Income investors are often attracted to mouthwatering yields, and L Brands' (LB) 7% payout certainly qualifies.

Founded in 1963, L Brands operates over 3,000 company-owned retail stores, primarily under the Victoria's Secret and Bath & Body Works brands. Most of its locations are mall-based.

By building up dominant brands in the lingerie, beauty, and fragrance niches, L Brands has been a great success story over the last few decades.

In 1993, L Brands ran 545 company-owned Victoria's Secret stores and had 121 Bath & Body Works locations.

Today its Victoria's Secret locations have more than doubled to 1,165 stores, and Bath & Body Works' footprint ballooned over 10 times to a whopping 1,703 shops. Along the way L Brands also developed and sold off popular chains including Express, The Limited, Abercrombie, and Lane Bryant.

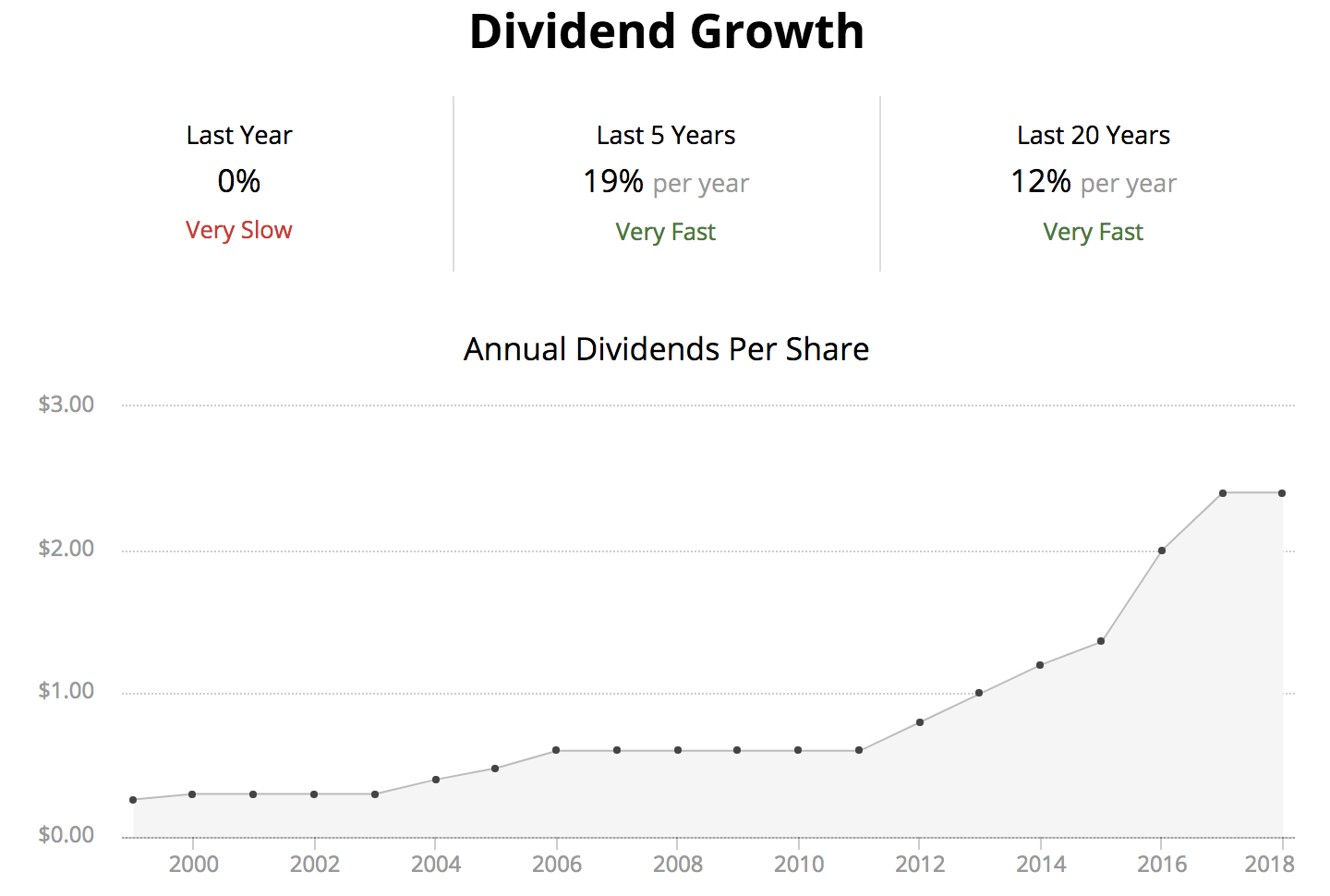

Thanks to its success in the brick-and-mortar retail world, the firm boasts an impressive track record of paying dividends without reduction for more than 25 consecutive years.

