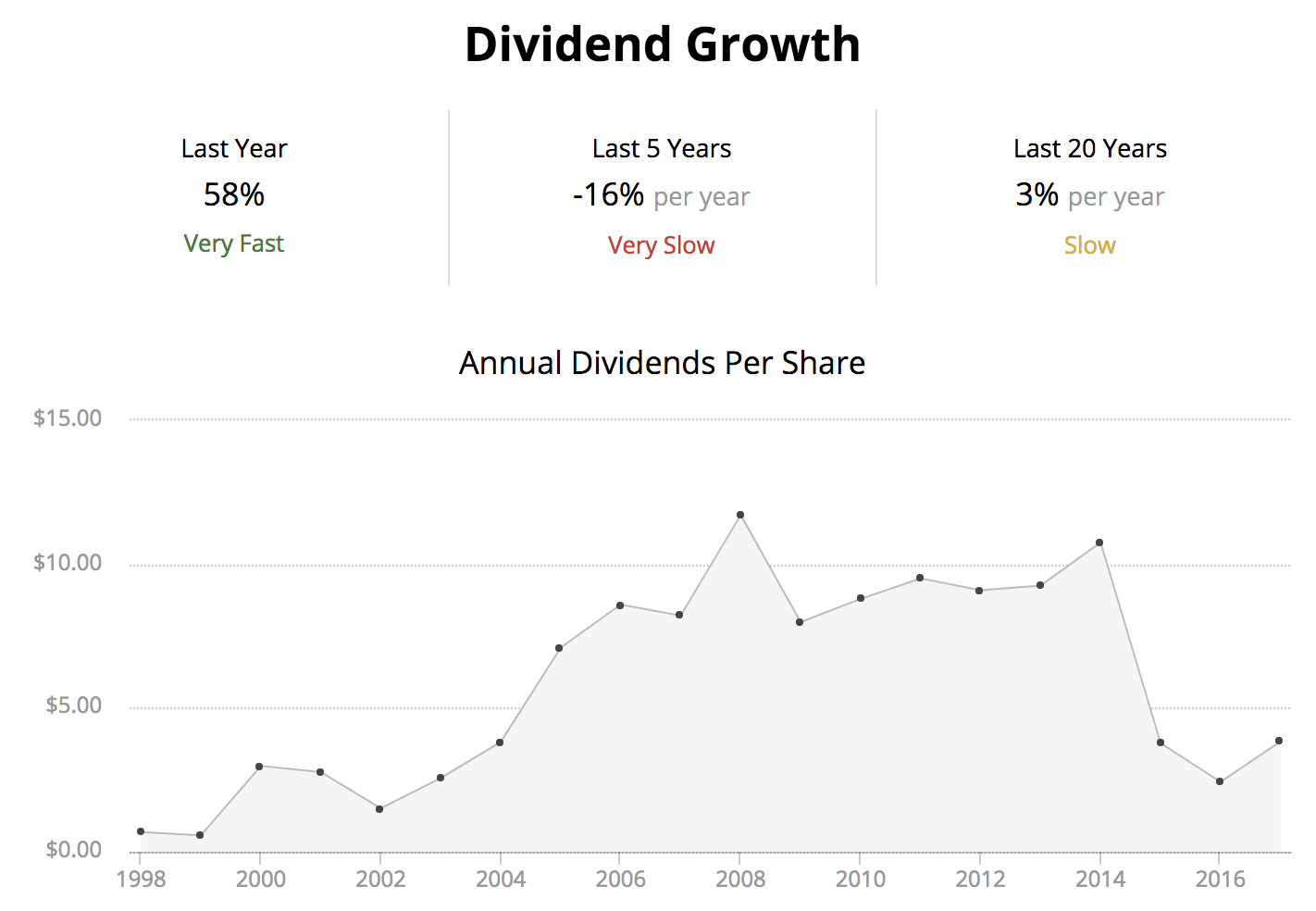

However, trust distributions are not just a function of unreliable and unpredictable oil prices. They are also very dependent on the founding energy company's production decisions, which have been a major contributor to the massive decline in BP Prudhoe Bay's distribution since it peaked in 2008.

Source: Simply Safe Dividends

The decline in the trust's distribution has not only been caused by oil prices getting cut roughly in half since 2008 (peak of about $140 per barrel), but also because production has been falling under that 90,000 barrels per day (bpd) royalty cap.

BP has been investing less in drilling new wells on the trust's acreage since the oil crash. As a result, in the second quarter of 2018 daily average production for BP's trust fell to 84,000 bpd, down from 91,800 bpd a year earlier.

