Dominion Energy Offers to Buy Out Its MLP Dominion Midstream Partners

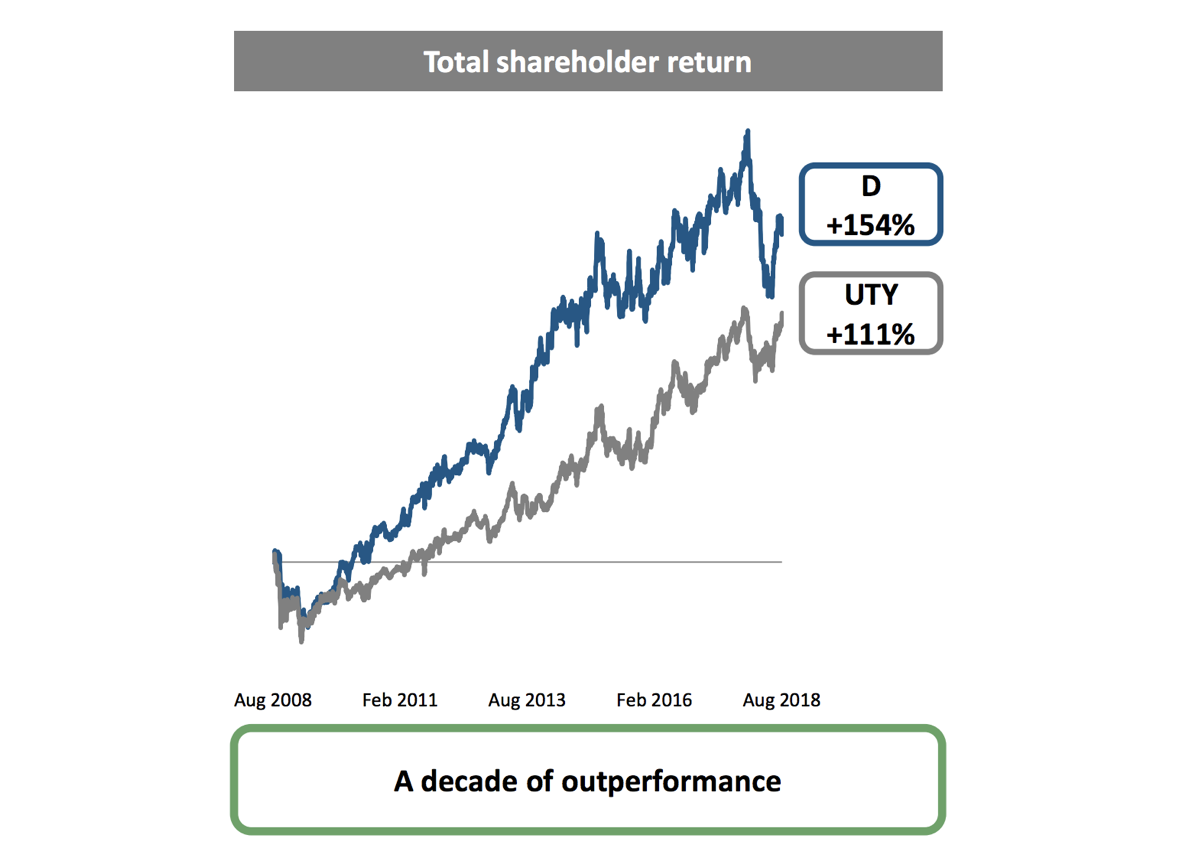

Dominion Energy (D) has managed to significantly outperform most other regulated utilities over the past decade, establishing itself as a quality dividend growth investment. A large driver was the utility's expansion into midstream infrastructure, specifically natural gas and liquified natural gas (LNG) storage, transportation, and export capacity.

However, in recent years the midstream industry has faced major headwinds, and now Dominion Energy has announced it feels it has to radically change its midstream growth strategy by offering to buy out its MLP, Dominion Midstream Partners (DM).

Let's take a look at what this means for investors in both stocks, but especially what implications it has for the future growth prospects of Dominion Energy's earnings and dividend.

Why Dominion Energy is Offering to Buy Out Dominion Midstream Partners

Dominion Midstream Partners is a midstream MLP which was set up by Dominion to serve as a funding vehicle for its fast-growing midstream business. Under this arrangement, Dominion Midstream would raise debt and equity capital from investors to buy Dominion Energy's midstream assets (pipelines, etc.), once long-term contracts were in place.

As a result, the MLP would benefit from rapidly growing distributable cash flow to fund its generous and fast-growing payout (20+% annual growth since its 2014), and Dominion could quickly recoup the large costs it incurred to construct these valuable, long-lived assets.

