Medtronic: A Well-Run Dividend Aristocrat in Healthcare

Medtronic (MDT) is one of the classic American success stories, having been founded in 1949 by Earl Bakken and his brother-in-law, Palmer Hermundslie, in a Minnesota medical equipment repair shop.

Over the course of nearly 70 years, the company has grown into one of the world’s largest medical equipment device companies. Today Medtronic's products help treat over 40 medical conditions and 70 million patients around the world each year. The company's medical supplies products are used primarily in hospitals, surgical centers, and alternate care facilities, such as home care and long-term care facilities.

Medtronic's business mix changed significantly when the company acquired Covidien for roughly $50 billion in January 2015. The deal expanded Medtronic's presence in faster-growing emerging markets, bolstered the size and scope of its portfolio of hospital supplies, and helped the company avoid some taxes by relocating its headquarters overseas.

Acquiring Covidien nearly doubled Medtronic’s revenue and should help it gain more leverage and prominence on hospitals’ supplier lists as they increasingly look to cut costs.

Prior to the acquisition, Medtronic was primarily known for its cardiac and coronary devices (defibrillators, pacemakers, valves, heart stents, etc.), diabetes care, spinal fusion, and neural stimulation businesses. Covidien focused on hospital and medical supplies, equipment for surgeries (e.g. surgical staplers), and vascular therapies.

Today the company’s diverse portfolio of products is organized into four main business units with positions in many faster-growing medical technology markets:

Cardiac & Vascular (38% of revenue): pacemakers, implantable defibrillators, cardiac monitoring, and diagnostic systems, and heart valves.

Minimally Invasive Therapy (29%): electrosurgical tools, fixation meshes, blood vessel sealing technology, vessel ablation products (for prevention of heart attacks and strokes), and patient monitoring systems such as endoscopic devices.

Restorative Therapies (26%): for helping patients with brain, pain, and injury recovery, as well as special needs such as reproductive and digestive problems.

Diabetes (7%): real-time blood sugar tracking and insulin management pumps, as well as less invasive diabetes treatment systems.

Source: Medtronic Investor Presentation

By geography, Medtronic generates approximately 53% of its revenue in the U.S., followed by international developed markets (32%) and emerging markets (15%), which are consistently recording double-digit growth.

With 41 consecutive years of dividend growth to its credit, Medtronic is a dividend aristocrat. Management has said it plans to continue growing the dividend each year, matching growth in the company's earnings over the long term to maintain a payout ratio near 40%.

Business Analysis

Medtronic’s success over the decades has largely stemmed from its unrelenting focus on continually innovating new medical products to meet the needs of a fast-growing and aging global population.

That means a rich history of significant R&D spending (over $2 billion per year, or 7% to 8% of total revenue), which has led to world-changing inventions such as the pacemaker in 1957 and an intellectual property portfolio of 46,000 patents.

