IBM's Dividend Remains Safe, But Red Hat Acquisition Raises the Stakes

On October 16, IBM (IBM) reported disappointing earnings that sent shares plunging nearly 8% the next day. This week shares continued tumbling after IBM announced plans to acquire software company Red Hat (RHT) for $34 billion.

As a result, IBM's stock now trades at its lowest price since 2009, and its other valuation metrics also make it, at least initially, appear like a bargain hunter's dream stock:

Forward P/E Ratio: 8.2 (lowest in over 10 years)

Dividend Yield: 5.4% (all-time high)

But given that IBM's shares peaked in mid-2013 and have since fallen more than 40% from their all-time high, long-term investors have still suffered mightily over the years. Even accounting for the company's generous and growing dividend, since its peak IBM has lost more than 30%.

So many income investors want to know, is now a good time to be "greedy when others are fearful?" Or is this struggling technology giant a value trap to be avoided?

While the firm's dividend has historically been on very solid ground, our longtime readers know I've been an IBM bear for years. If you're interested, you can read the initial note I posted on the company in August 2015 here.

However, doing my best to put my biases aside, let's take a look at why the market is so bearish on Big Blue, if the dividend remains safe, and whether this high-yield stock appears to be a reasonable long-term investment with so much pessimism now priced in.

IBM's Growth Struggles Continue

Before looking at the Red Hat acquisition, which will account for less than 5% of company-wide sales, IBM's core operations deserve attention.

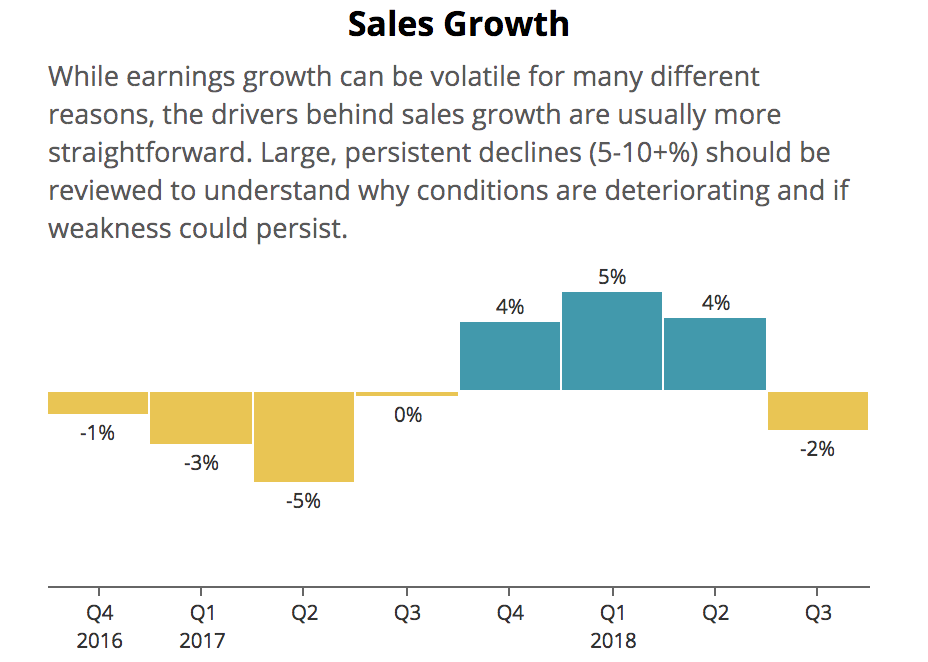

Earlier this year IBM investors were hoping that after 22 consecutive quarters of year-over-year revenue declines, the company had finally turned a corner. In the last three quarters before this one, IBM managed to post modest quarterly sales gains.

Source: Simply Safe Dividends

However, those quarters largely benefited from currency exchange rate tailwinds and the launch of the new Z14 mainframe server, which caused a temporary spike in sales.

IBM's short-lived revenue growth streak broke in the third quarter. The company reported flat sales growth, and -2% revenue growth after adjusting for currency fluctuations.

More troubling was that the company's Cognitive Solutions segment (23% of revenue, 46% of operating income in 2017), home to the famous Watson AI platform and expected to be an important growth engine, saw a 5% sales decline in constant currency.

