It's been a brutal year for dividend aristocrat AbbVie (ABBV), which has seen its share price plunge more than 30% from its all-time high. As a result, the stock's yield is now at a record high of 5.2%, and shares trade at just 9.9 times forward earnings.

Whenever a dividend stock's price crashes this severely, income investors naturally want to know whether it could be a great buying opportunity or is the market's way of warning that the payout may no longer be safe. At the very least, such severe price declines can signal that a company's long-term thesis is broken.

Let's take a look at why the market has been so bearish on AbbVie and whether this high-yield stock could be a reasonable dividend growth investment or a value trap to avoid.

The Drivers Behind AbbVie's Weak Performance

Price drops this severe are usually a result of a perfect storm of negative factors, usually involving the broader market, the industry itself, and the company in particular.

October's stock market pullback sent most stocks lower. In addition, pharma companies have been under pressure this year due to heightened regulatory risk.

Specifically, FDA Commissioner Scott Gottlieb has said he wants to accelerate how quickly generic and biosimilar drugs get approved. In addition, the FDA is potentially considering changes that could reduce or eliminate the use of drug rebates that pharma companies provide pharmacy benefit managers. Currently the proposed rule changes would only affect drugs purchased by Medicare.

Further fueling the market's fears about the pharma industry's margins is news that President Trump is now considering benchmarking Medicare reimbursement rates to the average drug price in Europe (usually 50% lower than in the U.S.).

At the company-specific level, AbbVie has faced pressure as well. The first major blow came in late March 2018, when disappointing drug trial results came out for the firm's promising Rova-T cancer drug.

That trial was actually for a third line indication (to be used if patients failed with two previous drugs first). However, it means the risks of future poor drug trial results on more important approvals (expected in 2019) have increased.

Rova-T was a potential $5 billion per year blockbuster drug (compared to company-wide revenue of about $32 billion today) and the key reason AbbVie paid about $10 billion to acquire biotech company Stemcentrx in 2016. The poor result caused analysts to reduce the expected future peak sales for Rova-T, in some cases from $5 billion per year to $2 billion.

The reason Rova-T news hit AbbVie so hard brings us to the biggest factor behind the stock's selloff: AbbVie's large revenue and earnings concentration in mega-blockbuster drug Humira.