Source: Simply Safe Dividends

However, the past isn't always a guide to the future. Let's take a look at why L Brands appears to have one of the riskier dividends in the market and faces a potentially challenging long-term turnaround.

L Brands Continues to Struggle With Its Turnaround

L Brands owns some great brands, but its Victoria Secret business (64% of sales and 49% of operating income) has been struggling to adapt to the rise of e-commerce, changes in consumer culture, and declines in lower quality malls where around half of its stores are located, per The Wall Street Journal.

Part of the problem is arguably L Brands' iconic 81-year-old CEO and founder Les Wexner, who claims the title of the longest serving CEO of an S&P 500 company. The Wall Street Journal wrote an excellent piece here detailing Mr. Wexner's retail philosophies and growth strategies for the company.

He's a big believer in the importance of physical store locations, surmising that as long as "the store environment is exciting, I'm convinced people want to go to the store." In the article, he goes on to state his belief that the fascination with smartphones will fade and the internet won't kill his stores.

While the jury is still out on those contrarian claims, L Brands focus on growing its store count in recent years (net store count is up 30 locations year-to-date) while most other retailers are contracting their footprints has not helped its results. Nor has the company's decision to direct the majority of its capital investments to store improvements rather than omni-channel initiatives.

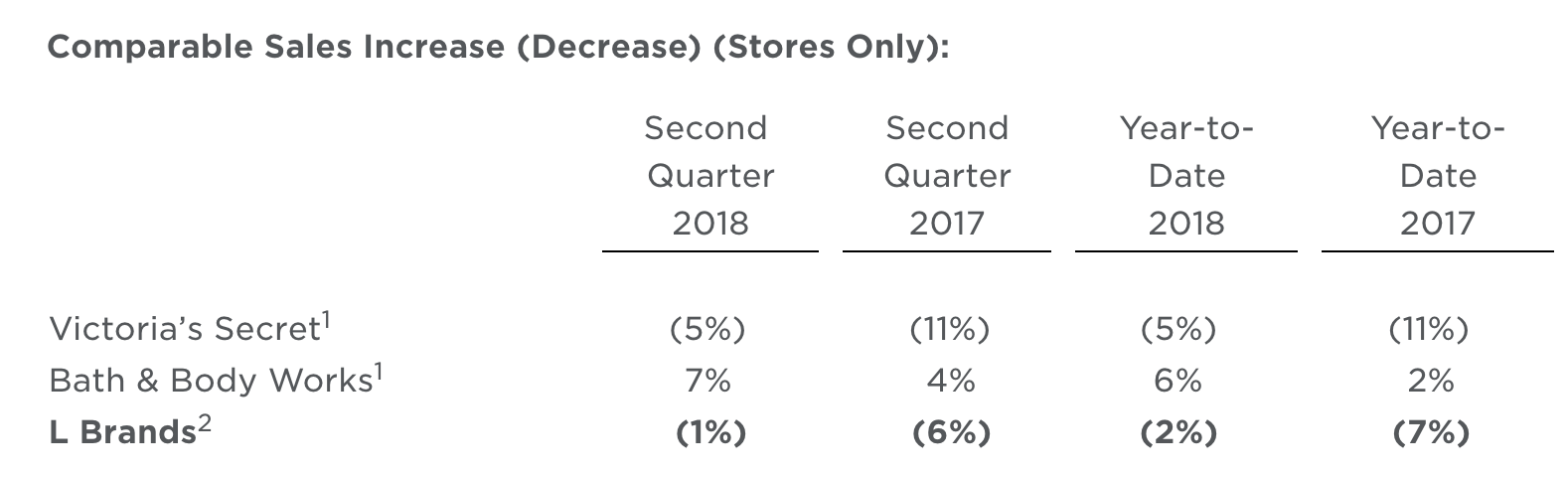

As you can see, L Brand's year-to-date comparable sales from stores open at least a year are down 2% overall, driven by a 5% slump at Victoria's Secret.

