Colgate-Palmolive: Uninterrupted Dividends for Over 120 Years

Founded in 1806 by William Colgate as a starch, soap, and candle business, Colgate-Palmolive (CL) has grown into one of the world’s largest consumer products conglomerates today.

The company’s 34,500 global employees sell its world-famous brands (such as Colgate, Palmolive, Protex, Speed Stick, Ajax, Irish Spring, Sanex, Hill’s, and Softsoap) in more than 200 countries through four business segments:

Oral Care (47% of sales): toothpaste, mouthwash, toothbrushes.

Personal Care (20%): shower gel, body lotion, liquid hand soap, bar soaps.

Home Care (18%): household cleaners, liquid fabric conditioners, hand dishwashing soap.

Pet Nutrition (15%): specialty pet food.

Source; Colgate Investor Presentation

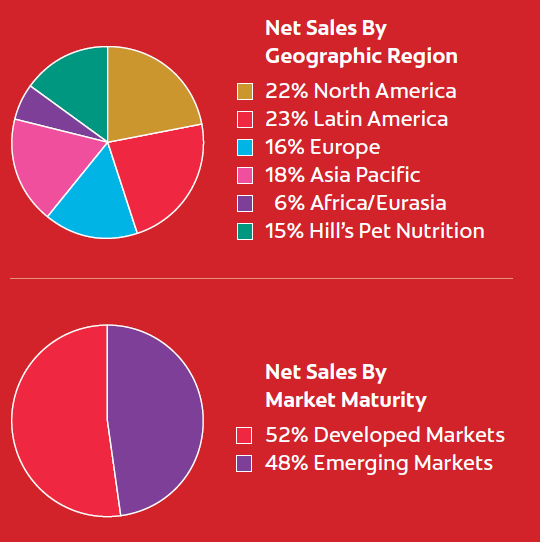

In addition to a broad portfolio of well-known brands, Colgate’s business is highly diversified by geography (70% of sales outside of the U.S. including Hill's Pet Nutrition), including a strong presence in faster-growing emerging markets. In fact, the company's business is split 50/50 between developed markets and emerging markets.

Source: Colgate Annual report

Colgate has been in most of these developing nations for decades, meaning that its brands are very well known and trusted. Colgate should benefit as rising living standards in emerging markets increase demand for its toothpastes, soaps, lotions, and pet foods. As one of the most internationally diversified consumer staples giants, Colgate is a potentially an attractive option for investors seeking lower-risk exposure to countries like China, India, and Latin America.

Colgate's distribution is also nicely diversified with Walmart (WMT) being its largest customer, representing 11% of total revenue. All other wholesale retail partners are under 10% of sales, helping to reduce the risk of customers squeezing Colgate on price.

Colgate has raised its dividend for 56 consecutive years, making it a dividend king. The company has paid an uninterrupted dividend for 123 consecutive years.

Business Analysis Colgate has been in business for a long time (more than 210 years). In fact, the company’s first toothpaste was introduced in jars during the early 1870s and moved into a collapsible tube in 1896.

Not surprisingly, one of Colgate's competitive advantages is the cumulative knowledge base it has built up over the company’s lifetime. Over two centuries' worth of R&D, marketing expertise, consumer insights, branding, and distribution relationships have been accumulated and strengthened over the years.

Perhaps equally important, Colgate has been in key emerging markets for a very long time as well. For example, the company entered Mexico in 1925, Brazil in 1927, and India in 1937.

Source: Colgate Investor Presentation

This long-lasting presence has certainly helped Colgate understand these consumers on a deep level, adapting its brands and products to meet their needs very well over time.

As a result, Colgate enjoys leading market share positions in many key categories in these faster-growing regions. For example, Colgate's toothpaste market share exceeds 80% in Mexico, 70% in Brazil, 50% in India, and 30% in China.

The company has meaningfully grown its share of each of those markets over the past 20 years as well, and in 2018 it commanded No. 1 market share in global toothpaste (42%) and 32% share for manual toothbrushes thanks to selling its core product in 78 countries.