One of the few bright sides to IBM's results was an increase in gross margins, which indicates the company's declining profitability (since 2014) may have bottomed.

More importantly, the Strategic Imperatives (SI) businesses, which represent IBM's future tech lines across important areas such as data analytics and cybersecurity, have seen 11% constant currency growth over the past 12 months, including a 24% increase in cloud computing revenue.

IBM is counting on continued double-digit sales growth from these businesses to offset its declining legacy hardware sales and ultimately restore it to positive top and bottom line growth.

However, the news surrounding SI and cloud computing wasn't all good. While the trailing 12-month sales growth was impressive, the quarterly figures were far less so:

Q3 SI revenue growth: 7% (and down 8% from Q2 2018)

Q3 Cloud revenue growth: 10% (Q2 growth was 20%)

The sharp deceleration in IBM's future tech divisions caused SI sales to once more fall below 50% of company-wide revenue, which is the benchmark management set as its 2018 goal.

This deceleration, which came despite a continued pickup in economic growth and IT spending, casts more doubt over whether Big Blue will be able to compete with larger and more dominant tech giants in the industries of the future. Regardless, for 2018 IBM is still guiding for:

"at least" $13.80 per share adjusted EPS; flat compared to 2017

$12 billion in free cash flow; -8% compared to 2017

With IBM's results once again disappointing, management did what many other growth-challenged giants do: buy growth.

IBM to Acquire Red Hat On October 29, IBM announced it would acquire Red Hat for $34 billion, its largest-ever acquisition.