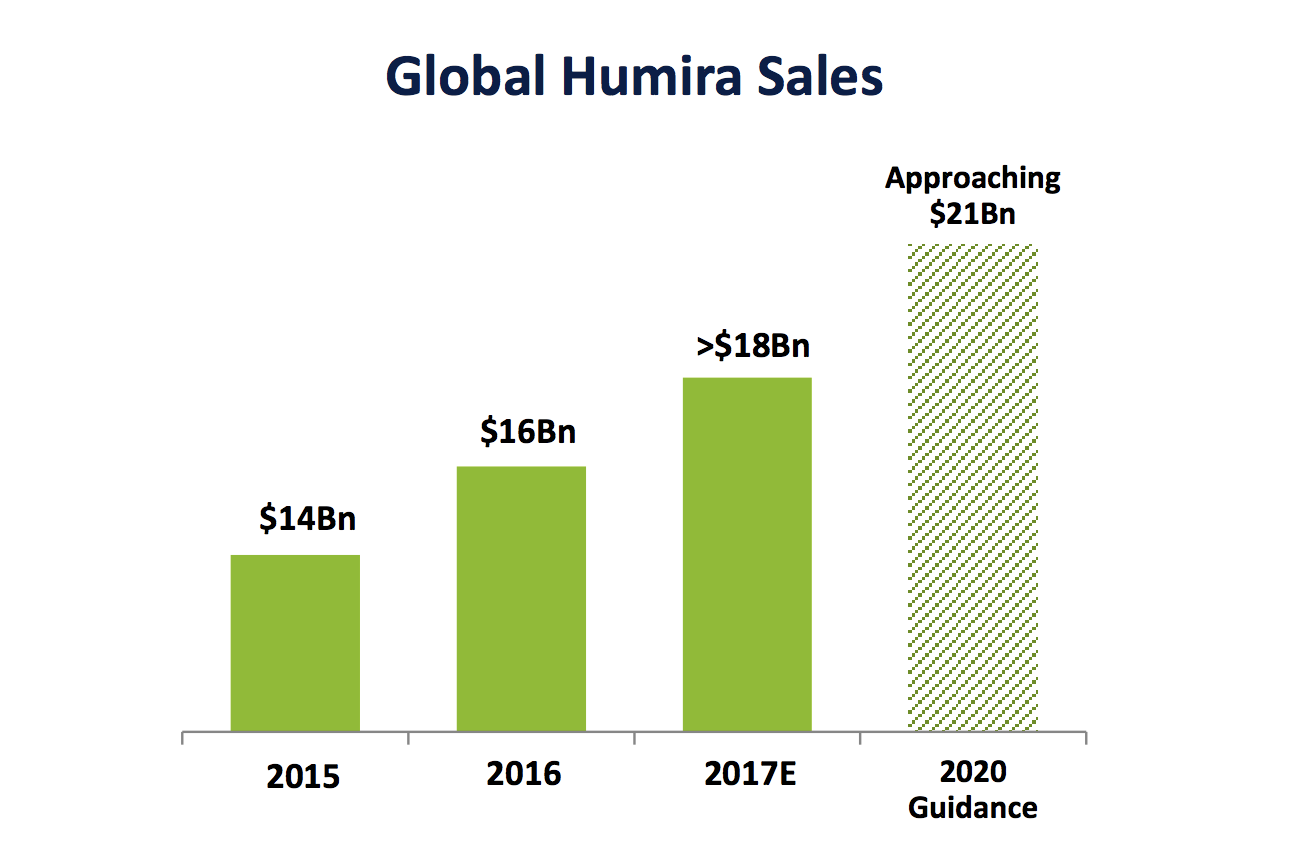

Humira is an IV immunology drug (treats issues like arthritis) and has become the best-selling drug in history. In 2017 Humira generated $18 billion in sales. The drug is on track for sales of $20 billion in 2018, and management expects revenue to peak at about $21 billion in 2020.

Source: AbbVie Investor Presentation

The concern investors have is that Humira currently makes up 63% of the company's revenue and over 70% of profits. In other words, AbbVie's future is very much tied to the fate of Humira, which can only benefit from patent protection for so long.

In 2018 Humira lost patent protection in the EU, and numerous rivals are launching biosimilars there starting in October 2018. Management had previously said it expected EU Humira sales to decline by about 20% in 2019 as a result of having to cut prices on the drug to maintain market share.

But on October 31, Bernstein analyst Ronny Gal reported that AbbVie was planning to cut Humira costs in the EU (and had already won the first national healthcare contracts) by 80%. That was far larger than the 50% price cut that most drugmakers offer when biosimilars hit the market.

As a result, Mr. Gal thought that the company would have to revise its EU Humira (and overall company sales) guidance downward. Fortunately, when AbbVie reported third-quarter earnings on November 2, the outcome wasn't so bad.

While discounting is coming in higher than expected, its impact doesn't appear to be as severe as bears feared. However, the dust has yet to completely settle for this next year. Here were management's relevant comments:

"HUMIRA global sales were $5.1 billion in the quarter, up nearly 10% operationally. In the U.S., HUMIRA sales increased 12.5% compared to the prior year, with more than half driven by underlying volume growth plus a mid-single digit price contribution...International HUMIRA sales approached $1.6 billion in the quarter, up 4.2% on an operational basis and in line with our prior guidance...

Now to characterize for you what are we seeing versus what we planned for, I'd say on average the discounting is coming in approximately 10 points higher than what we would have anticipated. So if you go back to the 18% to 20% that we've communicated before as a planning assumption that we had back a year or two ago, if you look at the new calculation, you would put that at 26% to 27%.

