Federal Realty Investment Trust: A Dividend King REIT

Founded in 1962, Federal Realty Investment Trust (FRT) is one of the oldest REITs in the world. The company specializes in high-quality, neighborhood shopping centers that are anchored by grocery stores and located in large, affluent markets such as Silicon Valley and New York.

Source: Federal Realty Investment Trust

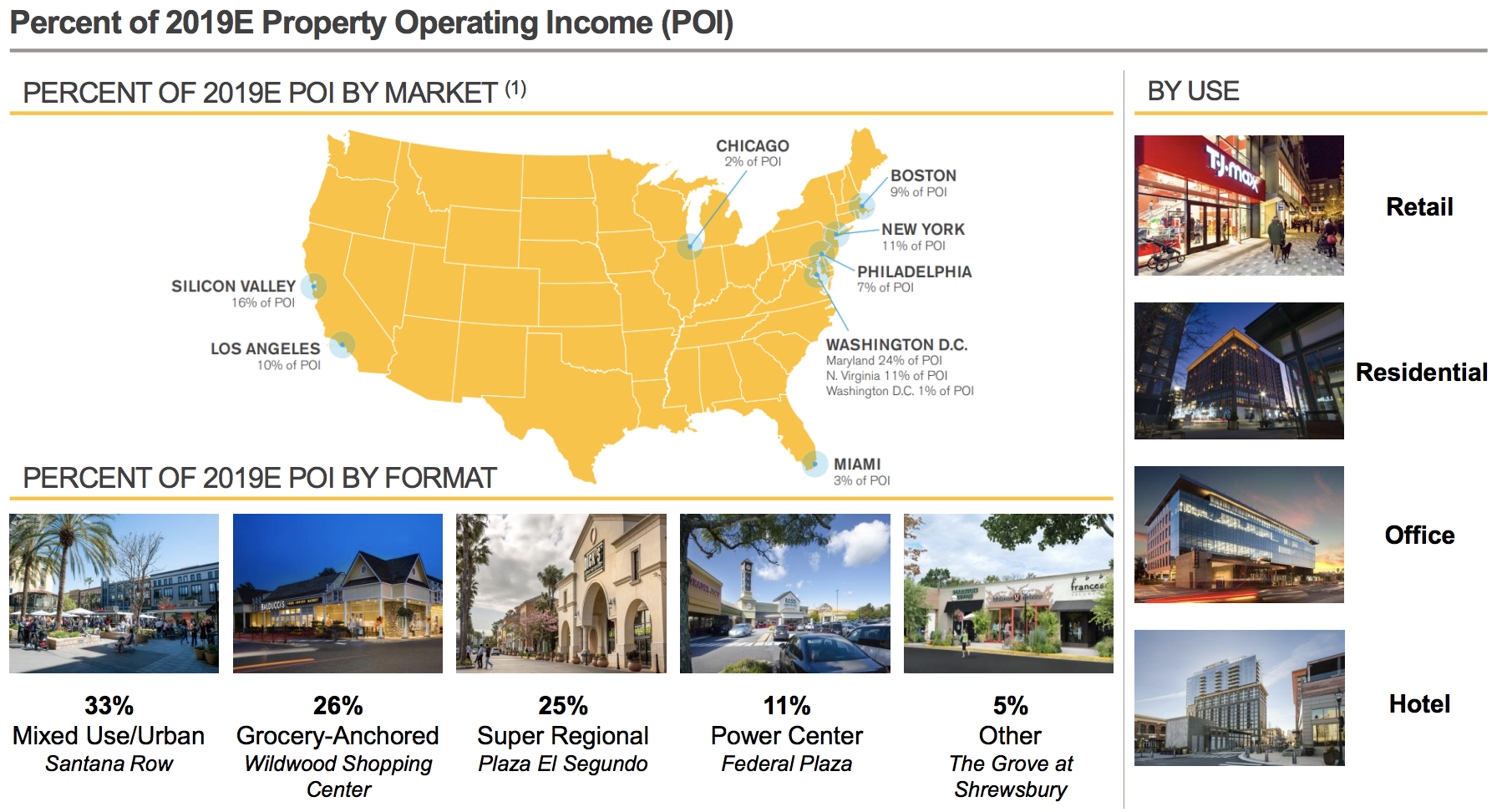

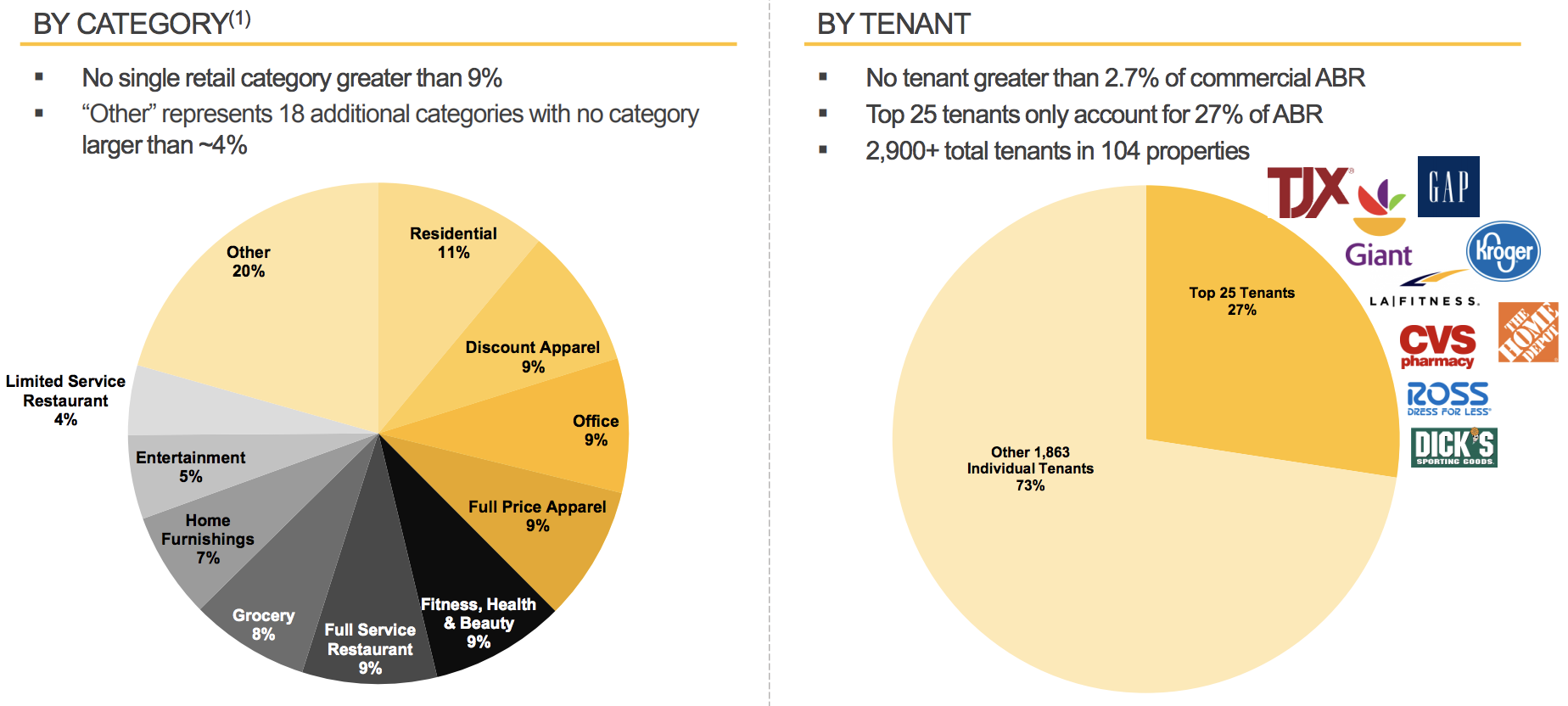

Today the REIT owns 104 properties, comprising 24 million square feet of leasable area which is under long-term leases to over 2,900 tenants in numerous subcategories. As you can see, Federal Realty's cash flow is highly diversified. No single retail category exceeds 10% of the REIT's operating income, and no tenant is greater than 3% of rent.

Source: Federal Realty Investor Presentation

About 65% of the firm's rent is from tenants who operate in relatively e-commerce resistant industries like grocery stores, restaurants, fitness centers, health and drug stores, autos, and entertainment.

Over the past 20 years, Federal Realty has been investing more into non-retail properties such as offices, hotels, and apartments. Most of these properties are close by or directly connected to its shopping centers creating mixed-used centers that are more valuable to tenants due to higher foot traffic.