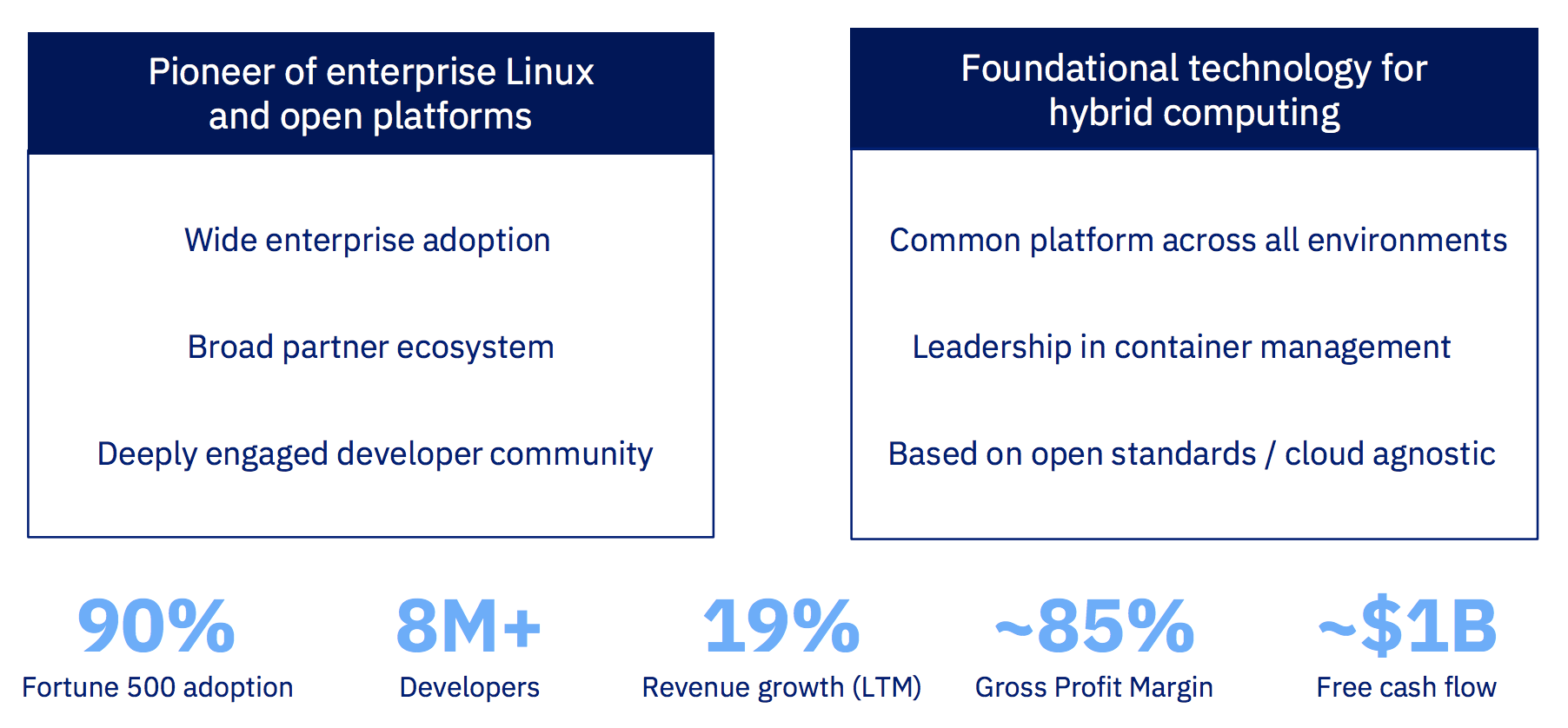

Red Hat has been in business for 25 years and essentially provides corporations with software they need to effectively manage their applications across their in-house data centers and with cloud providers such as Amazon (AMZN), Microsoft (MSFT), and IBM.

IBM claims that 80% of enterprise workloads have yet to migrate to the cloud. The idea is that many companies will opt to keep some of their computing on their own servers while migrating other programs to various cloud providers. Red Hat helps make that work easier for software developers.