Specifically, since Dominion owns 51% of DM's limited partner units and its incentive distribution rights, about 75% of the cash flow from Dominion Midstream's long-term, fixed-fee and volume committed contracts flowed back to Dominion Energy, who serves as the MLP's sponsor. Dominion could use this cash to fund additional growth initiatives, strengthen its balance sheet, and fuel its own strong dividend growth.

Two major midstream projects that Dominion Energy has recently completed or is in the process of building are the $4 billion Cove Point LNG export terminal and the $5 billion Atlantic Coast Pipeline (ACP). Dominion Midstream Partners was expected to be an important financing vehicle to back these opportunities.

The ACP is 48% owned by Dominion Energy and is expected to be completed by the end of 2019. The pipeline will transport cheap gas from the booming Marcellus/Utica shale to supply Dominion's customers in Virginia and North Carolina with low cost gas and gas generated electricity.

However, in March the Federal Energy Regulatory Commission (FERC), which regulates much of its midstream assets, changed an important tax rule that disallowed MLPs from deducting a tax allowance from cost of service contracts on interstate pipelines (those regulated by FERC), starting in 2020.

While FERC revised the policy in July to be less damaging to MLPs, the market's uncertainty over what this would mean for Dominion Midstream's cash flow still resulted in its unit price collapsing nearly 50% from its 2018 high.

As a result, the MLP could no longer affordably issue equity to buy Cove Point and other midstream assets from Dominion. As a result, Dominion Energy determined that its MLP can no longer serve its function as a funding vehicle.

Therefore, on September 19, 2018, Dominion offered to buy out the 49% of remaining DM units it doesn't already own for a fixed ratio of 0.2468 Dominion shares for each Dominion Midstream unit that investors hold.

At the time, that offer represented a price of $17.75 per unit or an 8.2% premium to the MLP's average 30-day unit price. Management expects a buyout deal to be struck by the end of the year and the acquisition to be completed in the first quarter of 2019.

Here is Dominion Energy CEO Thomas Farrell's rationale for the deal:

"Continued weakness in MLP capital markets combined with the prolonged disruption in Dominion Energy Midstream's (DM) common unit price since the March 15 Federal Energy Regulatory Commission policy revision were key factors that led to this decision...The proposed transaction would provide a premium to recent market trading levels for DM common unitholders and also benefit Dominion Energy shareholders by removing uncertainty as to the future of DM and the potentially negative impact of changes in FERC tax policy to the future cash flows of current DM assets."

In other words, by buying out Dominion Midstream in a $1.1 billion all-stock deal, management believes it can eliminate the negative cash flow implications of the FERC rule change (since those only apply to MLPs).

In addition, by eliminating the uncertainty of how it will fund its midstream growth, the company believes Dominion's stock will lose an important overhang that has caused its share price to fall over 10% in 2018.

But what exactly does Dominion's abandoning of the midstream MLP business model mean for investors in both Dominion Midstream and Dominion Energy itself?

What the Buyout Deal Means For Dominion Midstream Investors

The buyout offer has yet to be accepted by Dominion Midstream's board of directors or conflict committee. However, given DM's low unit price and the extremely low probability that the MLP's price will recover sufficiently to buy Cove Point or ACP, Dominion Midstream investors have to assume that they will end up owning shares of Dominion Energy if they continue holding their investment.

There are several important implications for Dominion Midstream unitholders to understand. First, you will end up with much less dividend income once the deal closes since Dominion Energy's yield is lower. Specifically, your annual dividend income will drop by about 41% once the deal closes based on each company's current payout and the share exchange ratio proposed by Dominion Energy.

The other implication has to do with taxes. MLPs are taxed very differently from corporations like Dominion Energy. And since this buyout, if it's approved (very likely), will be a corporate conversion, that means that any deferred tax liabilities Dominion Midstream investors have accrued over the years will have to be paid.

And most unfortunately of all, the buyout price, which is a fixed ratio of shares, means that anyone who bought the MLP at a high cost basis will be looking at a potentially significant (though unrealized) capital loss. Eventually shares of Dominion will hopefully recover enough to offset these losses, but only if investors don't sell their MLP units and are willing to wait a number of years.

What about the impact on Dominion Energy's business model? Fortunately, the effect on Dominion Energy's long-term EPS and dividend growth is likely to be minimal.

What the Buyout Deal Means For Dominion Energy Investors

Before the FERC rule change tanked Dominion Midstream's unit price and cut it off from equity markets, Dominion Energy was guiding for 10% dividend growth in 2018, 2019, and 2020. This was among the fastest payout growth rates of any regulated utility.