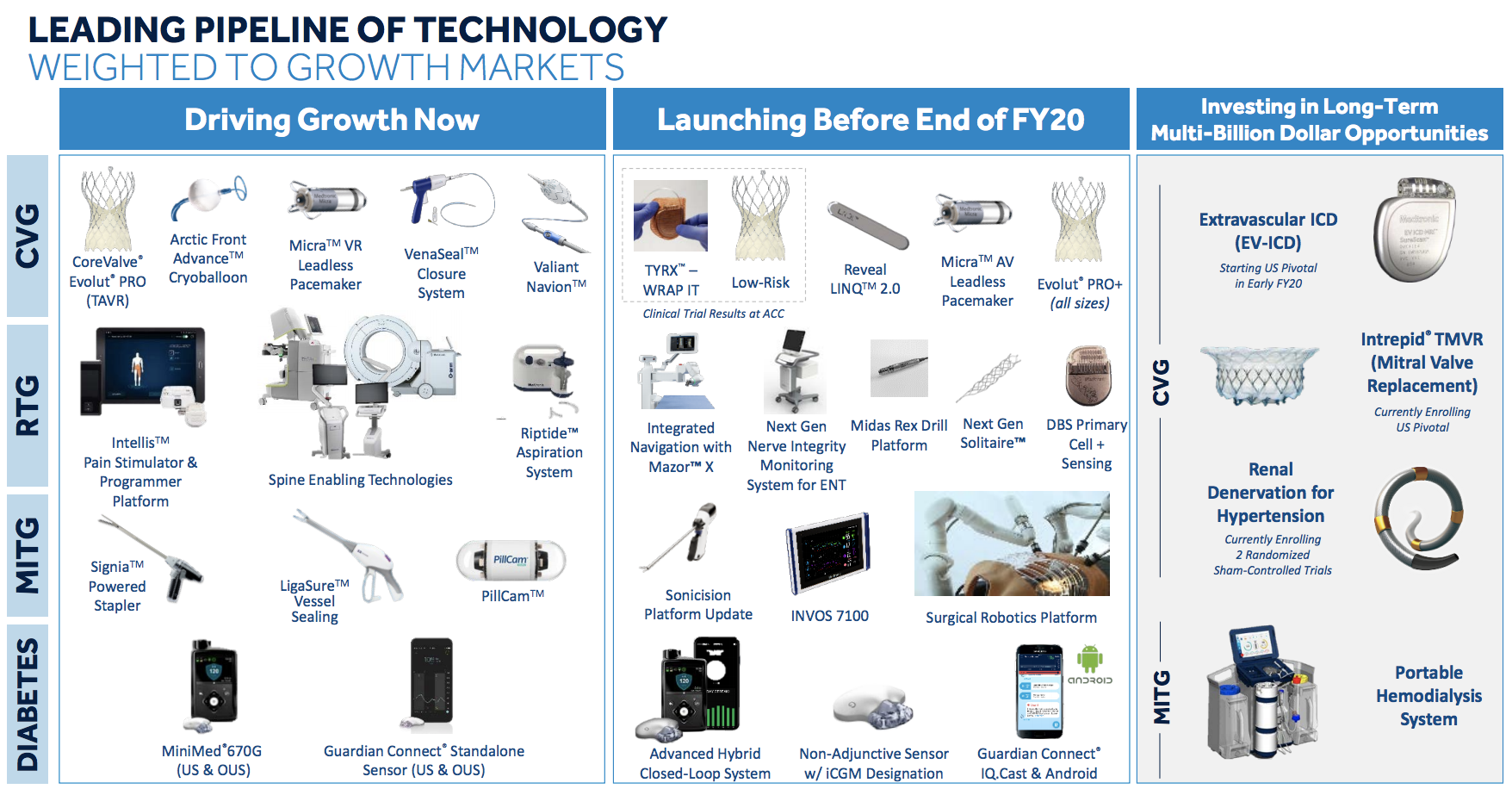

Medtronic's current R&D pipeline includes over 350 clinical trials to launch new products or expand the conditions its existing products can treat. The company's future technology plans cover everything from surgical robotics systems to vessel sealing instruments, including a number of multi-billion dollar opportunities.

Source: Medtronic Investor Presentation

Given the price-sensitive nature of the healthcare industry, developing successful new technologies and medical devices is essential to maintaining market share and healthy profitability. What's more, U.S. healthcare reform has raised the bar for securing reimbursement for new technologies (more obvious improvements over the current standard of care are required), which entrenches the current market positions of the industry's largest incumbents.

Many of Medtronic’s medical devices also significantly impact patients’ quality of life and must be of extremely high quality. The company’s specialized products can offer superior performance in many instances, allowing Medtronic to maintain strong market share and profitability.

Meanwhile, surgeons generally do not like switching to new device makers, since doing so can result in higher risks to patients and requires doctors to alter their operating habits. All of these factors have helped Medtronic establish and maintain a solid position in the industry over the course of decades.

Thanks to a disciplined and well-executed acquisition strategy, such as its $50 billion acquisition of Covidien, Medtronic has also extended its sales reach into new promising treatment areas, as well as faster-growing emerging markets. Over 10% of Medtronic's revenue now comes from China, India, and Latin America, which have consistently recorded double-digit growth for years.

Medtronic routinely makes smaller tuck-in acquisitions as well to help it maintain and increase its lead in advanced medical technology. From fiscal 2015 through 2019 the company invested $6 billion in acquisitions and strategic investments, for example.

This combination of operating in a defensive (i.e. recession-resistant) industry, investing heavily in R&D, and making smart acquisitions has allowed Medtronic to generate positive sales growth for more than 10 consecutive years.