Source: L Brands Press Release

Making those figures even worse, L Brands' disappointing growth has come while the company has discounted much of its merchandise in an effort get more people into its stores to buy its products. The firm's gross margin is down from 37.2% year-to-date in 2017 to 35.7% this year.

Since physical stores have high fixed costs (rent, utilities, labor are largely fixed no matter how much merchandise is sold), the drop in comparable sales and gross margins has really hurt L Brands' bottom line. Specifically, operating income is down 25% year-to-date compared to 2017.

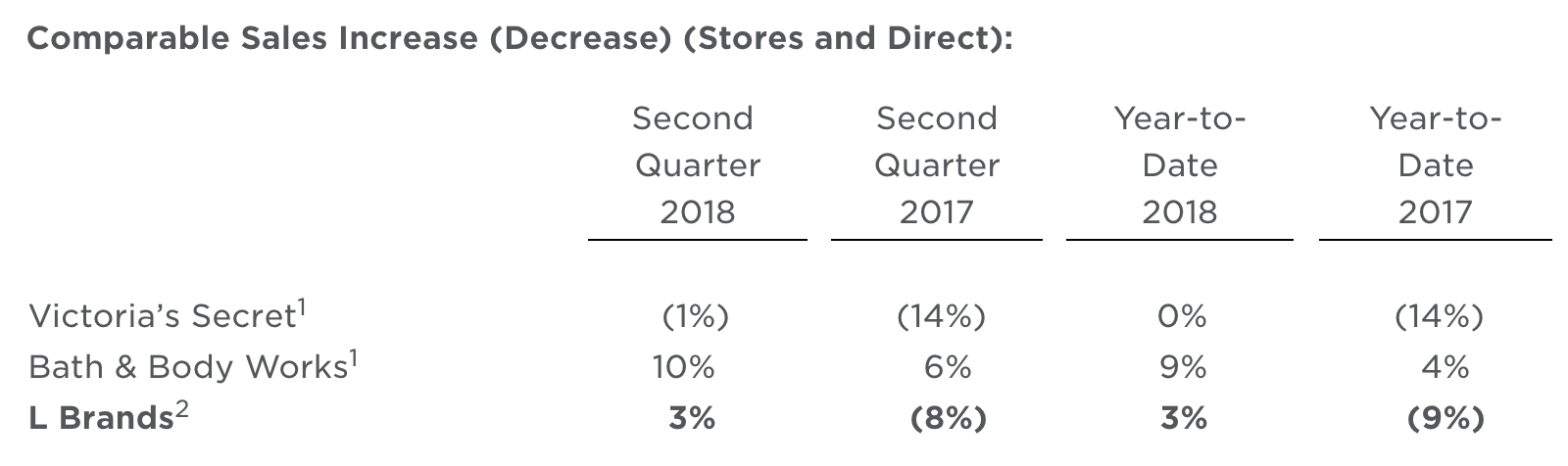

Now it's not all bad news. Around 20% of the company's sales are derived online, and Victoria's Secret's comparable sales would actually be flat year-to-date if online sales are included, putting company-wide comparable sales into the black.

Source: L Brands Press Release

However, with such a massive store footprint, the company's brick-and-mortar locations seem likely to remain an anchor on its financial health unless top line trends quickly reverse at Victoria's Secret storefronts.

Besides the company's questionable strategic choice to continue expanding its physical footprint in the age of the internet, the Victoria's Secret chain also seems to be missing a cultural shift.

Specifically, there seems to be a growing movement against the supermodel image of women pushed by Victoria's Secret. Instead, a growing number of women want to embrace authentic images, which doesn't exactly jive with the company's marketing and form-fitting products.

New, tech-savvy competitors are no doubt looking to capitalize on these trends, which is one reason why L Brands has resorted to higher promotions to try and protect its market share. However, discounting doesn't seem to be a wise long-term strategy, and financial pressure is rising as the company scrambles to find opportunities for profitable growth.

In fact, earlier this year management slashed 2018 earnings per share guidance by 20% due to heavier spending, mostly tied to international expansion efforts.

The good news is that L Brand's has managed to somewhat stabilize Victoria's Secret overall revenue, thanks to a bigger focus on online sales. That's because operating margins on its e-commerce sales are actually somewhat higher than the profitability achieved by its physical stores.