Now, I caution you about locking in on that number. I'm only giving it to give you a relative perspective versus where we were. Because obviously that number could move, and in all likelihood, I think it will move some. I don't think it will move dramatically, but I think it will move some.

So we factored in all of this pricing that we've already seen. You've seen some of that in our fourth quarter estimates. So you can basically look at that and factor that through 2019 as well. We factored that into all of our estimates, and we factored in further room for more downside...

And while 2018 certainly sets a very high bar for performance, we expect strong earnings growth once again next year. Although it's too early to provide specific growth targets for 2019 as we're still in the midst of our annual planning process, based on our strong underlying business momentum, we are confident in our ability to deliver double digit earnings growth once again in 2019.

And importantly, we expect to deliver this level of growth despite a number of factors including direct biosimilar competition, impacting our more than $6 billion international HUMIRA business; a difficult comparison year, particularly in light of the rapid ramp of our HCV business in 2018; and the significant investment we will be making in 2019 to support new product launches."

Besides the overhang of Humira's growth trajectory in international markets, adding to the selling pressure was news that the FDA just approved Novartis' (NVS) biosimilar Myrimoz for sale in the U.S. This news broke on the same day as the 80% Humira EU price cut. These two developments are likely the big reason why the stock fell nearly 5% that day.

So what do all of these developments mean for AbbVie's dividend safety? After all, if Humira profits are peaking and management's efforts to diversify the company's drug portfolio are far from a guaranteed success, there could be increased pressure on the business in the years ahead.

Is AbbVie's Dividend Still Safe?

In short, yes. Management even announced an 11.5% dividend increase when AbbVie reported earnings last week. Let's take a closer look at the factors that continue supporting AbbVie's payout.

Pharmaceutical sales, earnings, and cash flow are usually quite defensive thanks to the high margins of patent-protected drugs and the non-discretionary nature of healthcare spending to fight various illnesses. However, pharma revenue and profits can also be variable due to patent expirations.

Fortunately for AbbVie, while its EU Humira patents expired in 2018, the firm still has strong patent protection in place in the U.S., where about two thirds of Humira sales are generated.

Currently U.S. Humira sales are growing at a mid-teens pace (12.5% last quarter), driven by volume growth and price increases. AbbVie has also recently cut deals with all its major rivals who have biosimilars coming to the U.S.. This includes Amgen (AMGN), Samsung Bioepis, Mylan (MYL), and most recently Novartis.

These agreements mean that not only should AbbVie face little to no Humira biosimilar competition in the U.S. until 2023, but it will also receive a royalty payment on any biosimilar sales.

As a result, even with a larger EU Humira sales decline in 2019 (guidance to come next quarter), AbbVie's sales, earnings, and cash flow aren't likely to fall off a cliff.

In fact, the company's other blockbuster drugs (like cancer drug Imbruvica) likely will still drive positive sales and bottom line growth next year. Furthermore, analyst firm EvaluatePharma expects Humira to remain the best-selling drug in the world all the way through 2024 (when it will still be generating an estimated $15.2 billion in annual revenue).

