The Strengths and Weaknesses of Physicians Realty's Dividend

Founded in 2011, Physicians Realty (DOC) is a new entrant in the healthcare real estate space that sports a high 5% dividend yield. Attractive at first glance but without much of a track record, just how safe is this REIT's dividend?

The good news is that Physicians Realty appears to have a stable source of rent income to pay its generous dividend.

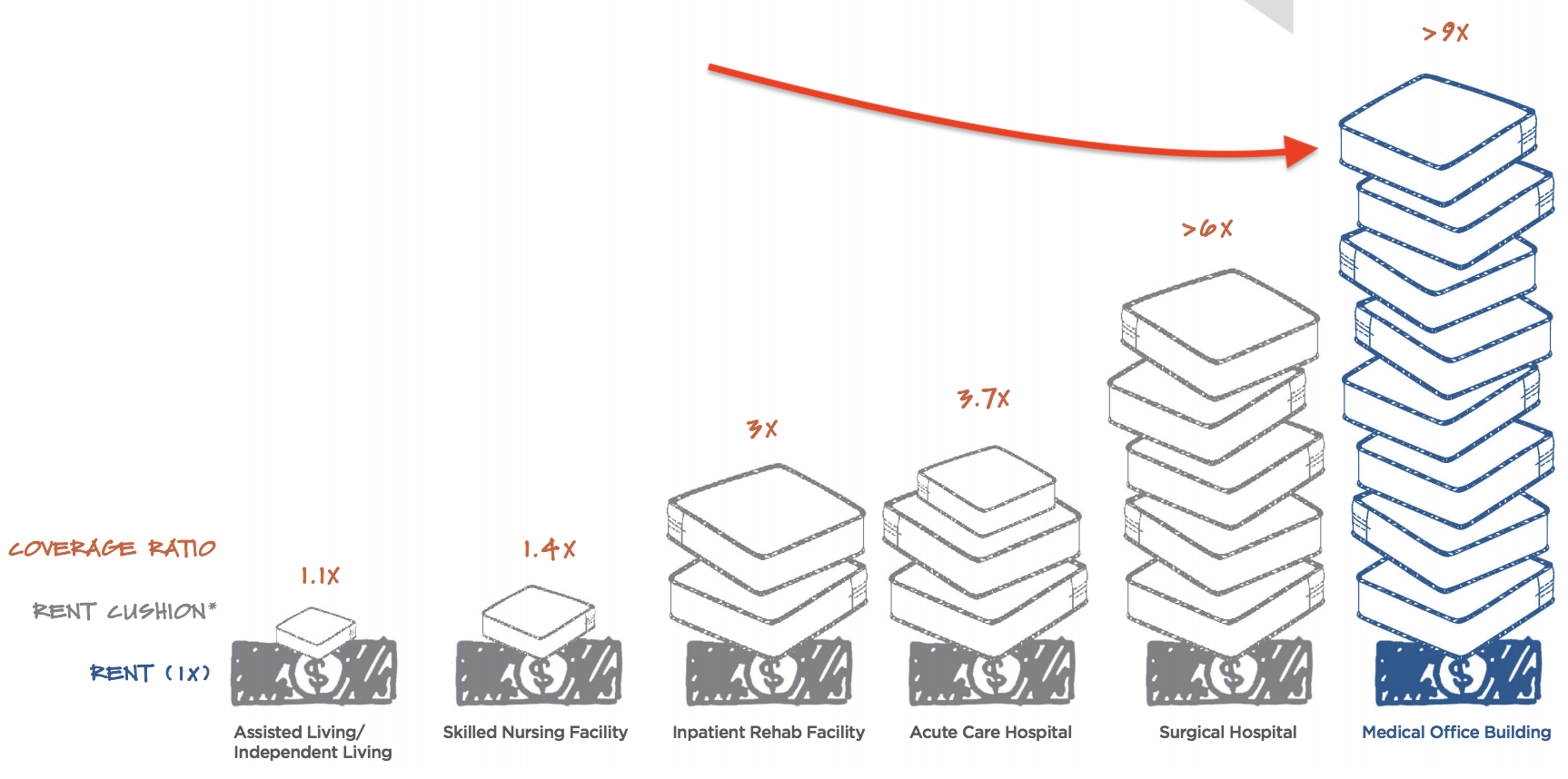

Physicians Realty's occupancy rate is a healthy 97%. The company acquires medical office buildings (MBOs) that are located on medical campuses or otherwise affiliated with a hospital. This is prime real estate for medical practices, suggesting the company won't have difficulty finding tenants in the future.