Shelf space is another major advantage that incumbents tend to enjoy in the consumer staples sector. Retail customers want products that they know will sell and be invested in by the manufacturer in the form of expensive in-store displays, attractive product packaging, and marketing campaigns. Taking a risk on new products from much smaller companies doesn't often provide much upside.

Colgate invests heavily to stay ahead of trends in its markets, which are slow-changing, to begin with. The company typically spends about 2% of sales on R&D and 10% on marketing, or a combined $1.8 billion per year, introducing new products and maintaining its brand power. In 2017 Colgate's 12 global R&D facilities were granted 1,780 patents on new products, about four times more than its nearest competitor.

These investments ensure that the company’s products continue to meet evolving consumer needs and remain in the forefront of their minds as they shop.

Altogether, Colgate's longevity, effective R&D and marketing investments, and high-quality management have allowed the company to dominate most of the markets it competes in.

Colgate is No. 1 in toothpaste (42% global market share; approximately 3x greater than its next biggest competitor and up from 35% in 1995); No. 2 in mouthwash; No. 1 in manual toothbrushes; No. 1 in liquid hand soap; No. 2 in liquid fabric conditioners; No. 2 in bar soaps and liquid body cleaning; No. 2 in hand dishwashing and household cleaners; and No. 1 in pet food sold through vet clinics.

The company’s quality reputation, well-known brands, and strong mindshare with consumers have helped it grow sales and profits through price increases. In fact, Colgate has historically been able to achieve positive pricing changes across its portfolio most years, averaging a low-single-digit annual boost.

Colgate's advantages show up in the company’s operating margin, which has remained fairly stable and averaged more than 20% over the last decade. Very few companies enjoy such strong profitability. Higher-margin businesses are generally able to compound their earnings faster and fuel significant long-term dividend growth, which Colgate has done for more than 50 consecutive years.

From a growth perspective, Colgate's track record is also remarkable. The company more than quadrupled operating profits over the last 20 years and has consistently reported low- to mid-single digit organic sales growth. Emerging markets are growing 2-3x faster than developed markets, providing a nice tailwind thanks to Colgate's geographic mix (48% of sales were in emerging markets last year).

In addition to emerging market growth, Colgate's investments in new product lines and categories should also drive nice volume growth over the coming years. The company’s 2012 Global Growth and Efficiency Program is also expected to deliver $500 million to $575 million in annual after-tax savings by the end of 2019, allowing Colgate to reinvest in R&D and marketing to continue driving profitable growth.

Overall, Colgate's long-term plan aims to deliver about 4% annual revenue growth and modest margin expansion over time, fueled largely by continued success in emerging markets. Combined with share buybacks, that should help drive mid-single-digit earnings and dividend growth over time.

Source: Colgate Investor Presentation

Key Risks The consumer staples sector attracts many conservative dividend growth investors because its pace of change is typically slow and demand for many of its products is consistent, even in weaker economic climates. For these reasons, the sector is viewed to have lower fundamental risk.

With that said, consumer habits are constantly evolving. For example, many packaged food giants are struggling to shift their sales mix and brand perception into healthier natural and organic foods. Some branded product categories also face increased competition from private label brands, which have meaningfully improved in quality and won over more trust from consumers.

When companies become very large in size and sometimes overextend their product portfolios, it becomes harder to combat these threats in a timely manner. Procter & Gamble (PG) is a prime example in recent years, although its business appears to finally be turning around.

Fortunately, Colgate doesn't seem to have as many of these risks as some of its peers do. Toothpaste doesn’t really face health concerns, and its evolutions (e.g. extra whitening) are minor compared to many other product categories. Colgate can also continue leveraging its brand to create any new product variations that come up in many of its markets and plug them into its existing distribution channels to fight off new threats.

Internationally the company faces a lot of upstarts in most of its markets, who theoretically might have a stronger sense of local consumer tastes. But Colgate's approach to foreign operations is to hire locals to staff its executive ranks. This minimizes the risks of wasting time and investor capital in a fruitless attempt to grow sales overseas, which is why Colgate's international revenues have increased so strongly over the decades.