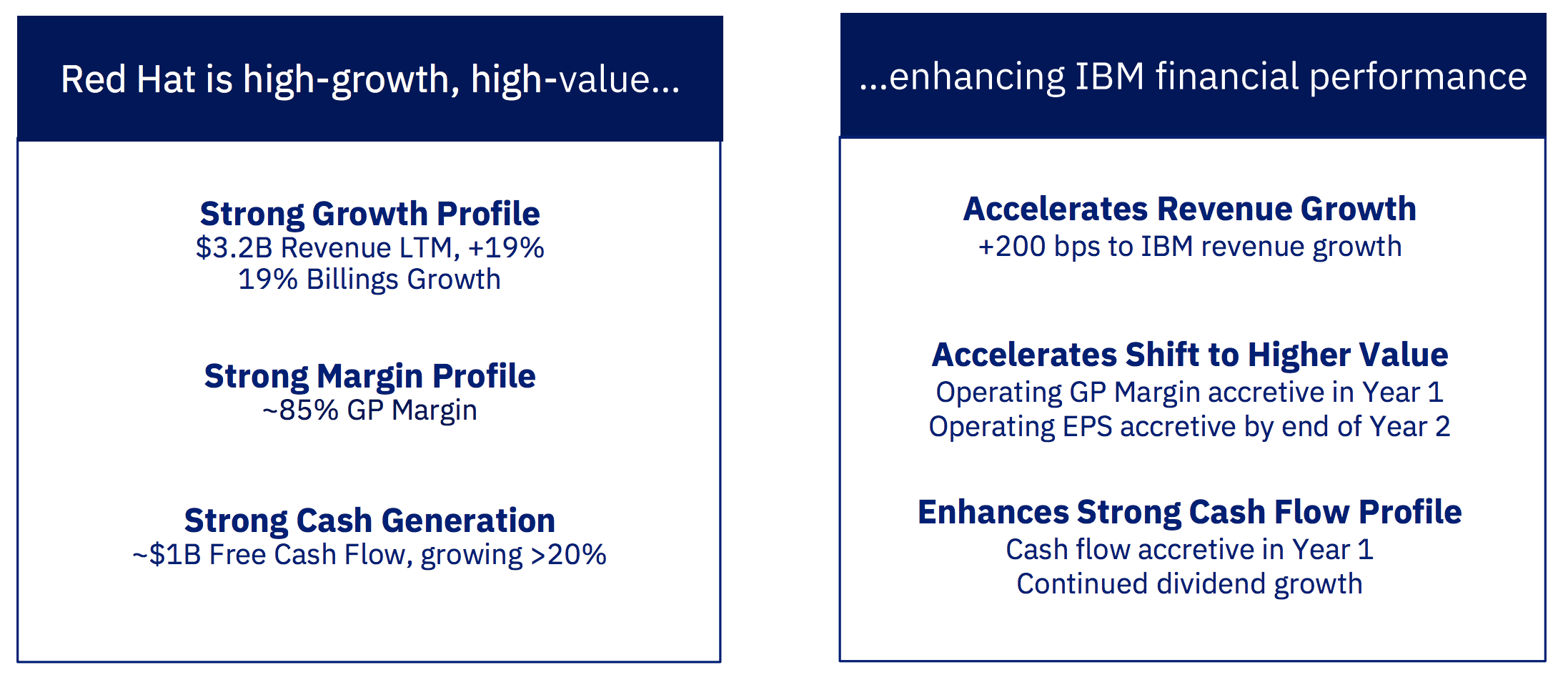

Red Hat's business model is certainly appealing. Mature software companies are known for their impressive profitability and excellent cash flow generation. Red Hat sports an 85% gross margin, does business with 90% of the Fortune 500 companies, grew revenue nearly 20% over the past year, and has a free cash flow margin north of 20% (compared to IBM's 8%).

Source: IBM Investor Presentation

Thanks to Red Hat's impressive metrics, IBM expects the deal to boost its revenue growth by 200 basis points and improve its gross margin and cash flow per share in the first year after closing.

Source: IBM Investor Presentation

Of course, a company like this doesn't come cheap. IBM is paying over 10 times trailing sales and over 30 times free cash flow for Red Hat. If Red Hat doesn't continue its growth trajectory, or the hybrid cloud landscape shifts in a way management did not expect, shareholders will be regretting this risky deal.

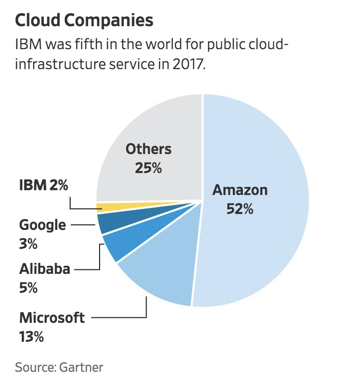

On the other hand, IBM needed to do something. The company was losing in cloud and, based on its lackluster quarterly growth figures, wasn't showing enough signs of being able to start closing the gap with its major rivals.

Source: The Wall Street Journal

Like with most things, it will take time to gauge how wise the Red Hat deal ultimately is. However, given the steep price tag and the risks involved, not to mention IBM's poor reputation of acquiring businesses only to ruin the cultures that made them successful, investors have fair reasons to remain skeptical of this strategic acquisition.

Regardless, what does IBM's acquisition of Red Hat mean for its dividend?

Dividend Is Safe For Now But Overall Investment Thesis Is Weakening

Despite IBM's chronic sales declines, its payout has remained on solid ground for years. Two factors primarily supported the firm's attractive dividend safety profile.