Furthermore, due to less government regulation and better reimbursement from insurers, practices within MBOs are generally more profitable than those at traditional hospitals. Tenants of MBOs are typically better able to cover their rent than tenants of other healthcare property types.

Source: Healthcare Realty Investor Presentation

Tenants also sign long-term, 5 to 15-year leases that bake in annual rent increases of 2% to 3%. Better yet, 92% of leases are absolute or triple net, which puts tenants on the hook for most operating expenses (e.g. maintenance and utilities) and creates greater certainty of future cash flow.

Buoyed by an aging population that's likely to spur healthcare spending for decades to come, Physicians Realty appears to have a dependable source of rent income for the foreseeable future.

The less encouraging news? Management's aggressive approach to growth in the business' early years weighs on the safety of Physicians Realty's dividend.

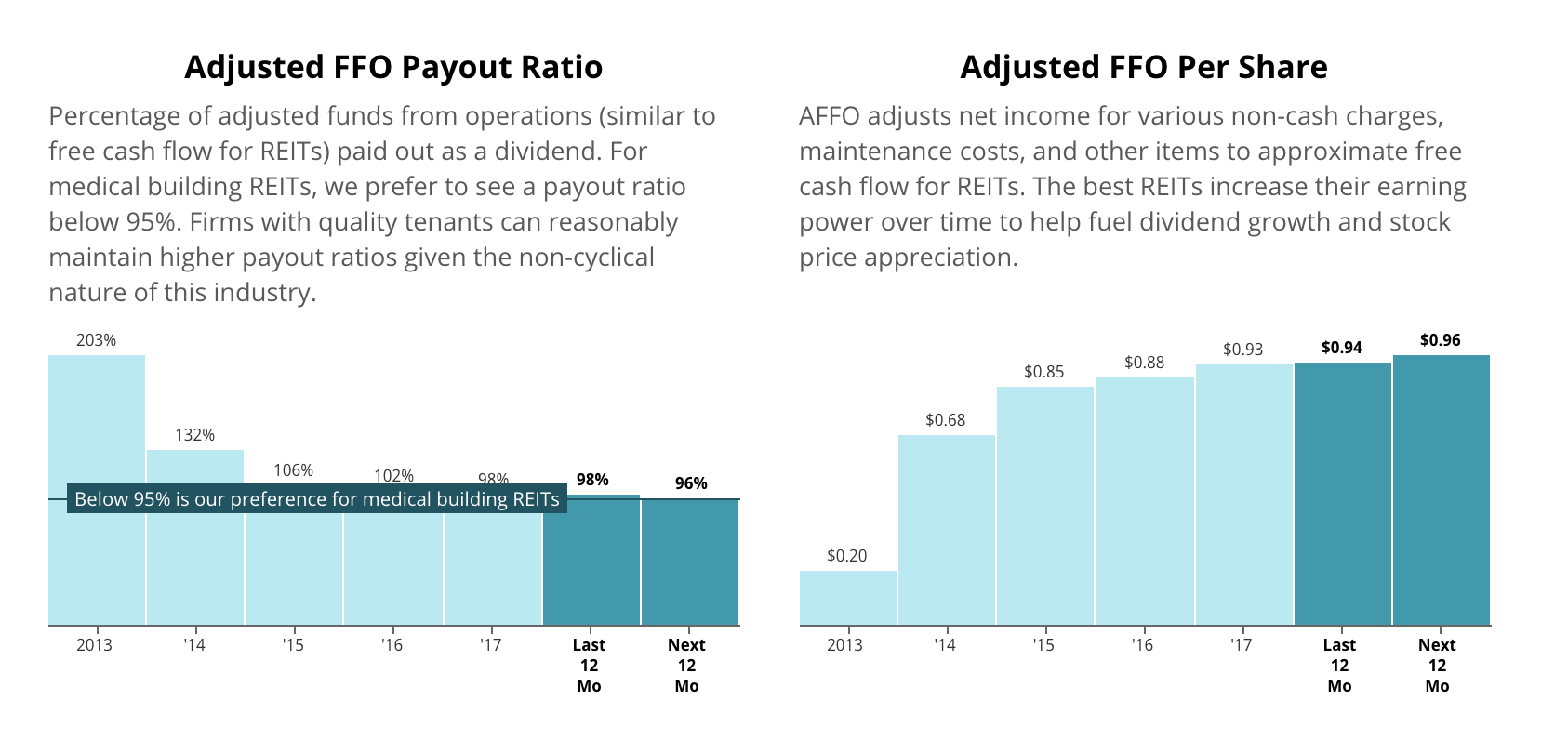

The firm's AFFO (adjusted funds from operations) payout ratio currently sits at 98% and has been above 100% for most of its history. Possibly in an effort to attract investors, management has chosen to retain little to no cash flow, instead relying entirely on issuing debt and equity (i.e. new shares) to fund growth.

