Whirlpool: Paying Uninterrupted Dividends Since 1955

Founded in 1911, Whirlpool (WHR) is the world's largest appliance manufacturer with over $20 billion in annual sales. The company makes and sells laundry appliances, refrigerators and freezers, cooking appliances, dishwashers, mixers, and other small home appliances under brands names like Whirlpool, KitchenAid, Maytag, and Jenn-Air.

Source: Whirlpool

Globally, Whirlpool's brands target an impressive 90% of the world's consumers, and the firm's sales are nicely diversified across its various product lines. Refrigerators & freezers account for 29% of sales, followed by laundry (28%), cooking appliances (19%), and other products (24%).

While Whirlpool markets its products in nearly every country throughout the world, approximately 49% of 2018 sales were derived from the U.S. Whirlpool operates via four business segments:

North America: 54% of 2018 sales

Europe, Middle East and Africa: 22% of sales

Latin America: 17% of sales

Asia: 7% of sales

Whirlpool has paid consistent annual dividends since 1955.

Business Analysis

Whirlpool has a rich history of product innovation over its 120-year history, having introduced one of the first electric washing machines in 1911, the first stand mixer in 1919, and the first countertop microwave in 1967.

In addition to its in-house product development work, Whirlpool's brand portfolio has expanded both organically, via new brand launches in foreign markets, as well as through periodic acquisitions, such as the purchase of KitchenAid in 1986 and MayTag in 2006.

As a result of the company's steady accumulation of popular brands, including sixwith over $1 billion in annual sales, Whirlpool holds No. 1 or No. 2 market share positions in each of its major geographic regions.

One of the keys to Whirlpool's success in achieving leading market share has been targeting every price point in the industry around the world:

Premium brands (15% of sales): KitchenAid, Jenn-Air

Mass market brands (75% of sales): Whirlpool, Maytag

Value brands (10% of sales): Indesit, Amana

In developed regions such as North America and Europe, which combine for more than 70% of Whirlpool's revenue, the home appliance market is mature since population growth rates are so low.

As a result, Whirlpool enjoys substantial replacement sales since many consumers often replace worn out appliances with the same brand in order to match the other appliances in their house. Therefore, as long as the company's product lineup remains competitive, Whirlpool's large installed base should remain a major cash cow.

Whirlpool invests $1 billion annually into capex and R&D to ensure its appliances stay aligned with evolving consumer preferences. A strong cadence of product innovation helps Whirlpool maintain its entrenched market position by pleasing customers and building brand loyalty for repeat purchases.

Long an industry leader in incorporating new technologies (touch screens, voice controls, etc) into its products, Whirlpool is now bringing to market some of the first home appliances connected to the internet and to each other.

Connected devices can be integrated with smart home systems like Amazon's Alexa and Google's Nest to offer consumers increased convenience and efficiencies while also creating potential for Whirlpool to sell high-margin bundled subscription services in the future.

In addition to its product innovation, Whirlpool also gains advantages from its leading global scale. This provides the company with relatively low costs to manufacture and distribute its appliances, an important advantage in the competitive and low-margin household appliances industry.

Going forward, Whirlpool's long-term growth strategy is to maintain leading market share in large and mature markets such as North America and Europe. Stronger growth will come from emerging markets where solid economic growth and a fast-growing middle class are driving higher demand for quality appliances.

Altogether, management expects that its investments, along with Whirlpool's strong economies of scale, will allow the business to achieve modest organic sales growth of about 3% annually and margin expansion in the coming years.

Over the long term, it's hard to imagine this mature, cyclical industry's growth exceeding a low single-digit rate. After all, demand for household appliances is largely tied to the economy, housing market, and overall population growth. Already the giant in the industry, Whirlpool seems unlikely to grow at a much faster pace.

Should the company hit its financial targets while continuing to buy back stock, Whirlpool has potential to generate high single-digit EPS growth. The firm's payout ratio sits at management's target (30%), so in this scenario future dividend growth would likely hover in the mid- to upper single-digit range as well.

However, while Whirlpool is an industry leader, there are plenty of risks that income investors need to be aware of before investing.

Key Risks

Whirlpool sells durable goods which are cyclical and tied to the health of the U.S. and global economies. For example, during the Great Recession, Whirlpool's sales fell 13%. While that's not terrible, the firm's earnings fell more than 40% due to the high fixed costs required to manufacture appliances.

This sensitivity to the economy explains why management targets such a low EPS payout ratio (30%) for its dividend and also why the company has gone many years between dividend increases in the past.

In other words, while Whirlpool's dividend appears to be safe due to management's financial conservatism, investors can't expect clockwork-like annual payout increases from the company.

More importantly, while Whirlpool undoubtedly has several competitive advantages and has been conservatively managed to ensure it has staying power for the long term, the business gives us a "best house in a bad neighborhood" feeling.

