V.F. Corp: An Apparel Maker With Double-Digit Dividend Growth Potential

Founded in 1899, V.F. Corp (VFC) is a global lifestyle apparel maker in the outerwear, footwear, backpack, luggage, accessory, sportswear, occupational, and performance apparel categories.

The company owns about 20 well-known brands, including Vans (34% of sales), The North Face (24%), Timberland (17%), and Dickies (7%). Activewear generates 42% of V.F. Corp's revenue, outdoor apparel contributes another 42%, and workwear generates the remaining 16%.

Source: V.F. Corp Annual Report

About 60% of the firm's revenue is generated from selling its products on a wholesale basis to retailers, and the remainder is sold direct-to-consumer either online (10% of sales) or through V.F. Corp's company-owned retail stores (30%).

Geographically, V.F. Corp is very global with about 45% of its sales generated outside of the U.S.

Adjusted for the 2019 spin-off of its jeans business, V.F. Corp has paid higher dividends each year since 1973 and is committed to double-digit dividend growth.

Business Analysis The consumer apparel industry is highly discretionary and marked by ever-changing fashion tastes and shopping habits, making it one of the more challenging spaces for companies to generate predictable cash flow.

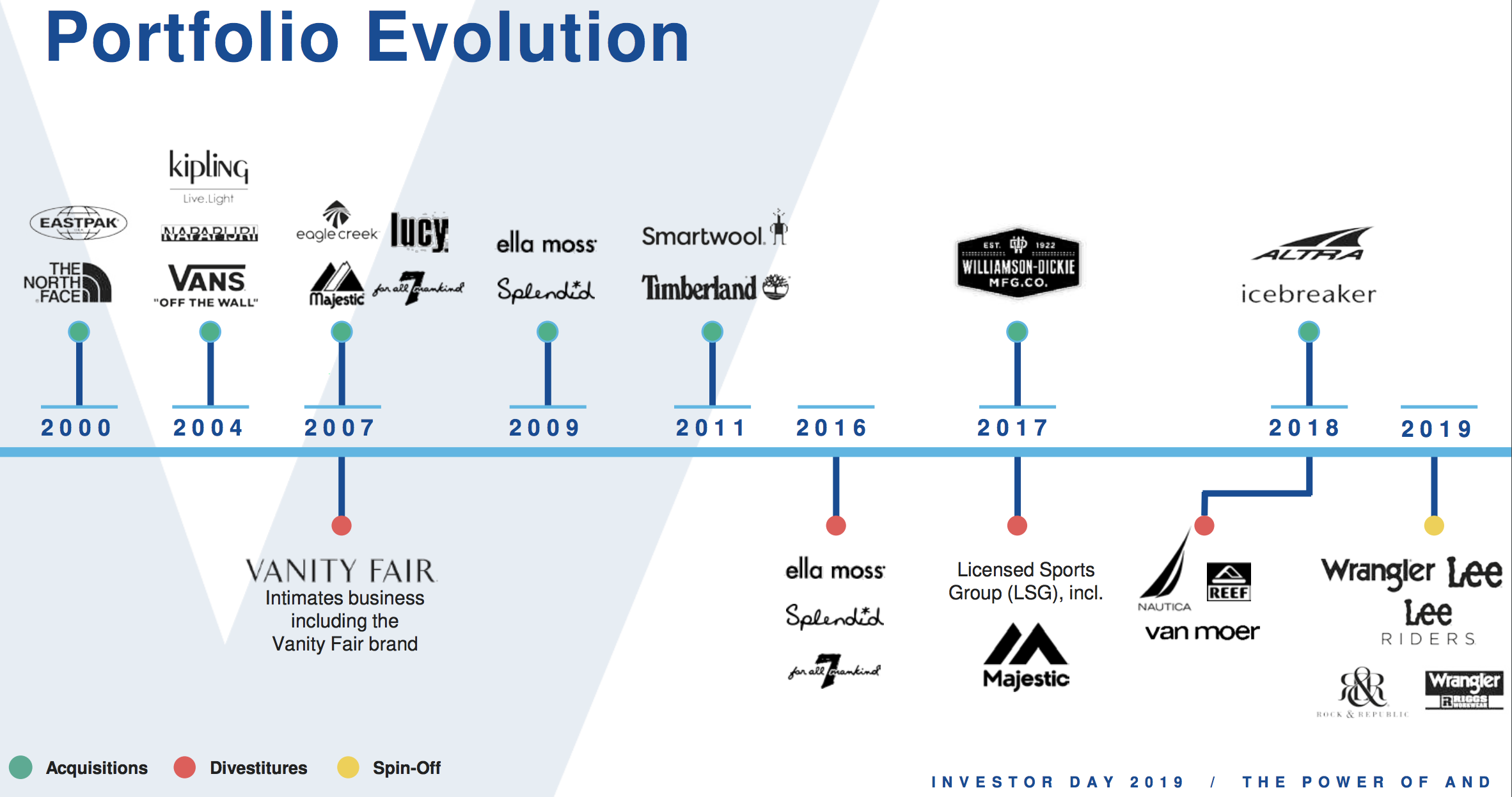

Unlike many of its apparel peers, V.F. Corp has done a remarkable job reinventing its portfolio of brands to stay relevant over time.