Source: Simply Safe Dividends

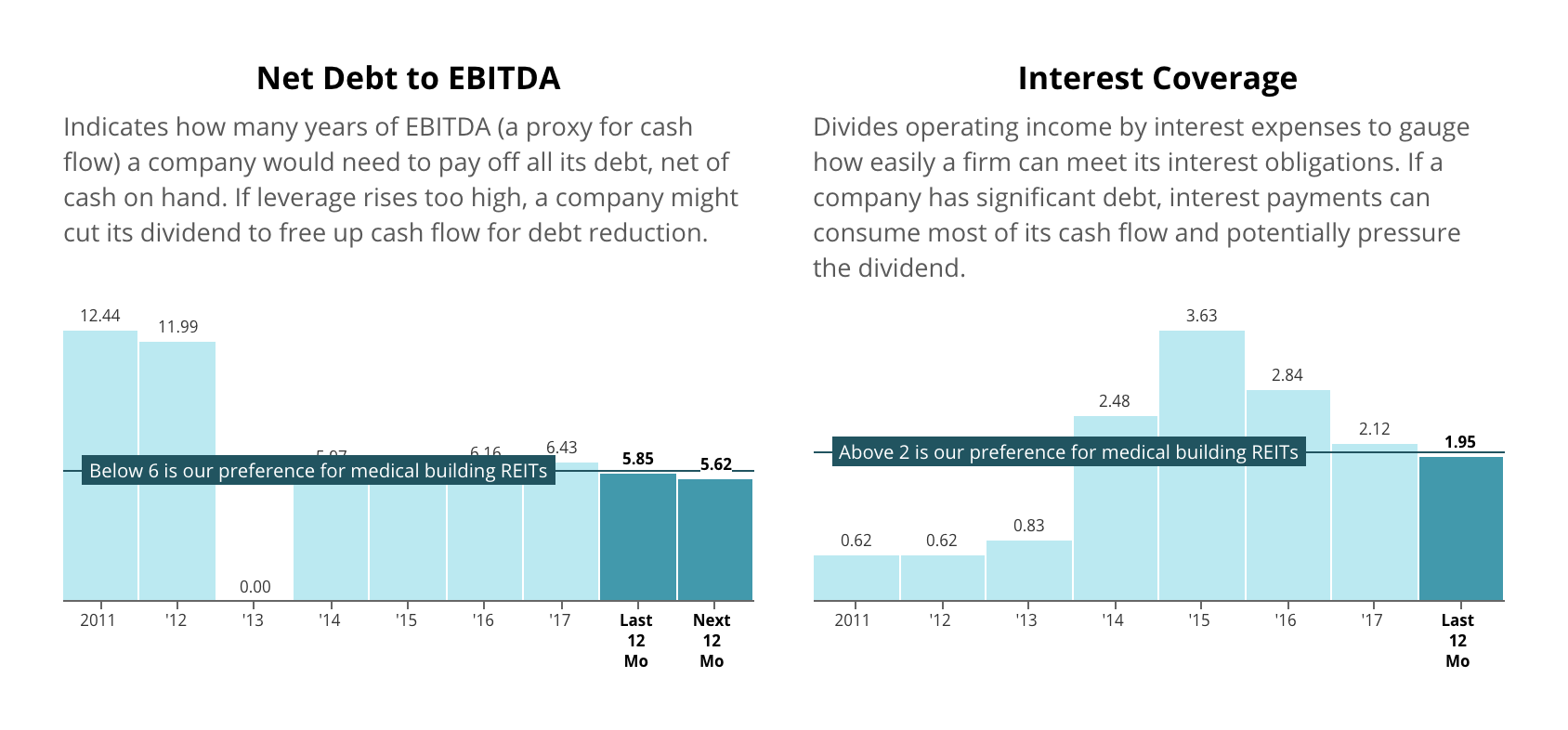

As a result of the company's reliance on debt to quickly grow its portfolio of properties and diversify across tenants and geography, both the firm's net debt to EBITDA and interest coverage ratios are pushing the limits of what we like to see.

Source: Simply Safe Dividends

Physicians Realty's mediocre debt metrics, short operating history, and relatively small size has led to a precarious BBB- credit rating from Standard & Poor's, just one rung above non-investment (i.e. junk) grade.

Maintaining and improving upon this credit rating is critical to management's plan to affordably fund growth opportunities.

Since the company pays out almost all of its cash flow as a dividend, if business take an unexpected turn for the worse and capital markets tighten, management could be forced to cut the dividend to accumulate cash and protect the firm's credit metrics.

Sure, Physicians Realty's rental income looks stable today, but there are still scenarios that could jeopardize the dividend.

The REIT has been in business for just seven years, so it's hard to know how committed to the dividend management would be during a downturn. (Over a third of REITs reduced their dividends during the financial crisis.)

If, for example, credit markets were to freeze up as they did during the financial crisis, management could find itself unable to refinance or otherwise pay back a large chunk of debt due to mature soon.

Since the dividend is ultimately a discretionary payment, it could be an easy decision for management to cut the dividend in order to shore up the company's liquidity and pay back debt until capital market conditions improve.