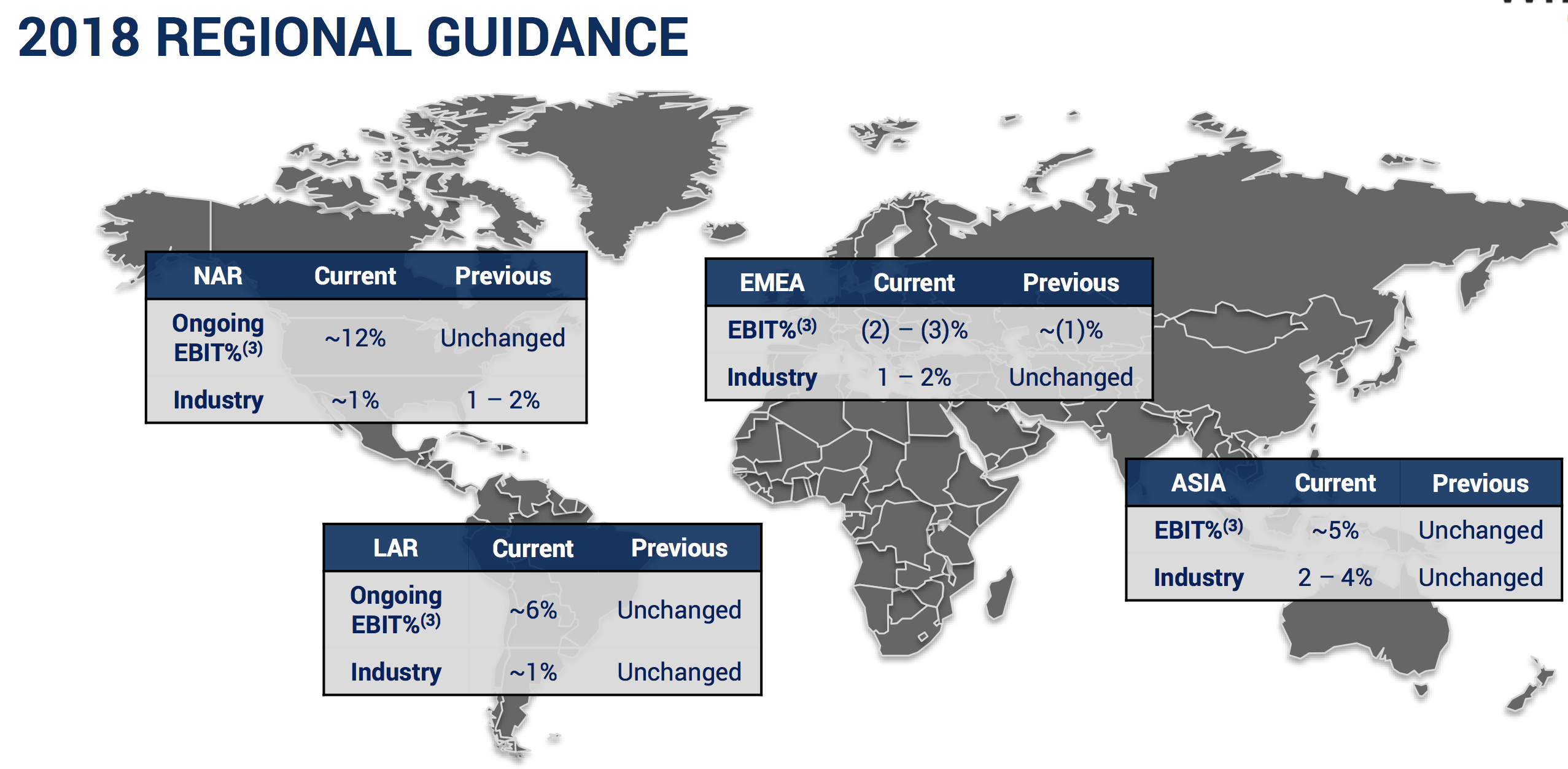

The household appliance industry's operating margins around the globe are rather abysmal, averaging near 1%. With the exception of Europe, the Middle East, and Africa, the company's profitability around the world is much better than the industry average.

Source: Whirlpool Investor Presentation

At the same time, Whirlpool is far from immune to the perpetual challenges the industry faces, including volatile raw material and freight costs, capital-intensive manufacturing processes, price-sensitive consumers, and cyclical demand trends.

Consumers are becoming more informed shoppers as well. Ten years ago, newspaper ads were the No. 1 source for consumers when they looked for information about an appliance to buy, according to management. Today, it's almost all digital as consumers research competing appliance brands online before making a purchase.

In other words, Whirlpool must continue differentiating its products with the right investments in innovation and distribution (e.g. e-commerce) if it wants to maintain its leading market share positions and above-average profitability.

Whirlpool's financial results in any given quarter or year are also exposed to currency risk due to the firm's global presence (51% of sales are from outside the U.S.). If the U.S. dollar appreciates against local currencies, then the company's products become more expensive and less competitive in foreign markets, where the firm doesn't have a local manufacturing presence.

In addition, foreign sales translate into less revenue and earnings in U.S. dollars when Whirlpool reports results. While currency fluctuations tend to be mean reverting (cancel out over time), in the short to medium term they can create growth headwinds that might cause Whirlpool to miss its financial targets. That in turn could result in slower or even no dividend growth over several years.

Overall, though, we expect Whirlpool's long-term earnings power to be influenced primarily by the industry's mature and cyclical nature and not by short-term headwinds like exchange rate fluctuations or even trade conflicts.

Closing Thoughts on Whirlpool

Whirlpool is a time-tested household name, thanks to over a century of product innovation and its strong portfolio of appliance brands all over the world. The company has an impressive track record of maintaining its dividend during industry downturns, and raising its payout steadily during good times.

Over the long term Whirlpool's capital allocation strategy of investing about 6% of sales into expanding and improving its manufacturing, along with developing new products, should serve it well by keeping its operations lean and its customers loyal to its brand. Targeting long-term profitable growth in emerging markets will help, too.

However, while Whirlpool's generous dividend appears safe, investors need to remember the business operates in a highly competitive and cyclical industry. At the end of the day, it's harder to get excited about the company as a long-term investment given the challenging nature of the home appliances space.