In fact, the firm's four largest brands – Vans, The North Face, Timberland, and Dickies – generate over 80% of V.F. Corp's revenue today but weren't even part of the company 20 years ago.

V.F. Corp is known not for creating new brands in-house but rather acquiring them and then improving them over time. Management's goal is to only acquire brands that it believes can generate at least a 15% return on investment within three years, and eventually achieve $1 billion or more in annual sales.

While V.F. Corp has had to exit some categories that ran into growth challenges (e.g. denim jeans), the firm has a great long-term track record of opportunistically scooping up promising brands and developing them into juggernauts.

Source: V.F. Corp Investor Presentation

V.F. Corp acquired The North Face for $25 million in 2000 when the struggling company was at risk of filing for bankruptcy. The North Face brand generates over $2 billion in annual revenue today, representing about 25% of V.F. Corp's sales.

Similarly, V.F. Corp bought Vans for about $400 million in 2004. Vans' revenue was stagnating around $350 million but has ballooned to more than $3 billion under V.F. Corp's watch, accounting for more than a third of the firm's total business.

The firm also purchased Timberland for $2.3 billion in 2011, doubling its footwear business, and it paid $820 million in 2017 for Williamson-Dickie, establishing itself as leader in workwear.

V.F. Corp invests significantly in advertising, consumer research, and in-house production (the company makes about 20% of its own goods) to strengthen each brand's image and extend it into new product lines and geographies.

For example, Vans was once a brand dominated by skating culture (male-focused) but the company has successfully made it into a lifestyle brand that's now 60% bought by women and focused on a wide range of footwear and apparel.

The company's marketing focuses not only on print, digital, and TV ads, but also includes sponsoring sports and music events, as well as charity programs. V.F Corp has long prided itself on being a company that values "people, planet, and profit", aligning its values with those shared by many Millennials.

Combined with efforts to grow its direct-to-consumer business, which accounts for about 40% of revenue and provides the company with more control over a customer's experience, V.F. Corp has done a great job making consumers feel a strong connection to the messages of its brands.

As a result, most of the company's products command premium prices and high margins. Few retailers own brands that have been able to retain such consistent brand loyalty and steady sales and market share growth.

Going forward, the company's four mega brands will dictate V.F. Corp's success. Management expects these brands to collectively grow at a high single-digit pace, driving double-digit EPS and dividend growth.

Your guess is as good as mine regarding how large each of these brands can ultimately become. V.F. Corp believes its addressable market is approximately $500 billion, implying its brands have less than 3% market share.

Nike, a global footwear and apparel maker, is also about three times the size of V.F. Corp, suggesting there's plenty of room to continue expanding, especially as management hunts for new brands it can develop.

Simply put, an investment in V.F. Corp is a bet that the company's core brands are far from reaching a saturation point and that management will be able to continue adapting V.F. Corp's portfolio of brands as consumer trends evolve.

Key Risks Fickle consumer tastes pose one of the biggest risks to apparel makers, especially when it comes to high-priced clothing and footwear. Given the unpredictable nature of fashion trends and the difficult of identifying durable brands, my general preference is to avoid the industry.

V.F. Corp's long-term track record makes it one of the few companies worth considering in this space, but its concentrated brand portfolio creates risk. With more than 80% of sales coming from just four brands (and over 30% from Vans), V.F. Corp's long-term growth goals are dependent on strong brand execution.

Unfortunately, it's hard to discern how long of a runway V.F. Corp's brands have left. If the company's major brands reach maturity sooner than expected, then management may need to reinvent V.F. Corp's portfolio once more.

Not unlike a concentrated stock portfolio, the future could work out very well for V.F. Corp if its powerhouse brands continue their strong growth. However, investors could also be left disappointed if consumers lose some interest in the outdoor and action sports apparel categories.

While these certainly seem like clothing mainstays, consumer preferences could still evolve within these categories and favor new brands or styles that emerge.

It wouldn’t hurt if V.F. Corp had greater brand and product category diversification, but the firm's existing brands have shown impressive durability over time. Risk is also mitigated somewhat by management’s ability to grow or acquire new brands and plug them into the company’s existing distribution network.

However, while V.F. Corp has historically grown through sizable brand acquisitions, management may struggle to locate sufficiently high-quality and profitable buyout targets to continue this trend given the company's size.

That's not necessarily a problem as long as V.F. Corp's core brands continue their current trajectories, but it keeps the firm's portfolio concentrated and could V.F. Corp's long-term pace of growth.

Finally, several short-term risks could hurt V.F. Corp's performance any given quarter. Foreign currency exchange rate fluctuations, shifts in consumer spending, weather, raw material costs, inventory management issues, and weakness at brick-and-mortar retailers are all examples. However, none of these risks seem likely to threaten the company’s long-term earning power.

Closing Thoughts on V.F. Corp Few industries can be as hard to invest successfully in as retail, thanks to unpredictable fashion trends, the cyclical nature of the business, and the potential disruptive threat of e-commerce.

However, V.F. Corp's long-term approach to investing in a portfolio of top brands, overseas market expansion, and online sales make it one of the few retail-focused firms that conservative dividend growth investors may consider, assuming they are comfortable with the risks created by the firm's brand concentration.

When combined with V.F. Corp's conservative balance sheet and strong free cash flow generation, the company should have no trouble continuing to raise its dividend for the foreseeable, just like it has every year since 1973.