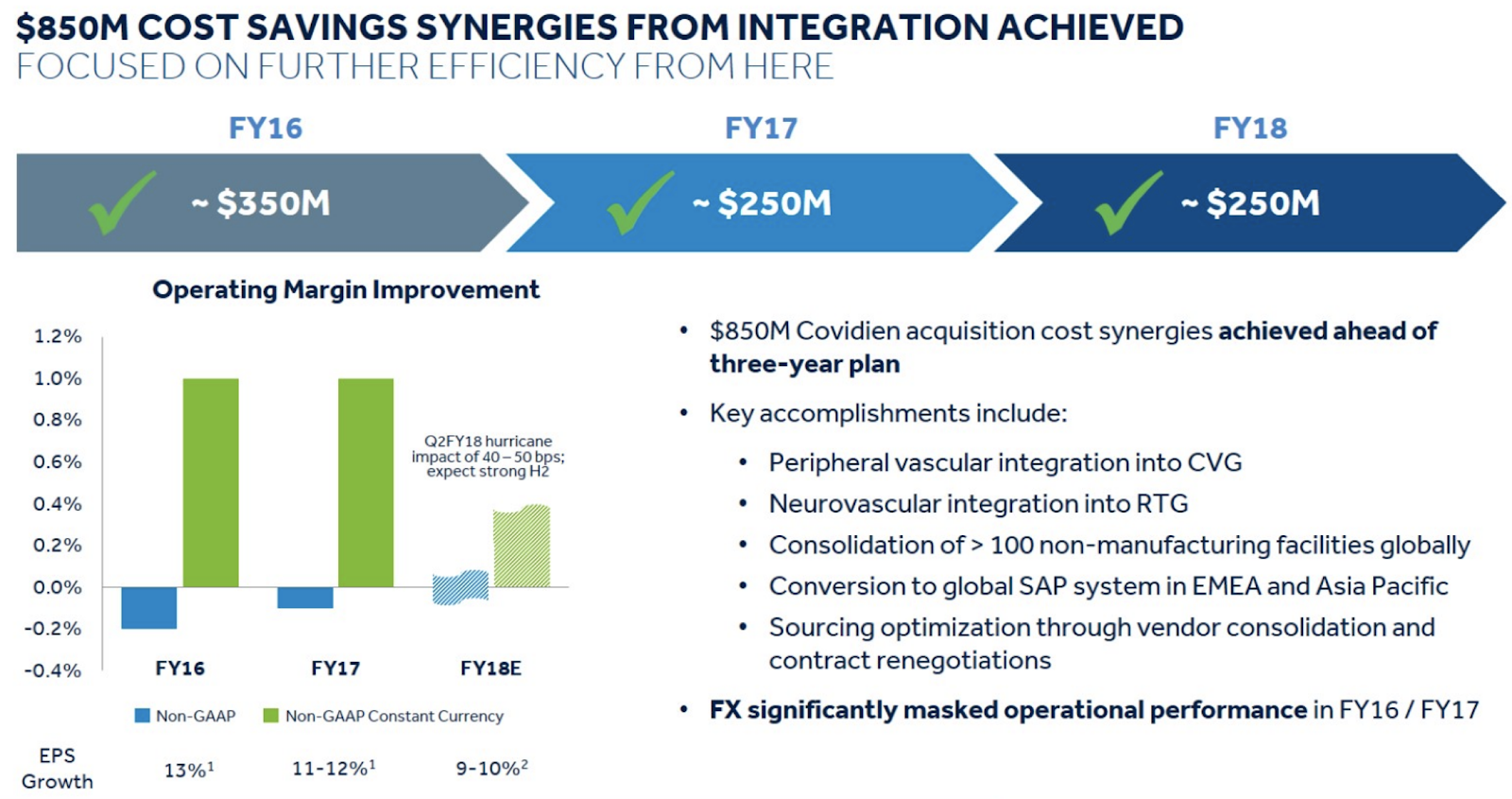

Most importantly, Medtronic’s management team has proven to be a group of skilled capital allocators. As a result, Medtronic has consistently delivered on its long-term profitability goals, such as the $850 million in synergistic cost savings that were an important component of the decision to buy Covidien. The company even delivered those savings by January 2018, earlier than initially planned.

Source: Medtronic Investor Presentation

Management aims to expand the company's operating margin by 40 basis points to 50 basis points per year over time, through shifting to higher margin products and continuing to execute on various cost-cutting and efficiency initiatives.

Combined with a willingness to part with slower-growing and less profitable businesses, such as selling its medical supplies business to Cardinal Health (CAH) for $6.1 billion in 2017, Medtronic has consistently achieved impressive operating margins north of 20%.