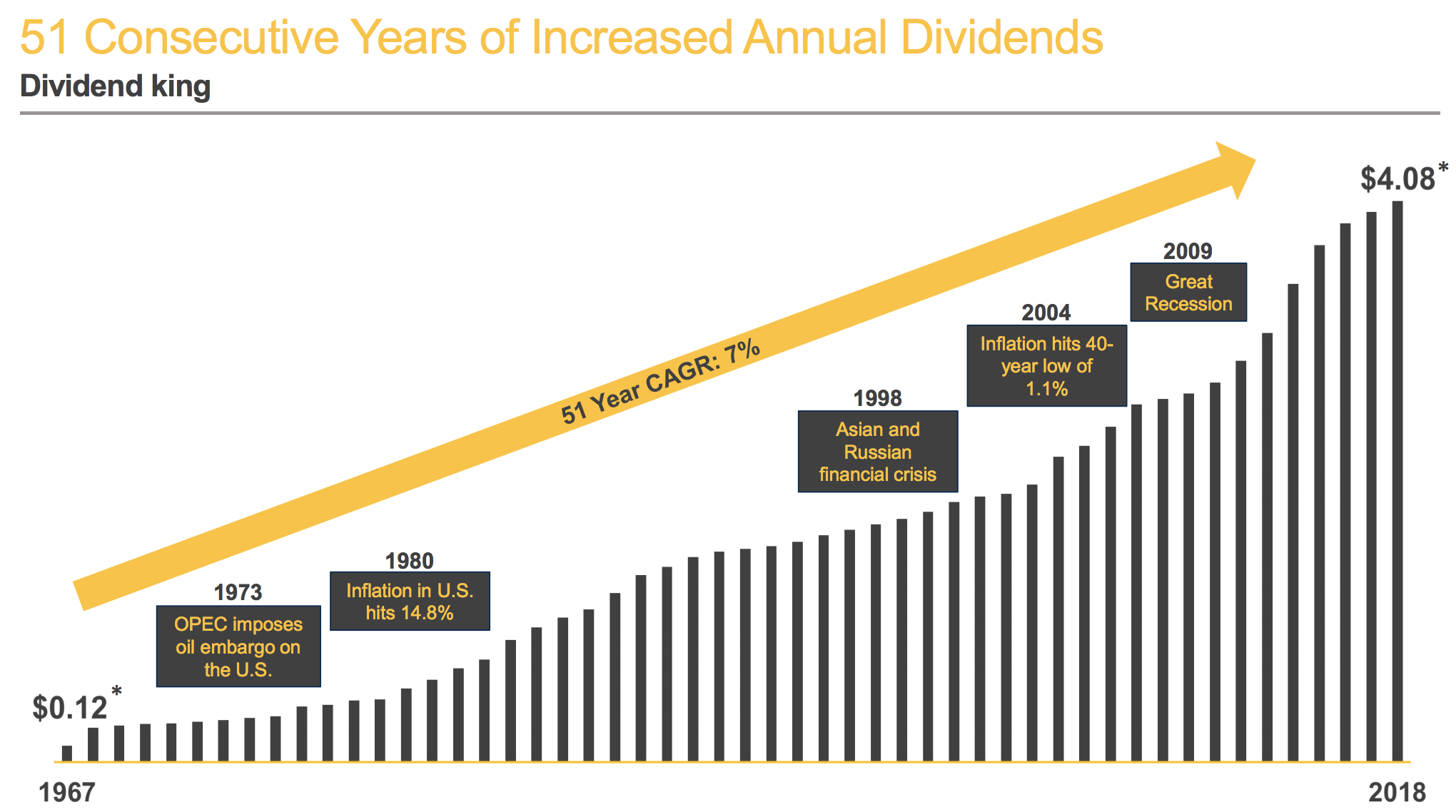

Federal Realty has raised its dividend for 51 consecutive years (the longest dividend growth record of any REIT), making it the sector's only dividend king.

Business Analysis

Federal Realty Investment Trust has several advantages that make it arguably the highest-quality shopping center REIT and one of the best-managed companies in the world.

First, management emphasizes quality over quantity. For example, Federal Realty focuses almost exclusively on owning premium shopping centers, mostly anchored by grocery stores which drive consistent foot traffic.