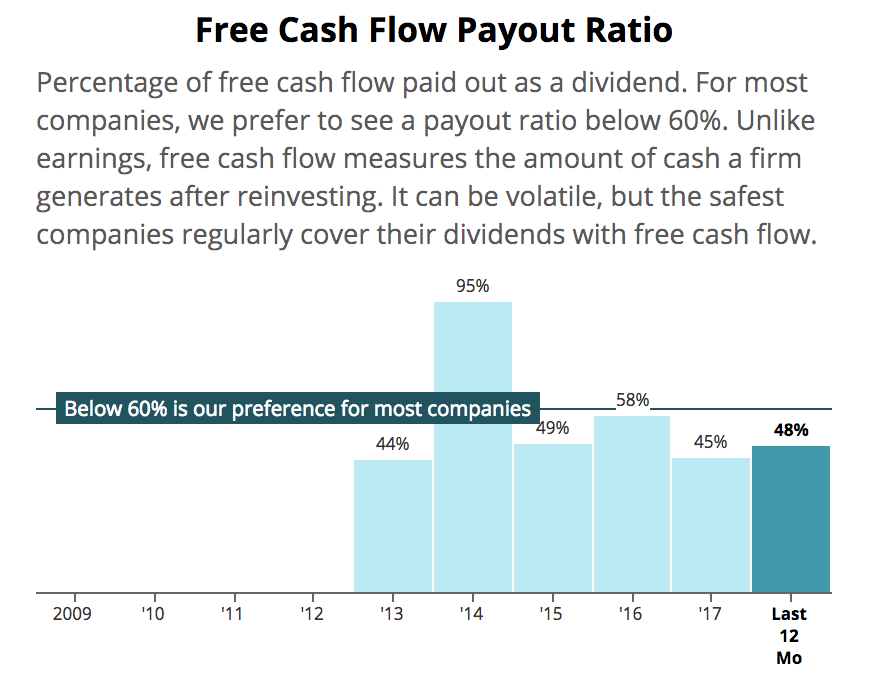

Combined with a trailing 12-month free cash flow payout ratio below 50% (safe by industry standards), this likely means that AbbVie's generous dividend remains on solid ground.

Source: Simply Safe Dividends

What about AbbVie's debt levels? If those are too high, might that not force management to cut the dividend in order to retain more cash to deleverage and diversify and the company's drug portfolio?

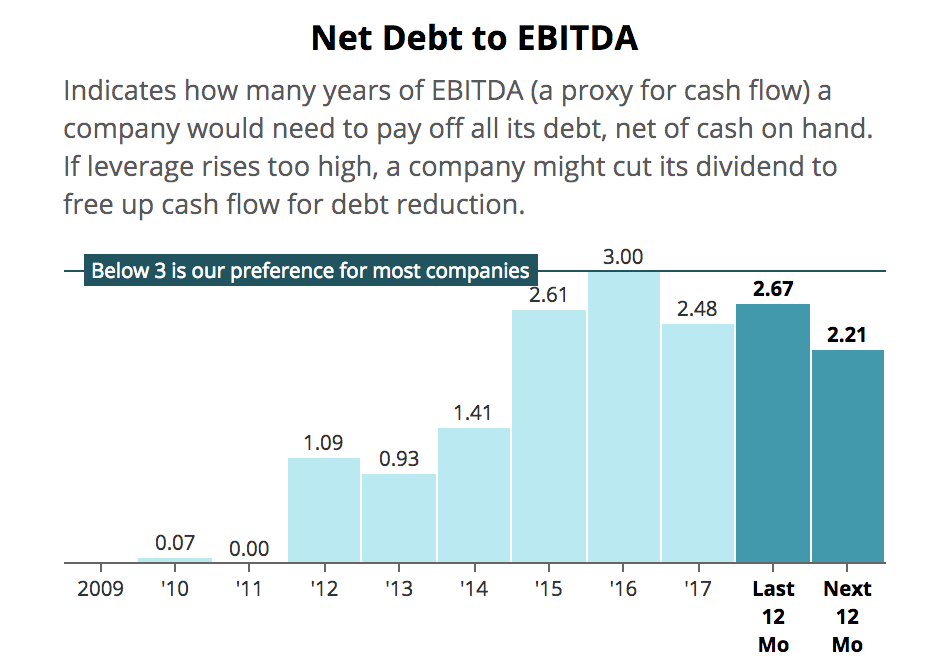

While that's always a valid concern, AbbVie's net debt to EBITDA (leverage) ratio is expected to sit at 2.2 times over the next year. As you can see, the company's leverage has been falling since 2016. AbbVie, like many pharma companies, uses debt to fund acquisitions, and in 2015-16 the firm paid more than $25 billion to acquire Pharmacyclics and Stemcenterix.