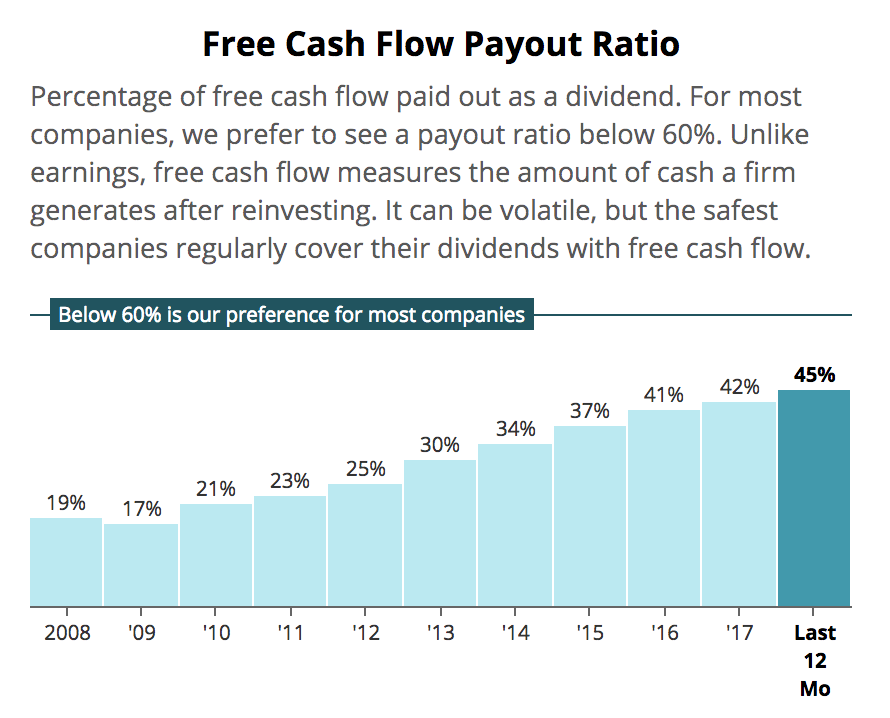

First, while IBM's free cash flow payout has increased significantly over the last decade, it remains at a reasonable level of 45% today. The company retains around $6 billion of free cash flow after paying dividends that can be used to reinvest in growth opportunities, maintain a strong balance sheet, make strategic acquisitions, and opportunistically repurchase shares.

Red Hat is expected to increase IBM's cash flow per share in year one, so the acquisition shouldn't pressure the company' payout ratio.

Simply put, despite IBM's growth struggles, its payout ratio does not suggest its dividend is in danger, especially given the firm's balance sheet.

Source: Simply Safe Dividends

Some companies with reasonable payout ratios will still cut their dividends if they feel a need to deleverage more quickly. That can be especially true following a large acquisition.

One of IBM's key strengths from a dividend safety perspective was its pristine balance sheet. Prior to the Red Hat deal, the company maintained conservative leverage ratios which earned it an 'A+' credit rating from Standard & Poor's. After the acquisition was announced, its credit rating was downgraded one notch.

Source: Simply Safe Dividends

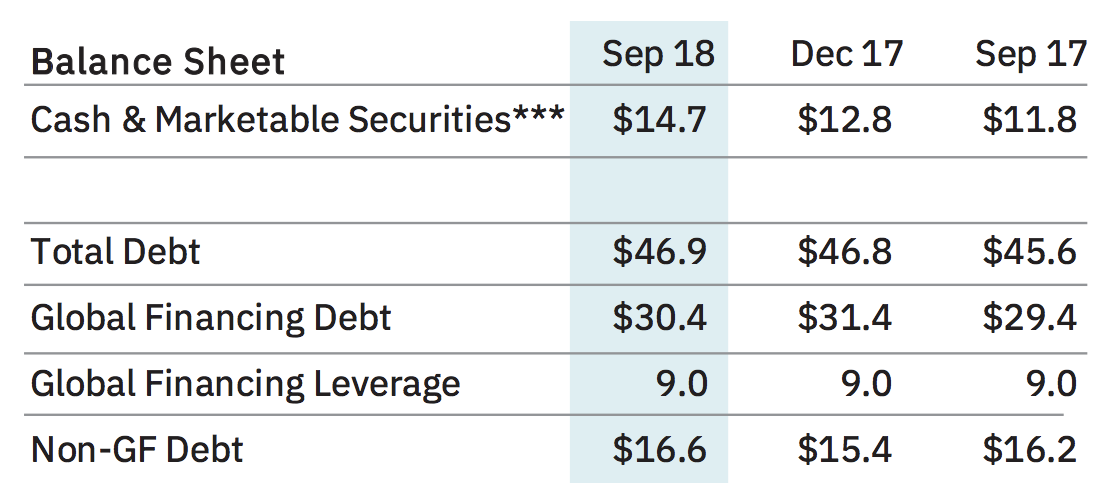

Besides its conservative use of leverage, IBM's dividend safety profile was also bolstered by its healthy cash reserve. The firm held nearly $15 billion of cash compared to just $16.6 billion of non-financing debt and annual dividend payments of about $5.7 billion.