From a private label risk perspective, most of Colgate's products are very personal items that are used daily by consumers, conditioning them to expect certain tastes, scents, and experiences. Personal products that are used daily seem to have stronger potential to build a more loyal group of consumers that are less willing to try lower priced items on the shelves.

Colgate's historical pricing power and volume growth give some confidence to this assumption, but it's true that the world is changing. Colgate's organic sales growth slowed to just 1% in 2017, and 2018's 0.5% increase shows the trend of slowing growth continues. Part of the problem may be that consumers are becoming savvier shoppers, especially in the age of e-commerce, which has made it far easier for customers to compare prices and reviews between competing brands.

For 2019 management plans to revitalize brands like Hill's pet food Science Diet brand and Colgate Total via new recipes, improved packaging, and greater ad spend. The company has been working on the new Colgate Total toothpaste for a decade and management is very excited about this initiative, calling it "new breakthrough technology, 10 years in the making and protected by numerous patents around the world."

Colgate's innovations to its famous toothpaste include:

Instant odor neutralization

Improved bacteria-fighting power (for enamel protection)

A new cooling agent (for longer minty sensation)

Decreased sensitivity for those with sensitive teeth

The new Colgate Total even has 60 current patents with another 140 pending, but ultimately only global consumers will determine whether those 10 years of R&D were well spent. Management's track record on capital allocation and execution is well above average for the industry so, for now, the company likely deserves the benefit of the doubt.

To protect its pricing power and organic growth profile, Colgate is also increasing its advertising spending and invests more than 70% of its marketing budget in digital initiatives. In 2018 online sales grew 30% and now make up 5% of total company revenue, suggesting that Colgate is performing well in this important channel.

In addition to changing consumer preferences and the threat from private label, the big boys sometimes get into market share battles with each other. The result is lower near-term earnings as higher marketing expenses are needed to protect share. For example, in 2004, Colgate issued a profit warning (its first since 1995) partly as a result of heavy marketing spending necessary to fight off intense global competition, and the stock fell by 11%.

For now, management says it plans to hold the line on prices, even increasing them in 2019 to offset rising input prices. However, raising prices in the current consumer staples environment could negatively impact market share, which investors will want to watch in the coming years to make sure that Colgate is actually able to defend its historically wide moat.

Investors should also note that Colgate's near-term results can be impacted by temporary macro headwinds. Close to 70% of sales are generated outside of the United States, with about 50% of revenue recorded in emerging markets.

A strengthening U.S. dollar dents reported sales and earnings growth, and many emerging markets can also be volatile given their economies' dependence on commodity prices. Demand for Colgate's products is generally inelastic, but the business could experience some hiccups if these potential headwinds arise. However, these events shouldn't impact on Colgate's long-term earnings power and seem more likely to be buying opportunities than anything else.

Closing Thoughts on Colgate With a track record of paying uninterrupted dividends since 1895, a portfolio of household brands, recession-resistant products, numerous opportunities for moderate long-term growth, and dominant market share around the world, Colgate has a lot to offer.

Unlike some of its peers, Colgate could also has a more compelling case for meaningful long-term earnings growth because of its stronghold in fast-growing emerging markets. As per capita spending on hygiene increases around the world, many of Colgate's products should benefit.

Furthermore, since the company is focused on fewer product categories (toothpaste, soap) than many of its large rivals, Colgate could have an easier time expanding into adjacent product categories that leverage its brands and distribution channels.

While private label, e-commerce, and intense competition are legitimate challenges in a number of consumer product categories, Colgate seems to be focused in less price-sensitive areas (e.g. toothpaste) and is investing more aggressively in online sales and digital advertising to stay on top.

Overall, Colgate seems likely to continue moderately expanding its business and dividend over time, just like it has done for many decades. Just keep in mind that management will need to deliver on its 4% long-term organic growth target in order for the company to prove that it is not only a good source of very safe dividends, but modestly growing ones as well.