Source: Simply Safe Dividends

Currently management is focused on organic growth via bringing one of the strongest drug development pipelines in the industry to market (more on this in a moment). With no major acquisitions expected for the foreseeable future, coupled with AbbVie's strong A- credit rating and low borrowing costs, it seems very unlikely that the firm's balance sheet would jeopardize its dividend.

However, just because a dividend isn't at strong risk of being cut doesn't necessarily mean a high-yield stock is worth buying.

What About AbbVie's Long-Term Growth Prospects?

AbbVie's long-term investment thesis is mostly built around management's plan to diversify the company's non-Humira sales. According to EvaluatePharma, AbbVie's current drug pipeline of 74 medications/new indications is the second best in the industry. By 2022, AbbVie's pipeline is expected to generate $21.2 billion in additional sales for the company.

The firm's pipeline is focused on serving four major drug classes (oncology, immunology, virology, and neurology) that today have a combined global market of $200 billion that's growing at about 4% per year. AbbVie's strongest near-term non-Humira drugs include:

Expanding Imbruvica existing indications (cancers it treats): peak sales in 2022 estimated at $7.5 billion

Psoriasis drug Risankizumab: a competitor to Johnson & Johnson's Stelara ($4 billion in annual sales)

Cancer drug Venclexta (joint venture with Roche): already winning approvals and peak annual sales projected at $3 billion by 2022

Upadacitinib: oral immunology drug (to replace Humira), recent trials show remission rates of 66%, double the current standard of care

AbbVie has an above-average track record on R&D, specifically in its drugs winning approvals and making it to market. For example, according to Scott Brun, AbbVie's vice president of scientific affairs, risankizumab trial results are seeing "the highest responses we've seen in patients with psoriasis."

Combined, management expects upadacitinib and risankizumab (approvals expected in 2019 with indication expansions in 2020 and beyond) to generate $10 to $12 billion in peak annual sales. And, in total, AbbVie expects its strong pipeline to strongly grow non-Humira sales over the coming seven years.