Source: IBM Investor Presentation

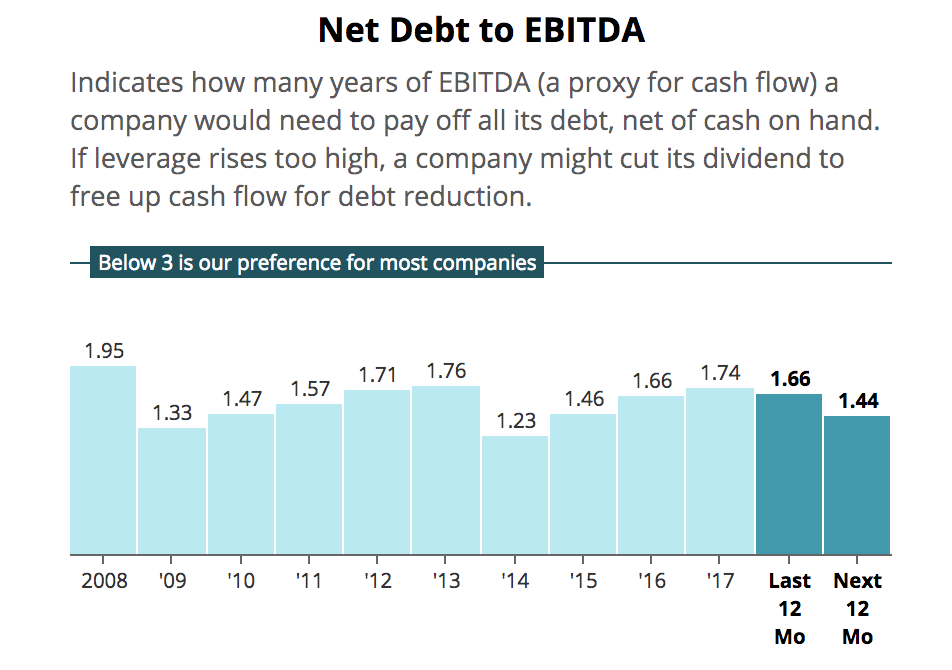

IBM will pay for Red Hat using a combination of cash and debt, which will weaken its balance sheet and debt ratios. Per Moody's estimates, "IBM's pro-forma gross adjusted debt to EBITDA will exceed 3x at closing, up from about 1.7x as of September 30, 2018."

While that's not necessarily a dangerous level of debt, it does raise the stakes. IBM's existing operations need to continue throwing off plenty of free cash flow like they do today to help the company deleverage over the next few years.

As we saw when reviewing IBM's free cash flow payout ratio, the good news is that the firm currently retains a healthy amount of cash flow after paying dividends (around $6 billion) to help reduce its debt load. Investors need to be sure that continues to remain the case in the years ahead.