Since oil peaked in 2015, the trust's production has been consistently below its 90,000 bpd royalty cap and, according to the trustee, production is expected to be below 90,000 bpd "in most future years."

Simply put, acreage oil reserves are being steadily depleted, no new reserves are being added, and BP is not expecting to invest in drilling new wells to raise production, even with oil prices up significantly since early 2016. During the oil crash BP cut the number of rigs operating on the trust's acreage from four to two, and that figure has not been increased since.

Therefore, the trust's income will be purely dependent on the price of oil, multiplied by steadily falling oil production. As a result, investors have no idea how much of their initial investment they can recoup before the trust is ultimately liquidated.

Remember that those distributions are not taxable income but rather a return of your initial capital. On each ex-dividend date the unit price is reduced by the distribution amount, thus lowering the value of your investment.

If you buy BP Prudhoe Bay Royalty Trust at $25 per unit, for example, then you need to receive at least $25 in distributions just to break even. That's because on the trust's termination date you are likely to receive next to nothing, since the unit price is set by the market and purely based on expected future distributions. Since future royalty income and thus distributions are eventually guaranteed to go to zero, the unit price will likely fall to zero over time.

Due to declining production, BP Prudhoe Bay's distribution would need oil prices to move steadily higher, just to remain relatively steady at current levels. Given the volatile nature of oil prices, that is a very uncertain scenario for income investors to bet on.

But let's say you get lucky, and the trust's payout benefits from a historic, sustained surge in the price of oil to $100 per barrel or beyond. Even then, BP Prudhoe Bay Royalty Trust is likely to make a poor investment. Here's why.

Let's assume that the higher oil price pushes the trust's termination date back out to 2028, which was the expectation back in 2014. Let's also assume that BP Prudhoe Bay Royalty Trust is able to maintain $5 per year in distributions, with steadily rising oil prices offsetting falling production over time.

In that scenario, for the remaining 10 years of the trust's life (remember it might be far sooner), investors who buy today at $25 per unit would receive $50 in distributions over the next decade.

Since the trust's value falls to effectively zero at termination, your actual gain over this 10-year period is $25 ($50 in payouts minus $25 invested capital). You will pay long-term capital gains taxes on this figure at the time (deferred tax liability).

So even in a best case scenario, investors in this trust would earn a 43% total return. That equates to a 3.6% annual total return, not adjusted for inflation. For context here's how safer alternatives to royalty trusts have performed historically:

bonds: 4.9% (since 1900)

stocks: 9.6% (since 1900)

REITs: 11.7% (since 1972)

Dividend Aristocrats (S&P 500 companies with 25+ consecutive years of dividend increases): 12.1% (since 1990)

This shows that royalty trusts are actually a "yield trap" that makes for a far worse long-term income investment than much safer alternatives.

And that's the best case scenario. According to the trust's latest annual report if oil prices average $51 over time "estimated royalty payments to the Trust will continue through the year 2019...and would be zero in the following year." This would mean the trust might potentially be terminated as early as 2021 since royalty payments of zero in 2020 trigger liquidation. While oil price fundamentals (medium-term supply/demand outlook) means oil prices are not likely to return to $50 anytime soon, they are highly unlikely to rise steadily over time (unprecedented in industry history).

This ultimately means that BP Prudhoe Royalty Trust investors are likely facing much lower than $35 in future payouts, which would put you are at high risk of booking a net loss if you invest today. But wait it gets worse. Not just does this trust specifically (and all trusts in general) suffer from declining distributions and poor long-term total return potential, but there's also tax complexity to consider.

For example, due to complex depletion tax allowances, investors owning trusts will not just have to file the standard 1040 tax form, but also supplement that with the schedule E and B tax form. What's more trust investors are liable for paying state income taxes as well. In the case of BP trust Alaska doesn't have a state income tax so this isn't a concern. But other trusts operate in different states where you will have to pay income taxes, further complicating your annual tax preparation and lowering your total returns even more.

Closing Thoughts on Royalty Trusts

High-yield stocks can be a great way for investors to grow their wealth over time, or merely support themselves during retirement. But while blue chip REITs and MLPs are potentially great long-term income growth investments, royalty trusts are not.

That's because they are not growing organizations with stable cash flows that support safe and growing dividends/distributions. Rather they are collections of depleting and commodity sensitive assets with a guaranteed termination date that means their mouth watering yields are an illusion. In reality all royalty trust distributions are returns of your original investment, which means that anyone investing in them is taking on substantial risk. Not just in terms of volatile swings in distributions, but in potentially generating negative total returns over time.

On top of that royalty trusts come with tax complexities that make them just not worth owning. Not when there are far superior and lower risk alternatives for generating generous, safe, and steadily growing income to help you achieve your long-term financial goals.