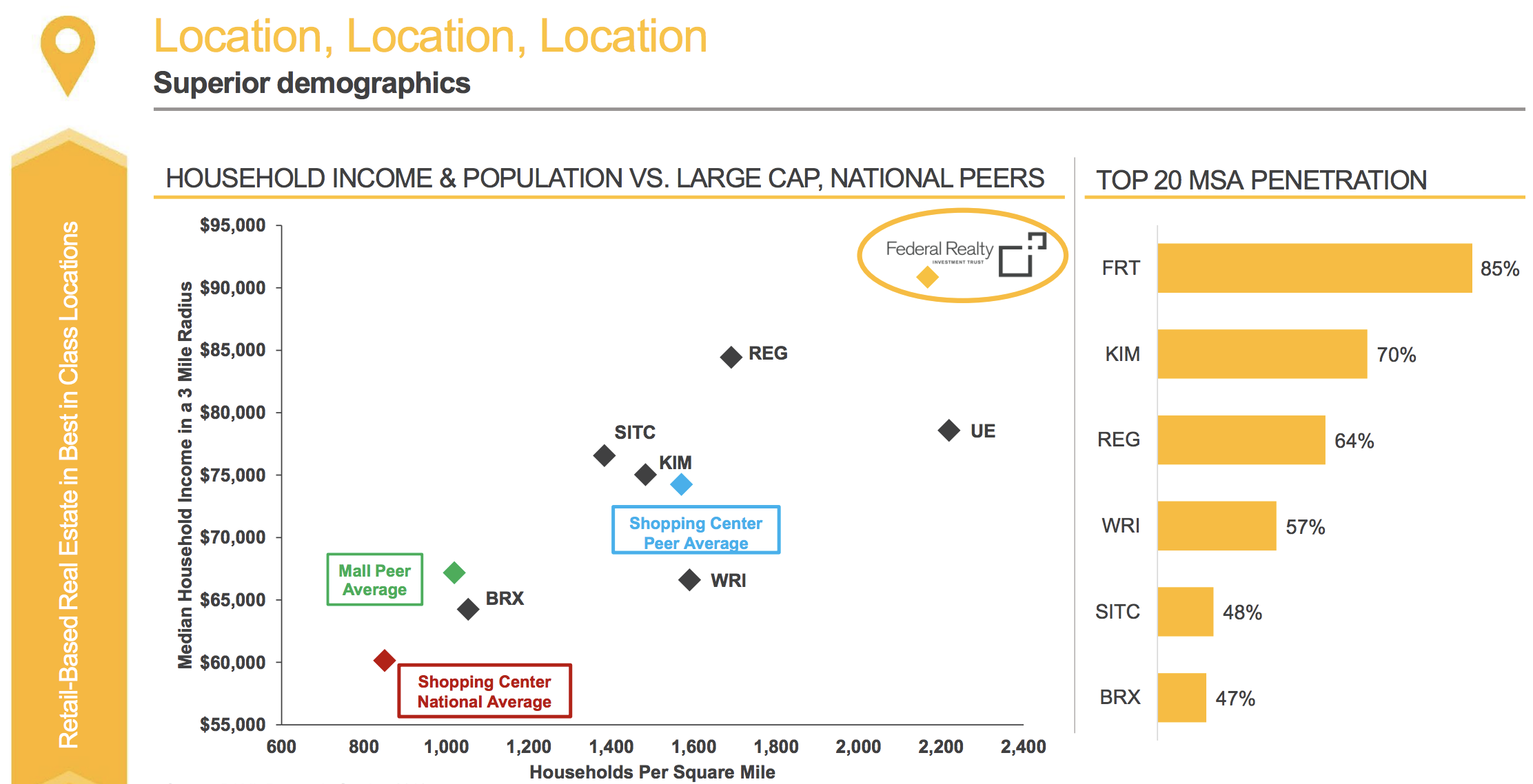

To help ensure the success of its tenants, who operate under triple net leases (they pay all maintenance, taxes, and insurance costs), the REIT focuses on acquiring and developing centers in the highest density and wealthiest areas within its core markets. In fact, 85% of the company's centers are located within the country's 20 largest and most affluent cities.

As you can see below, Federal Realty's average center is located in areas with three times the average population density and over 50% higher median household income, compared to the average shopping center REIT.

Source: Federal Realty Investor Presentation

Thisstrongfocus on top tier centers, with strong tenants, has allowed the REIT to generate average rent per square foot that's more than 50% higher than its peer group average.

Even better, Federal Realty's superior locations mean that not only does it enjoy industry-leading rents, but the company has been able to steadily increase its rental rates at relatively fast rates.