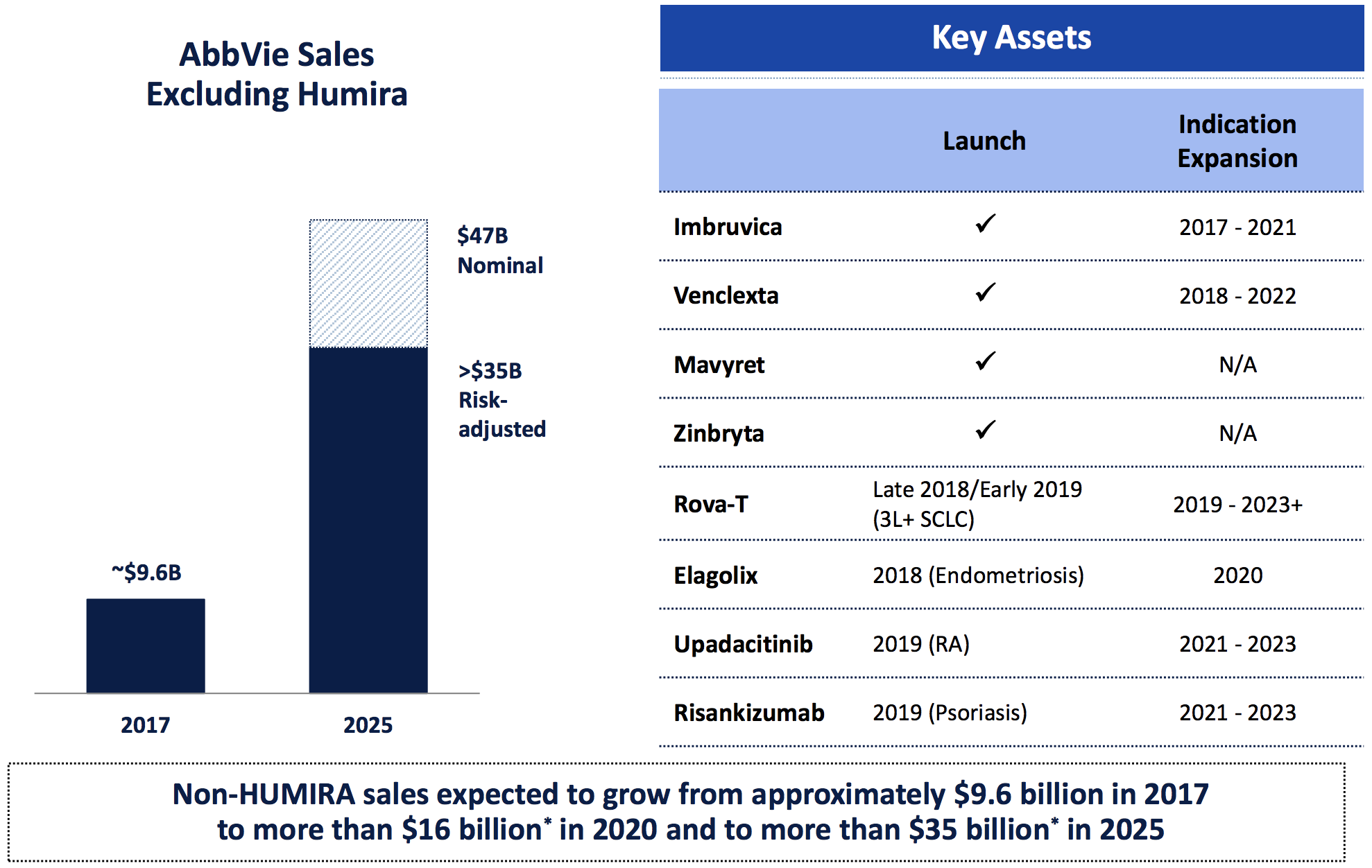

Adjusting for the risk of drug trial failures, AbbVie expects that by 2025 non-Humira sales will amount to $35 billion. Assuming the most pessimistic analyst estimates on Rova-T's future sales, that would fall to $32 billion.

But even in that scenario, AbbVie's Humira concentration could drop from 63% today to 27%. More importantly, overall sales, earnings, and cash flow would continue growing at a healthy clip.

Source: AbbVie Investor Presentation

A larger than expected price cut on Humira in the EU will likely reduce both management guidance and analyst growth expectations a bit. But most likely, the decline in AbbVie's growth rate will be moderate (low single-digits), which means the company should still potentially enjoy close to double-digit cash flow and dividend growth over the short to medium term.

Investors considering the stock just have to be prepared for perhaps heightened volatility and the market continues adjusting its long-term growth expectations for Humira and AbbVie's blossoming drug pipeline.

Closing Thoughts on AbbVie's Dividend and Long-term Appeal

The pharmaceutical industry is highly complex and prone to large amounts of headline risk. Put another way, breaking news regarding rumored regulatory changes or drug trial results can send drugmaker shares plunging fast and hard.

And thanks to the long and costly drug approval process (can take more than a decade and cost hundreds of millions of dollars), it's not always easy to know how quickly a pharmaceutical company's profits will grow in the future, or even if they'll grow at all. AbbVie's major dependence on Humira makes that statement even more true.

Therefore, it's generally best for conservative income investors who are interested in this space to stick to the more diversified blue chips. Those with strong balance sheets, balanced drug portfolios, and a good track record of delivering safe and growing dividends. Johnson & Johnson (JNJ) and Merck (MRK) are two examples.

There's nothing necessarily wrong with investing in AbbVie, especially with its shares having fallen so far and its dividend remaining safe, but investors must be comfortable with the firm's current Humira concentration and management's long-term diversification strategy.

Until more clarity is provided over the next few years, the stock could remain volatile as long-term growth expectations continue adjusting based on the latest Humira patent protection developments, drug pipeline progress, and any regulatory changes that make it to the finish line.