In the second quarter of 2018, the firm's online sales of Victoria's Secret products increased 22%. However, they account for just 12% of total revenue for that brand which calls into question how quickly L Brands can return to positive bottom line growth. That's especially true given that management is still investing heavily into expanding physical stores for Bath & Body Works as well as internationally.

For instance, management plans to expand its domestic square footage modestly in Bath & Body Works (low single-digits), but expand overseas (especially China) by around 25% per year. As a result, the company will be investing heavily into new physical locations overseas which will take a major toll on its already struggling earnings and cash flow.

L Brands' Dividend is on Thin Ice

For starters, since June 2016 L Brands has frozen its dividend, which is a potentially troubling sign given that the economy has been growing stronger and retail sales are booming.

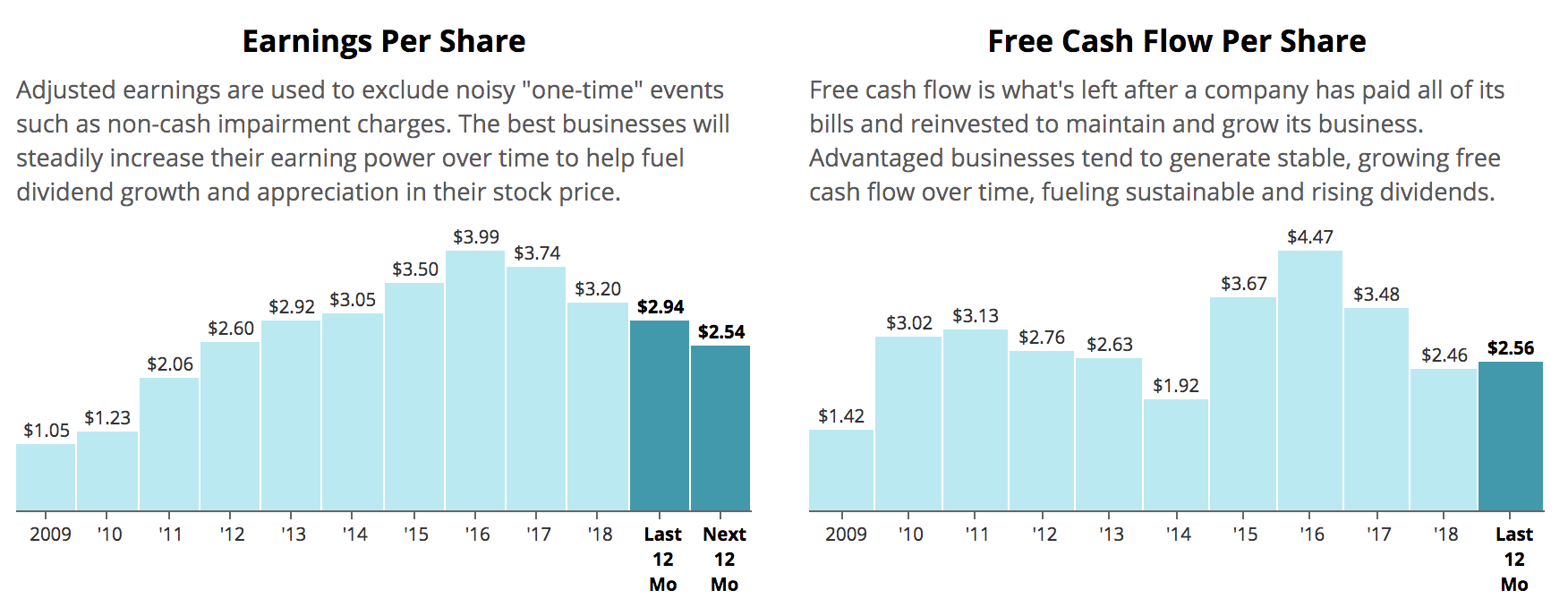

The company's dividend profile begins to get uncomfortable as soon as you look at L Brands' payout ratios. Despite slowly but steadily rising sales over the last few years, fueled by new store openings and online growth, the company's earnings per share and free cash flow per share peaked in 2016 and have declined significantly.