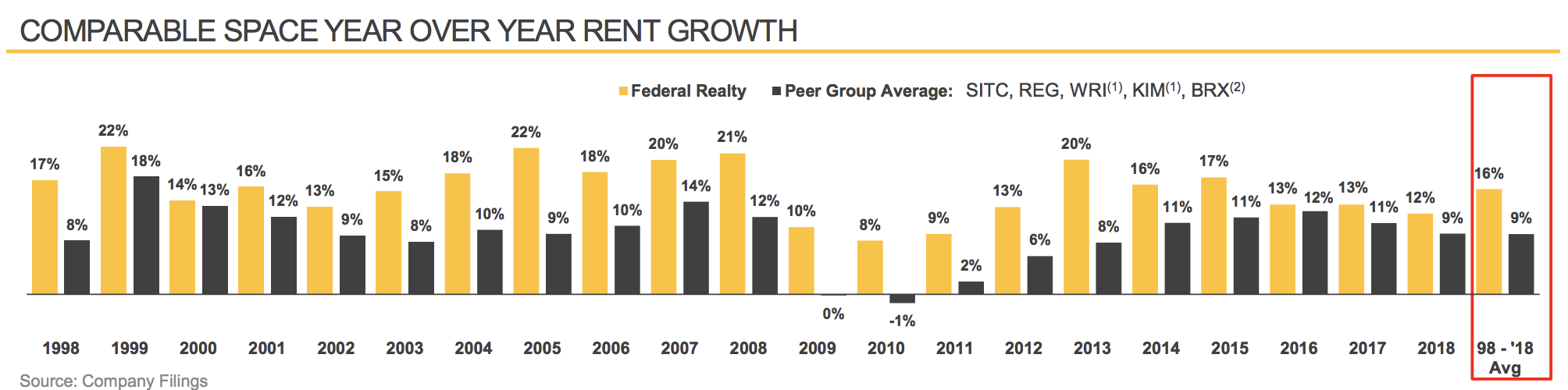

You can see this in the REIT's lease spreads, which measure how much average rent increases when a new lease is signed. This occurs when a tenant either leaves early (due to store closure) or signs a new lease once the old one expires.

Since 1998, Federal Realty's lease spread has averaged 16% (peers averaged 9%) and never declined, even during the financial crisis when its rivals recorded negative spreads.

Source: Federal Realty Investor Presentation

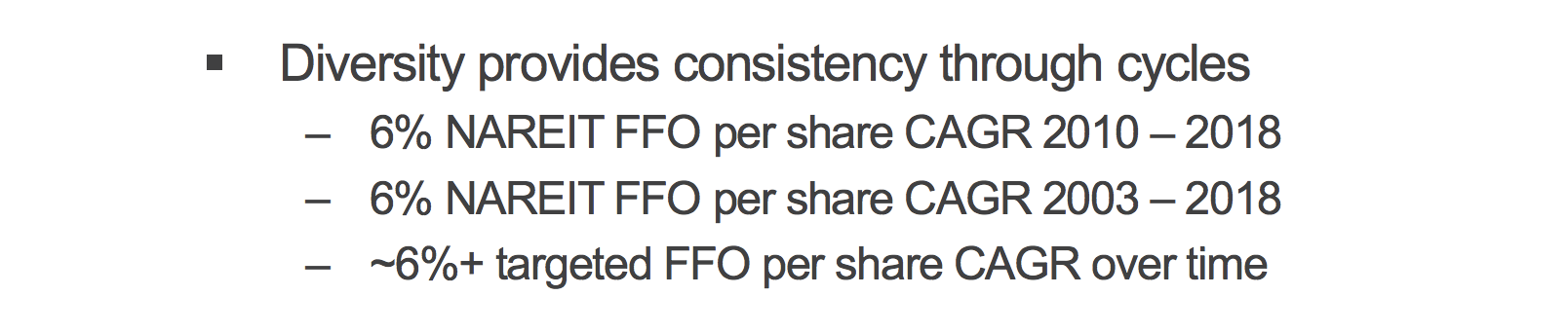

Federal Realty continues enjoying double-digit lease spreads today as well (12% in 2018). In other words, despite the shifting retail environment, the firm's tenants appear to be doing well enough to be able to afford much higher rents. Thanks to its strong pricing power, Federal Realty has historically achieved industry-leading growth in funds from operations, or FFO, as well.