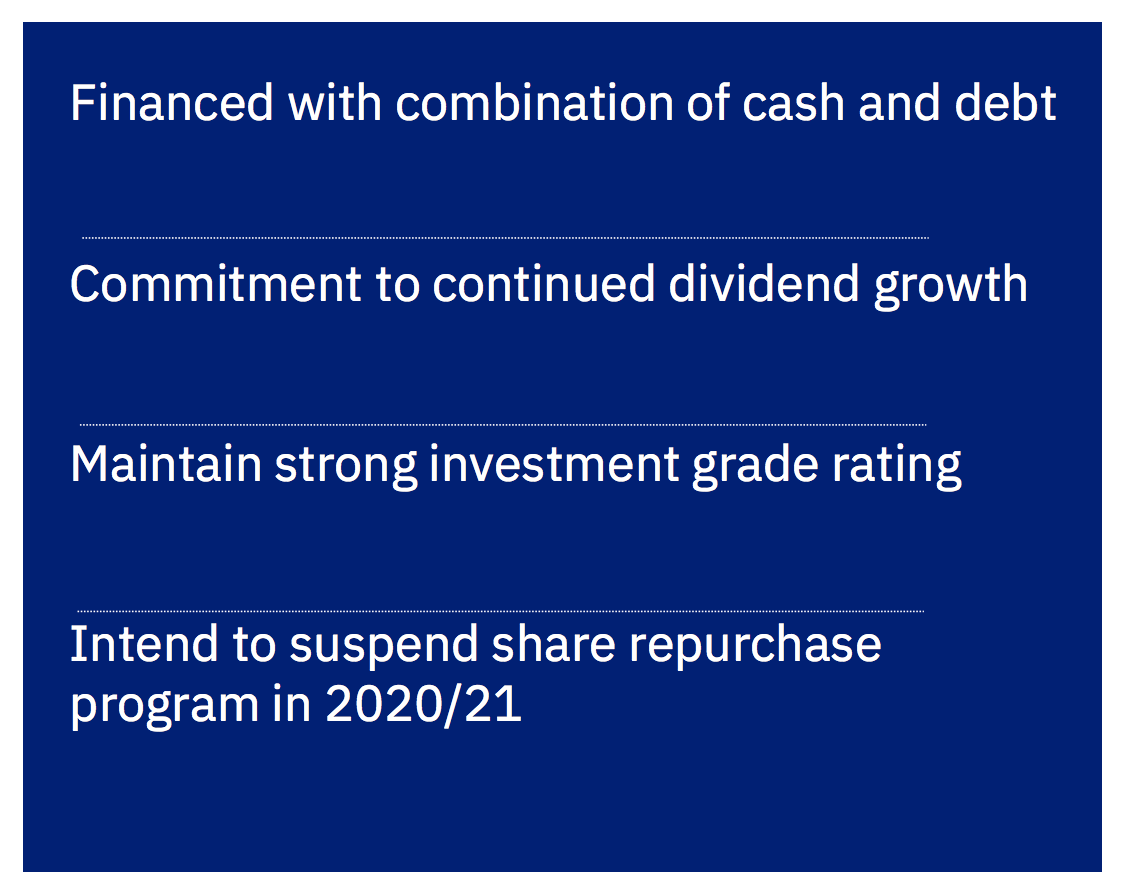

To direct more of its retained cash flow to deleveraging, management also plans to suspend IBM's share repurchase program in 2020 and 2021:

“The company will continue with a disciplined financial policy and is committed to maintaining strong investment grade credit ratings. The company will target a leverage profile consistent wit ha mid to high single digit A credit rating. The company intends to suspend its share repurchase program in 2020 and 2021."

Management expects these actions to allow IBM to continue growing its dividend, albeit at a very moderate pace for the foreseeable future. Based on the information we know today, the company's expectation appears reasonable.

Source: IBM Investor Presentation

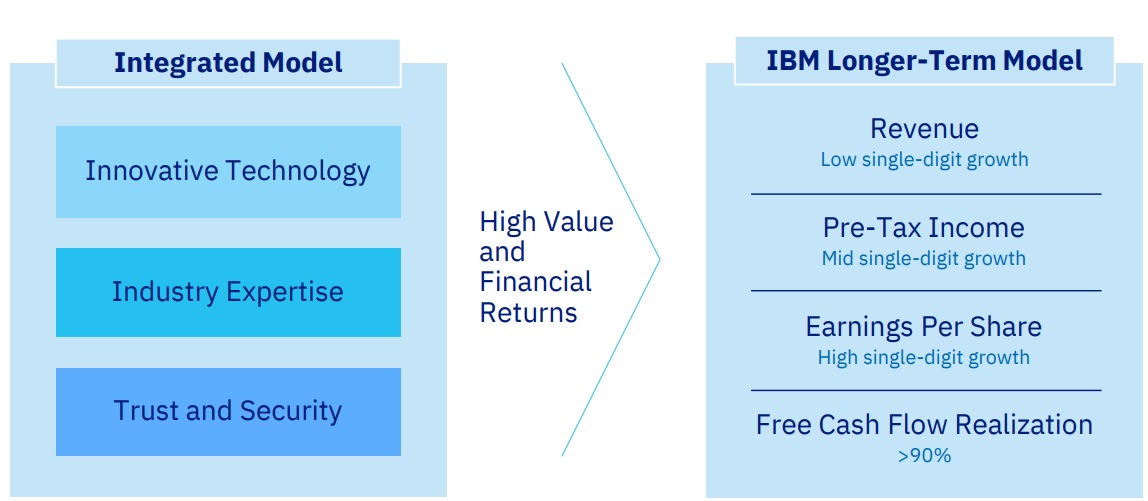

While IBM's dividend remains safe for now, what about the company's long-term growth potential? Well, that depends on management delivering on its promised turnaround, which it has thus far struggled to do.

Source: IBM Investor Presentation

IBM's claims that its turnaround plan can eventually achieve high single-digit long-term EPS and FCF per share growth. If the company were to increase its revenue to drive that level of growth, its stock would likely deliver solid double-digit annual returns.

However, it's important for investors to always take management's guidance with a healthy grain of salt. The growth challenges facing the company are real, and Red Hat won't change that reality overnight.

IBM's future growth is predicated on the continued growth of its strategic initiatives, which is ultimately tied to its cloud computing business.