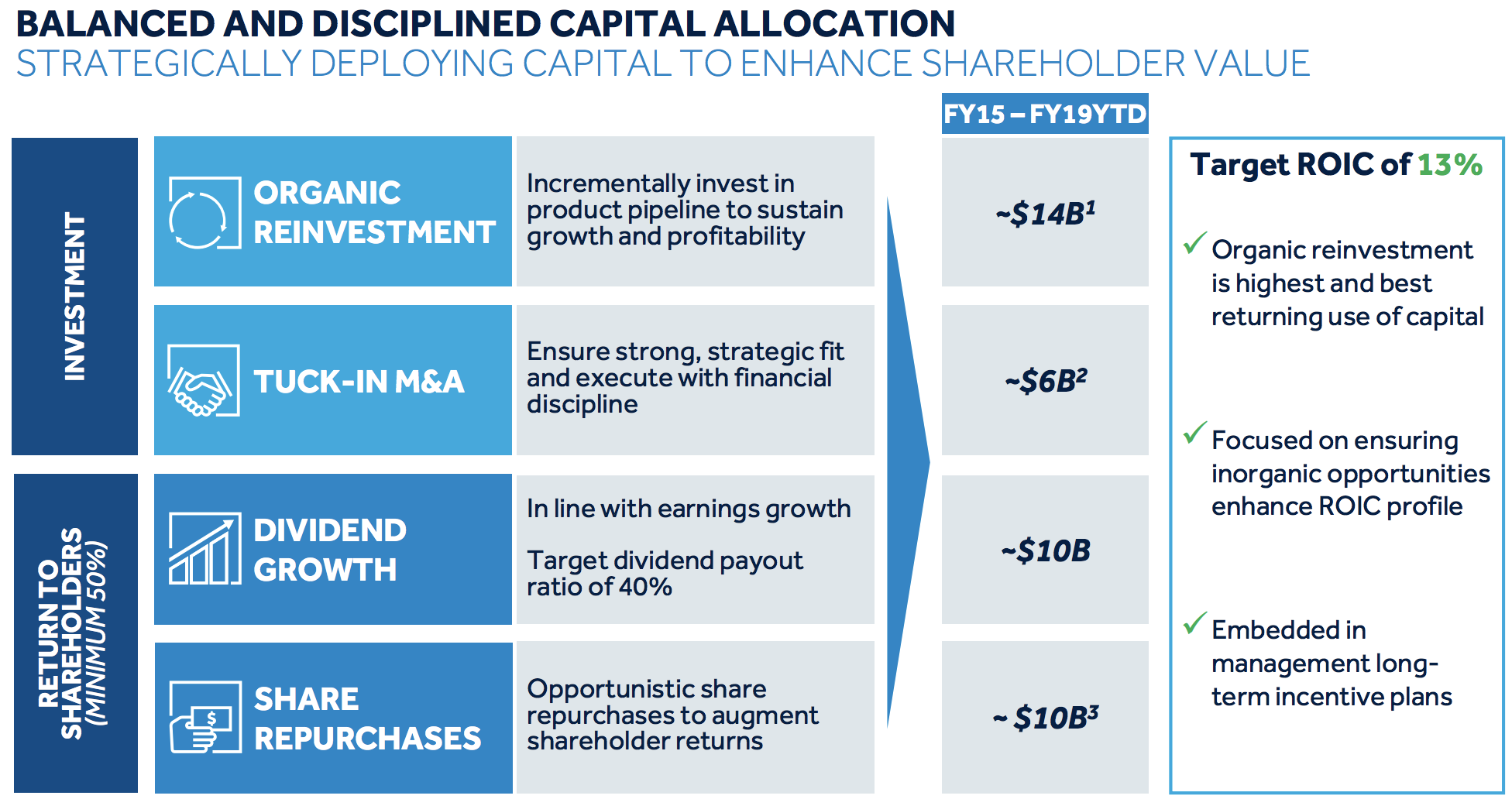

The company's solid profitability has also helped it generate excellent free cash flow. Management has committed to return at least 50% of free cash flow to shareholders in the form of buybacks and dividends.

Of course, a shareholder-friendly corporate culture, while necessary for a dividend aristocrat, isn’t sufficient. Management also has to strike a good balance between using cash flow to invest in the company’s future growth, maintain a strong balance sheet, and reward income investors with the steadily rising dividend they’ve come to expect from the company.