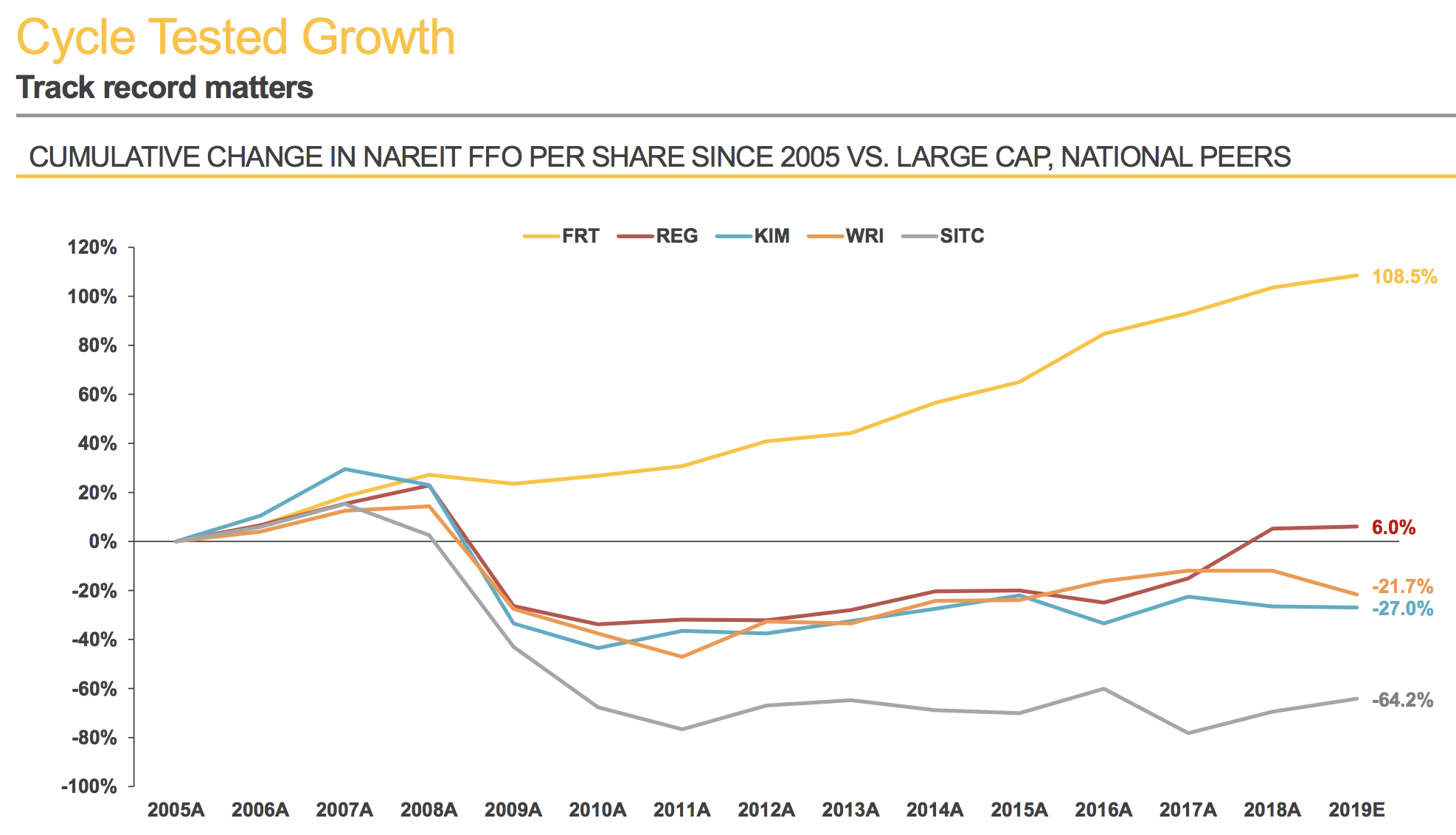

In fact, Federal Realty and Simon Property Group (SPG) are just two out of 24 retail REITs that have been able to deliver FFO per share growth every year since 2010. This highlights the power of quality retail REITs, run by two of the best management teams in the industry. Federal Realty's consistent cash flow growth is especially impressive when compared to the FFO per share growth of its peers since 2005.

Source: Federal Realty Investor Presentation

The firm's consistent growth has allowed Federal Realty to generate the industry's safest and fastest-growing dividend over the past decade. More impressively, Federal Realty also happens to have the single best dividend growth track record of any REIT, with a remarkable 51 straight years of annual dividend increases.

Source: Federal Realty Investor Presentation

Going forward, the company has two main strategies for growth. First, it plans to opportunistically acquire new shopping centers that fit into its high-density and high-affluence market strategy.

However, Federal Realty plans to achieve most of its long-term growth through aggressive but disciplined redevelopment projects. That means building hotels, offices, and apartments connected to or very near its existing properties.

In fact, today Federal Realty owns nearly 2,700 apartment units which have a strong occupancy rate of 97% and steadily rising rents (due to the tight housing markets in their locations).

There are three reasons why Federal Realty is focusing so much on non-retail developments.

First, by turning its existing centers into mixed-use properties, Federal Realty's retail locations become even more valuable to tenants. This is because offices, hotels, and apartments attract additional traffic to its shopping centers, increasing the value of its locations to retailers and supporting higher rents on its new leases.

Second, the cash yield on investment is actually higher than its core shopping center portfolio. For example, historically Federal Realty has achieved close to 6% cash yields on acquiring or building new shopping centers.

However, the company has been getting 6% to 12% cash yields on its non-retail developments, which combined with its low cost of capital means that each new investment is even more profitable and accretive to cash flow per share.

Finally, by targeting non-retail investment opportunities, Federal Realty has a far longer growth runway. In fact, management estimates that its mixed-use pipeline has more than $3.5 billion of development potential over the next 15 years. That's on top of the $1.1 billion development pipeline the REIT is currently working on.

The REIT has already obtained the land for its large shadow development pipeline of mixed-use developments. For perspective, Federal Realty's shadow backlog potentially includes increasing its residential apartment unit count by 60% and more than doubling its overall non-retail square footage.