As things stand right now, the company's borderline credit rating gives management incentive to prioritize the balance sheet over the dividend. The good news is Physicians Realty has relatively little debt maturing over the next few years, reducing some of this risk over the short to the medium term.

Physicians Realty's relatively small size (just $4.4 billion in assets) is mostly a disadvantage to the dividend as well. Compared to larger REITs, the firm has fewer properties to sell to raise cash or opportunistically recycle capital, less revenue to cover fixed operating costs, generally more difficult access to capital when conditions tighten, and a more concentrated tenant base.

In fact, 18.7% of Physician Realty's rent is from hospitals affiliated with Catholic Health Initiatives (CHI). Fortunately, CHI has a strong investment credit rating (Baa1) from Moody's, and each affiliate is responsible for its own rent payments, so the risk to Physician Realty's rental income appears minimal.

Another risk to the dividend is Physicians Realty's concentration in a single property type whose tenants' financial health is subject to uncertain government regulations. MBOs look like a good bet today, but it's difficult to predict winners and losers in the healthcare industry far into the future.

While none of these risks appear to be imminent threats, especially given the non-cyclical nature of this industry and tenants' healthy rent coverage, Physicians Realty's high payout ratio, less-than-stellar debt metrics, and history of aggressive growth leave less room for safety.

Our Dividend Safety Scores gauge risk over a full economic cycle, and our preference as long-term investors would be to concentrate our portfolio in safer alternatives, at least until Physicians Realty improves its payout ratio to a more conservative level.