Fortunately, Medtronic maintains a solid capital allocation strategy that should continue serving it well in the future. The company expects to use its free cash flow and healthy balance sheet to continue rewarding shareholders while selectively reinvesting in high return on invested capital opportunities that allow it to maintain a strong investment-grade credit rating (an "A" from Standard & Poor's).

Source: Medtronic Investor Presentation

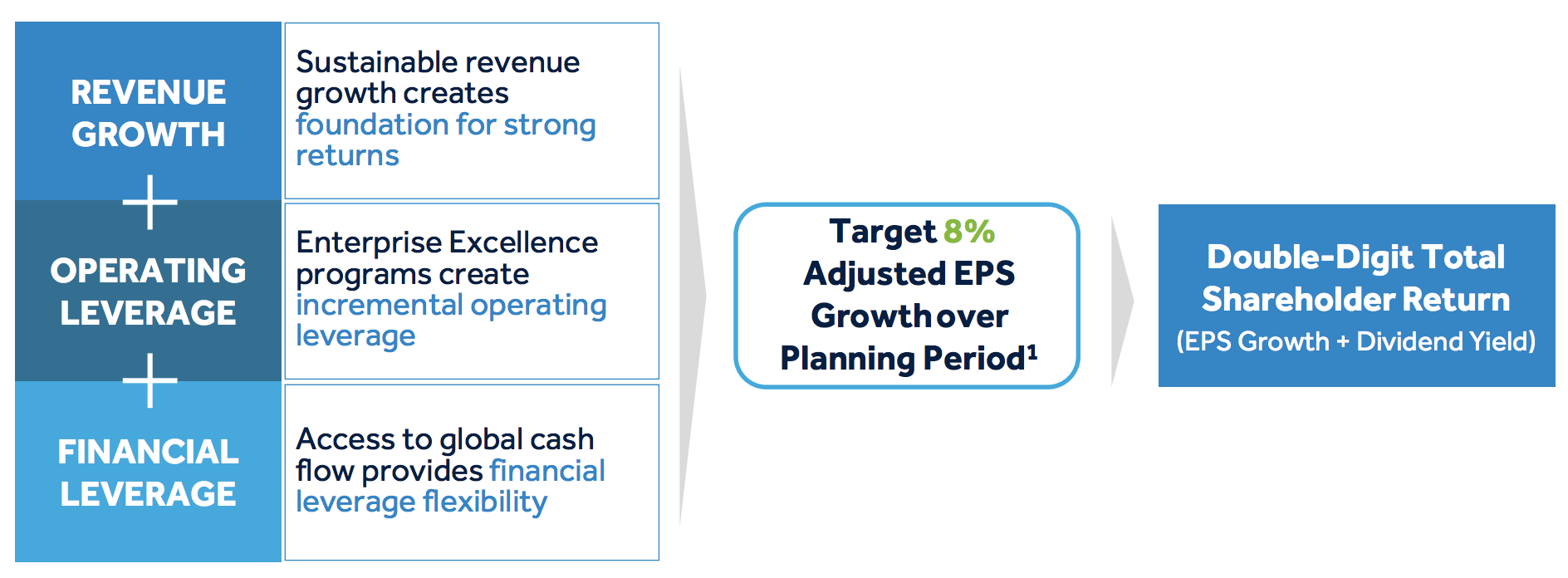

All of which means that Medtronic, thanks to its large economies of scale, strong dedication to R&D, new product development, and opportunities in emerging markets, seems likely to continue delivering mid-single-digit annual revenue growth and high single-digit earnings and dividend growth for years to come.

Source: Medtronic Investor Presentation

Overall, Medtronic’s primary advantages come from its ability to continuously develop specialized medical devices in profitable and fast-growing areas of the healthcare market. The company’s diversified product portfolio and the recession-resistant nature of its products provide reliable free cash flow which can be reinvested into the business to drive future growth.

As the healthcare industry focuses more on taking out costs, larger vendors such as Medtronic have potential to benefit because of their economies of scale, product breadth, unique technologies, and existing customer relationships.

Key Risks

Dividend aristocrats are generally low-risk stocks, given their long track records of steady growth, long-term focused management teams, and shareholder-friendly corporate cultures. However, that doesn’t mean there aren’t risks to consider.