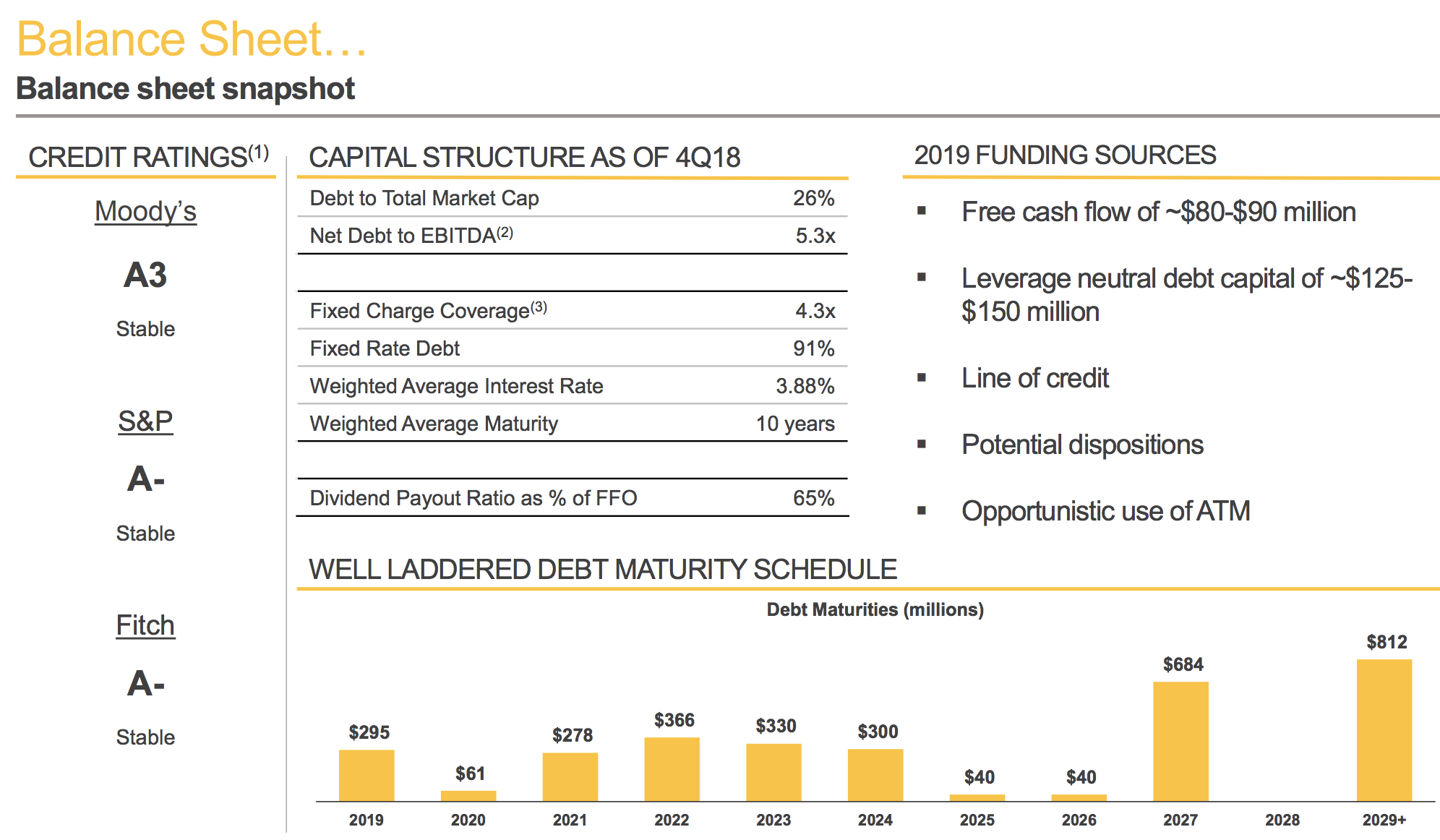

The firm's final competitive advantage is its access to low-cost capital to execute on its growth plans with less funding risk. Compared to many of its peers, Federal Realty maintains a relatively lower payout ratio (65% of FFO), which results in higher amounts of retained cash flow that can be reinvested. For context, the average REIT and shipping center REIT has an FFO payout ratio near 80% and 95%, respectively.

Also important is the strength of the balance sheet. Thanks to its very conservative approach to debt, Federal Realty has one of the sector's only "A" credit ratings (A-). Only five other REITs have an "A" rating from both S&P and Moody's, helping these firms borrow at low rates and earn a profitable spread with the investments they make.

Source: Federal Realty Investor Presentation

Besides enjoying access to low-cost debt, Federal Realty also enjoys a low cost of equity thanks to the premium its shares typically trade for. For example, Federal Realty shares currently trade at a forward price-to-AFFO multiple of 24.2, above the Real Estate sector average of 16.7. In other words, the company can sell new shares to investors at a high enough price to ensure that its cash flow per share rises with each new investment.