Source: Simply Safe Dividends

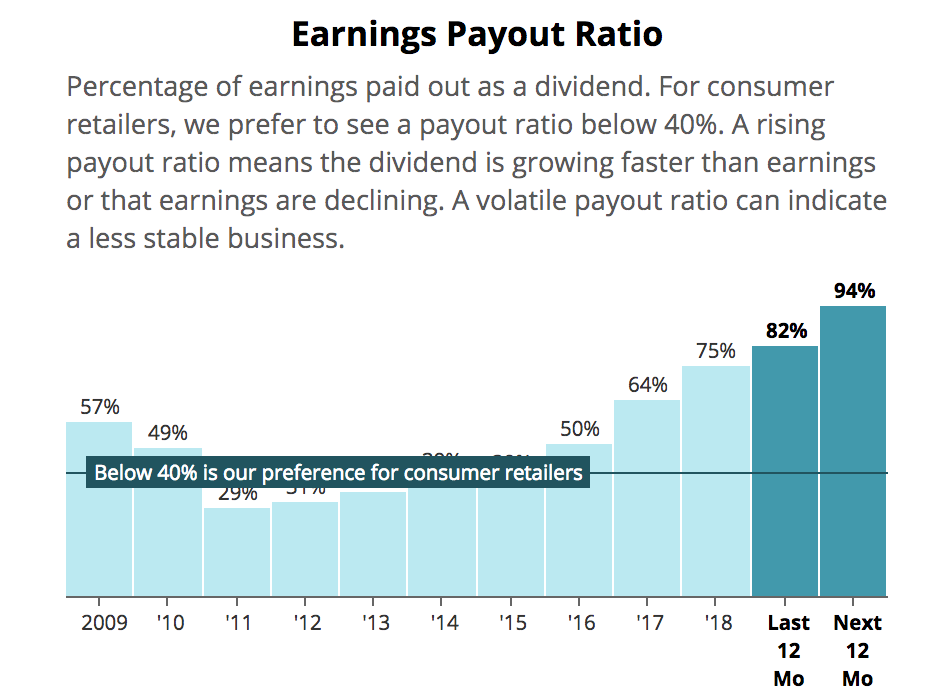

The company's slump in profits underscores the margin pressure the business has been under, as well as the large-scale reinvestments the company has had to make. The end result is a dangerous payout ratio expected to exceed 90% over the next year, marking its highest-ever level.

Source: Simply Safe Dividends

While a payout below 100% is technically sustainable, it leaves no safety cushion should the company's results come in below expectations (yet again). It's even more alarming in light of L Brands' lackluster balance sheet.

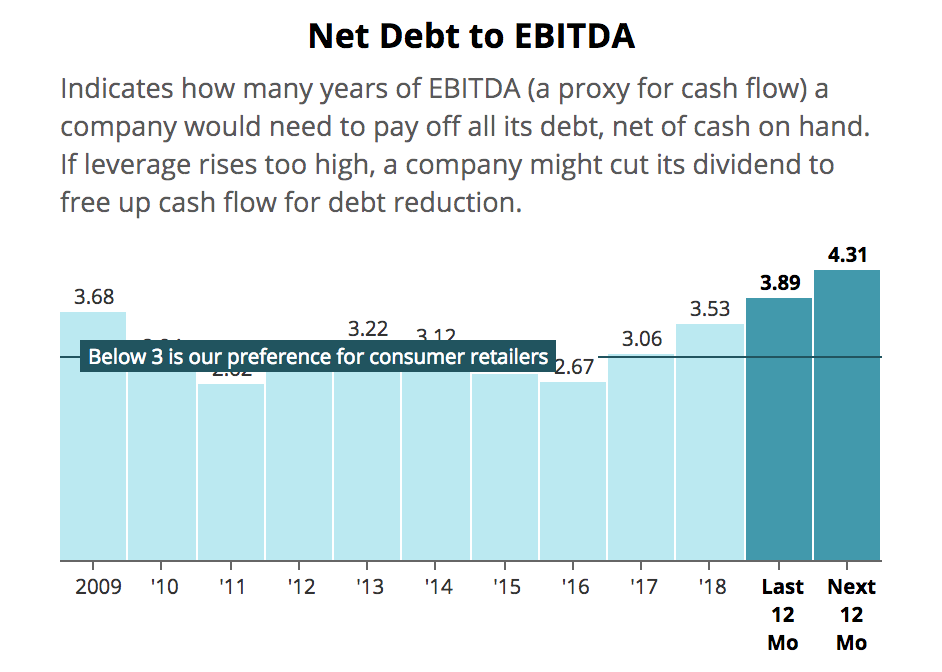

The company's debt levels have remained persistently high, at nearly $5.8 billion. With $843 million in cash on the balance sheet (down from $1.9 billion a year ago), L Brands' net debt to EBITDA ratio stands at 3.9 today but is expected to deteriorate to 4.3 over the next year as its profits remain under pressure.