For example, because Medtronic’s sales are increasingly coming from overseas, the company has a growing foreign exchange risk. Specifically, if the U.S. dollar is very strong, the company's reported sales and earnings growth rates can face headwinds. Fortunately, this risk shouldn't affect Medtronic's long-term potential.

Next, while Medtronic has a generally good history of acquisitions, both large and small, investors need to realize that every deal comes with execution risk. Management could overpay for a company or fail to achieve expected synergies from a large acquisition in the future.

For example, in 2008 the company purchased Kyphon for $3.9 billion to increase its market share in back surgery devices, which were rapidly growing and carried high margins at the time. However, expected cost synergies weren't achieved, and the back surgery market ended up growing much slower than expected. Medtronic ultimately took a write-down on this deal, recognizing it overpaid for the business.

Risks can be even higher in the medical field where small bolt-on acquisition targets, which make up the majority of Medtronic’s deal flow, are usually privately held companies.

Not only is it harder to value such firms, but because many of their products are in early development, it can take several years and millions of dollars of incremental R&D spending before Medtronic sees any sales or earnings to recoup its investment.

The biggest risk of all, however, is government regulation and potential changes to Federal healthcare policy.

For example, while the passage of the Affordable Care Act (i.e. ObamaCare) resulted in 17 million Americans gaining healthcare coverage, and thus increasing Medtronic’s customer base, the law also instituted a 2.3% medical products excise tax which lowered the company’s profits.

The tax was suspended from 2016 through 2017, but despite efforts by the Trump administration to repeal the tax, it went back into effect for 2018. Furthermore, the penalty for Americans not complying with the Obamacare individual mandate was repealed as part of the tax bill that passed in December 2017. The Congressional Budget Office expects that the repeal will result in four million more uninsured by 2019 and 13 million more by 2027.

Should future healthcare reform initiatives result in lower spending and more Americans losing health insurance coverage, Medtronic could face a scenario in which its slower future earnings potential (from higher medical taxes) is no longer offset by the increased demand created by more customers. The company's international diversification helps mitigate this risk to a degree, but the U.S. remains its most important region.

Meanwhile, operationally the company faces regulatory risk from dealing with so many agencies including the U.S. FDA, Department of Justice, Health and Human Services Office, and numerous other governmental authorities. Medtronic has to deal with hundreds of regulators in its 150-plus markets, which sometimes means its products don't get approved or fail to make it to market on time or on budget.

It's also worth noting that the proposed "Medicare-For-All" single-payer health system that's a cornerstone of many 2020 Democratic campaign platforms would also hurt the profits of virtually all medical companies. Under this idea, the U.S. government would essentially become the single client for all medical companies and either negotiate or use price regulations to push prices down across the healthcare chain.

Such a sweeping healthcare overhaul in America seems unlikely to ever make it through Congress, but private payers are attempting to put the squeeze on medical suppliers as well. As a result, many parts of the healthcare space are consolidating. Larger size creates stronger pricing power for insurance companies, health maintenance organizations, and vertically integrated giants like CVS, which now operates in pharmacy, pharmacy benefits management, and health insurance.

Most medical device markets are already fairly ruthless as well, despite some of their high-tech innovations. Products generally have short life cycles, are notoriously price-sensitive, and require constant R&D to maintain their market share.

Medtronic has meaningful scale ($30 billion in sales), strong market positions in its key segments, and a highly diversified product portfolio, but the company still had to reduce prices meaningfully during 2010-11 as the economy was slow to recover from the recession.

Simply put, despite its recession-resistant cash flow and potentially long runway for growth, the healthcare sector is complex. Sticking with blue-chip stocks such as Medtronic can help reduce some of these risks, but no company is immune from future growth challenges as the space continues evolving.

Closing Thoughts on Medtronic

While Medtronic’s low yield may not make it an option for all dividend investors, the company is one of the fastest-growing and perhaps most appealing dividend aristocrats in the healthcare sector.

Not only has Medtronic’s long track record of double-digit dividend growth proven its business model has staying power in all sorts of economic, political, and interest rate environments, but its future high single-digit dividend growth potential remains attractive.

Despite some of the uncertainty surrounding future government healthcare reform, it’s hard not to like the company’s diversified cash flow generated from numerous product lines, Medtronic’s large scale, which makes it an even more compelling supplier for hospitals, and the company’s exposure to emerging markets and an aging global population. All these factors will likely drive higher demand for medical devices over the coming years.