Thanks to these advantages, Management expects Federal Realty's FFO per share to grow around 6% annually over time, which is a good proxy for the company's future dividend growth as well.

A mid-single-digit growth rate is consistent with the REIT's long-term results, indicating that Federal Realty's business model is very stable and management is confident income investors will enjoy the same level of growth as in the past.

Source: Federal Realty Investor Presentation

All told, Federal Realty's combination of premium locations, investments into non-retail properties that enhance its store property values (and pricing power), low cost of capital, and lengthy dividend growth track record mean that this REIT appears to have strong competitive advantages to help it continue creating value for shareholders in the years ahead.

However, despite Federal Realty's impressive track record of adapting to evolving and challenging industry conditions, there are still certain risks that investors need to be aware of.

Key Risks

While Federal Realty's tenant base is highly diversified (no tenant represents more than 3% of total rent), it still does business with numerous struggling retailers such as The Gap (GPS), Ascena Retail Group (ASNA), and Splunk, which collectively account for close to 4% of total rent.

In total, about 35% of the REIT's rent comes from tenants in potentially e-commerce sensitive industries such as apparel and electronics.

Pressure from online sales is likely to continue rising for the foreseeable future, given that e-commerce has steadily gained market share over time and is expected by most analysts to keep growing at a double-digit rate.

And while the majority of Federal Realty's rent is from e-commerce resistant industries like grocery stores and restaurants, online disruptors such as Amazon (AMZN) are constantly trying to break into new markets (including grocery). This means that Federal Realty's tenants might eventually face increasing financial pressure as the world of retail continues evolving.

While Federal Realty's locations are in highly affluent and high-traffic areas, the brands of some of its retail tenants have begun to fall out of fashion due to consumers' fickle tastes and shifting shopping habits.

In other words, for some of Federal Realty's tenants, the issue isn't "location, location, location" but rather "you are selling the wrong products and brands." Those stores may end up struggling and either the tenants won't be able to afford to remain in their current locations or the head office may end up shutting them down if sales disappoint badly enough.

In some of those cases, the company could also have to invest more time and money into redeveloping certain locations before it can find a replacement tenant.

The good news is that Federal Realty's prime locations have proven to be highly in demand as seen by its continuing strong lease spreads. Even if some of its tenants fail, the REIT should be able to eventually replace empty locations with stronger and thriving retailers, and likely at much higher rents.

However, this turbulence may still result in short-term declines in cash flow growth that could disrupt management's long-term mid-single-digit growth target. For example, after a strong year of growth in 2018 (8.5% cash flow per share) management is guiding for just 2.4% growth in 2019. The stock's premium valuation multiple could contract if investors adjust their long-term growth expectations lower.

Another risk to keep in mind stems from management's increasing focus on non-retail redevelopment projects. While these are generally more profitable (higher cash yields on invested capital) properties than its bread-and-butter shopping centers, they can serve as a double-edged sword for two reasons.

First, office, hotel, and apartment development is very different than shopping centers, requiring specialized expertise. While Federal Realty has been finding success with mixed-use over the past 20 years, it still has far more experience with its core retail operations.

This is one reason why Federal Realty has partnered with numerous local office, hotel, and apartment developers via joint ventures to help not only develop its non-retail properties but also help to fund them.

However, this brings up a second risk to Federal Realty's long-term growth prospects. Specifically, the REIT isn't large enough to have the kind of liquidity to fully go it alone on its $3.5 billion potential development pipeline.

In other words, in the future, it's possible that some of the REIT's development partners might end up running into financial difficulties. This could result in project delays or cancellations. In addition, because real estate development is a complex endeavor, there is always the risk that Federal Realty won't be able to finish its projects on time or on budget.

As a result, its cash yields on investment could fall short of projections, resulting in growth coming in below expectations. However, it should be noted that as Federal Realty grows and management gains experience in non-retail development and achieves larger scale, these risks should decrease over time.

It should also be noted that the board of directors includes the CEOs of several other REITs and real estate development companies with experience in non-retail development operations. This minimizes the chances that Federal Realty is stepping outside its circle of competence with its mixed-use strategy.

Closing Thoughts on Federal Realty Investment Trust

Parts of the retail industry are undergoing disruption right now, thanks largely to e-commerce and fickle consumer tastes and shopping habits. However, as with all industries, there are high-quality companies in this space that have proven to be quite adaptable over time.

These businesses tend to be leaders in their industries and have time-tested management teams, strong balance sheets, unique competitive advantages, and numerous opportunities for long-term growth.

As the only dividend king in the real estate sector, Federal Realty has proven to have all of these qualities. Conservative dividend growth investors interested in a shopping center REIT that appears to be durable and capable of paying higher dividends for the foreseeable future should give Federal Realty a closer look.