While the company's 24% growth in cloud computing revenue over the past year is impressive, it's important to put that figure in context.

According to analyst firm Synergy Research, the cloud computing industry is growing about 50% per year. That means IBM is losing market share to dominant players like Amazon, Microsoft, Alphabet (GOOG), and Alibaba (BABA). All of these companies are reporting cloud growth of 50+%.

Source: Synergy Research Group

Why should investors care about cloud market share? Isn't IBM's double-digit cloud growth enough to make it a good investment?

IBM's falling market share in the cloud could hamstring its future turnaround plans, because cloud computing has strong network effects. The more companies move to a specific cloud platform, the more data that company has to feed into its artificial intelligence (AI) or machine learning algorithms.

This leads to better deep data analysis and more useful tools and applications for clients to maximize the profitability of their businesses. In addition, third-party software developers are more likely to develop new apps for the largest platforms, which means that market share matters a great deal.

Ultimately the cloud computing industry is likely to end up dominated by a handful of companies, who can offer the best overall platforms (integrated ecosystems). As IBM's struggles with Watson (cognitive computing) have shown, while IBM is devoting large resources to AI and machine learning, thus far that hasn't translated into strong top or bottom line growth that can keep up with its rivals.

And since IBM's long-term EPS and FCF per share guidance is predicated on achieving much stronger economies of scale (higher margins), market share is very important to the ultimate success or failure of its turnaround plan.

At the end of the day, IBM is facing brutal competition from much larger and well-capitalized rivals. Ones that are devoting far more money into R&D to continually improve their cloud and data analytics offerings. As a result, it's uncertain whether or not IBM's strong double-digit growth in SI can continue, and prove that the third quarter's sharp deceleration in growth was just a fluke.

While IBM isn't likely to cut the dividend anytime soon to devote more resources to R&D in an effort to become more competitive in the cloud, even after its Red Hat acquisition, the risk of a future dividend cut isn't zero.

Back in 1993, the last time IBM was struggling with a major turnaround effort, it fired its CEO and the new one quickly cut the dividend. In fact, IBM ended up cutting its payout twice within three quarters, for a total reduction of 79%.

The current CEO, Virginia Rometty, has been in charge since 2012. Her track record on execution has been poor thus far, and her ouster grows more likely with each passing quarter of poor results.

If Rometty is replaced by the board of directors IBM might end up announcing a major strategic shift that could once more call into question the safety of the dividend, especially if the firm's free cash flow generation has deteriorated.

Closing Thoughts on IBM's Future

IBM's long-suffering shareholders continue to wait for management's much-vaunted turnaround to succeed. This quarter's return to negative constant currency revenue growth shows the wait may be longer than many investors had hoped.

IBM's troubling decline in its Cognitive Solutions business shows that the company's R&D efforts over the years have failed to translate into good fundamental results. Meanwhile, the company's growth in Strategic Initiatives and cloud computing continue to underperform its larger rivals.

In that context, it's not surprising to see IBM take a more drastic measure by making its largest-ever acquisition to become the leader in hybrid cloud computing.

While this isn't a "bet the firm" deal, it does weaken IBM's balance sheet, put more pressure on the firm to maintain its existing free cash flow stream, and create additional operational risk.

As a result of the firm's expected jump in financial leverage from the acquisition, IBM's Dividend Safety Score has been downgraded from 92 to 65, a level that is still "safe." The company's payout appears to remain on solid ground based on the information we know today, but it's not as safe as it was prior to the Red Hat acquisition.

However, the longer the current management team fails to deliver on its promises, the more likely the CEO is to be replaced. While unlikely, that could bring with it a major strategic shakeup at Big Blue, one that has potential to cause the company to reevaluate its dividend payout policy like it did in 1993. We'll continue monitoring these developments if and when they happen.

At the very least, a more leveraged IBM that fails to deliver on its stronger future growth will mean much slower dividend growth than what investors have seen in recent years. This might continue to put pressure on the stock, because a company with little to no growth potential could potentially trade at high yields north of 5% in today's market environment.

As we stated in our February 2018 thesis, "Conservative dividend investors may be better off sticking with other companies that have clearer paths to profitable long-term growth and operate in markets with a slower pace of change."