Source: Simply Safe Dividends

The company's high debt level and junk bond credit rating (BB) indicate that L Brands has little financial flexibility left. Worse, its high payout ratio results in little to no retained cash flow that can go towards funding its capital-intensive turnaround efforts and reducing its leverage.

Simply put, as long as the dividend is maintained, the company is living on borrowed time and must continuously refinance its long-term debt. With the dividend consuming over $650 million annually, a major reduction (50-90%) would provide the company with much more breathing room.

However, management is not backing away from the dividend. At least not yet. The company recently announced plans to exit two of its smaller chains, La Senza and Henri Bendel. These two retailers were on pace to generate approximately $335 million in 2018 revenues, but they were also operating at a loss of $85 million. This is a step in the right direction, but it doesn't solve the problem of generating long-term profitable growth.

In August 2018 during L Brands' second-quarter earnings call, the company's CFO Stuart Burgdoerfer told analysts that management is "comfortable with the dividend today."

However, that comfort is based on expectations that strong holiday sales will boost revenue, earnings, and cash flow. Should that happen, management believes L Brands' dividend yield will revert to a "more normal range."

However, if holiday sales disappoint, or an economic downturn were to occur in the next few years, management's comfort with its current dividend could rapidly diminish. Given the firm's payout ratio and stretched balance sheet, there is no margin for error.

Michael Binetti, Analyst at Credit Suisse You guys have remained very committed to a very, very high dividend yield despite I think the operating results coming in below some of your this year. I know you've worked hard to moderate CapEx down a few times along the way but could you help us in how you think about holding steady the approach of the capital deployment in contrast the variances you've seen in the operating plans?

Stuart Burgdoerfer, CFO at L Brands Important subject obviously, important source of return for shareholders. Obviously the payout ratio is abnormally high. The yield is very high. We look at it regularly management does. We have the appropriate conversations with our board. Obviously a lot of our earnings and our cash coming to fourth quarter, we have conversations about this regularly. But importantly as we have more insight into holiday results we're comfortable with the dividend today have the free cash flow to support it but it's obviously something that should be looked at periodically and we do.

We're comfortable with that. We expect to one way to deal with the payout ratio is obviously to increase earnings that's what we're focused on. Earnings increases will drive obviously an increase in the share price and get dividend yields in relationships like that in a more normal range.

But with that said our operating performance has lagged our expectations over the last several years. So we look at it periodically in a rigorous way. That will continue. We're comfortable with it based on what we know at this point and we'll continue to look at it.

It's hard to feel very reassure by management's conditional statements about the dividend's safety, especially given the real challenges the business faces. Simply put, income investors in L Brands could be in for many more years of handwringing about the precarious nature of this retailer's dividend.

Closing Thoughts on L Brands

It's understandable why a 7% yield would seem attractive in this age of low interest rates. However, remember that L Brand's yield is in the stratosphere precisely because its dividend safety has been declining for the past three years.

While sales have managed to grow slowly over that time, the company's major reinvestments into remodeling its Victoria's Secret stores, expanding internationally, and pushing more into online commerce has meant steadily falling free cash flow and earnings that have pushed its dividend payout ratios to dangerously high levels.

And thanks to a highly leveraged balance sheet, L Brands has very little flexibility when it comes to financing its turnaround efforts. With its borrowing costs already pushing 7% and interest rates potentially set to rise in coming years, there is a very real risk that, despite management's claims of a sustainable dividend, the payout may have to be cut. Perhaps as early as next quarter if holiday sales miss expectations.

Even if management finds a way to preserve the dividend, a company like L Brands is one we try to avoid. Given the amount of leverage involved, there is a wide range of potential outcomes for this investment opportunity. Sure, a successful turnaround could mean the stock doubles, but there's also still real downside if earnings do not improve sooner rather than later.

Overall, L Brands seems most likely to be a "yield trap" that's best avoided. As conservative income investors, we prefer to invest in businesses with clearer paths to profitable long-term growth, low payout ratios, and strong balance sheets.