After the FERC rule change, management amended its dividend growth guidance to 10% in 2018 and 2019 and "6% to 10%" in 2020, depending on whether or not Dominion Midstream's unit price recovered sufficiently to allow it to buy Cove Point.

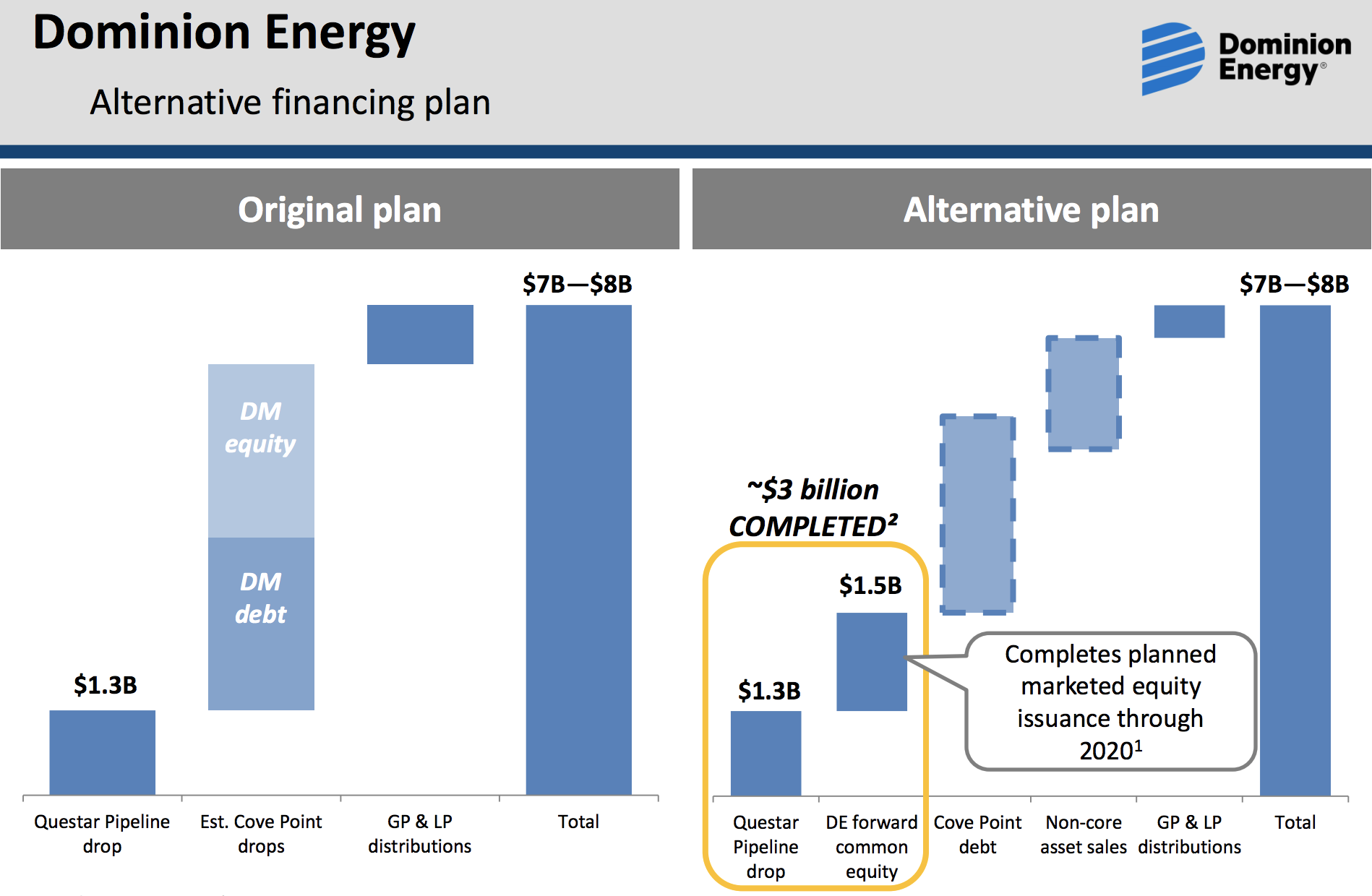

In total, between 2016 and 2020 Dominion Energy was planning on receiving $7 billion to $8 billion from Dominion Midstream, a combination of drop down proceeds from Cove Point and distributable cash flow sent back to the sponsor.

Following the FERC rule change, management had to adapt its long-term growth financing plans to include issuing its own loan to finance Cove Point, selling non-core assets, and issuing new Dominion shares.

Source: Dominion Energy Investor Presentation

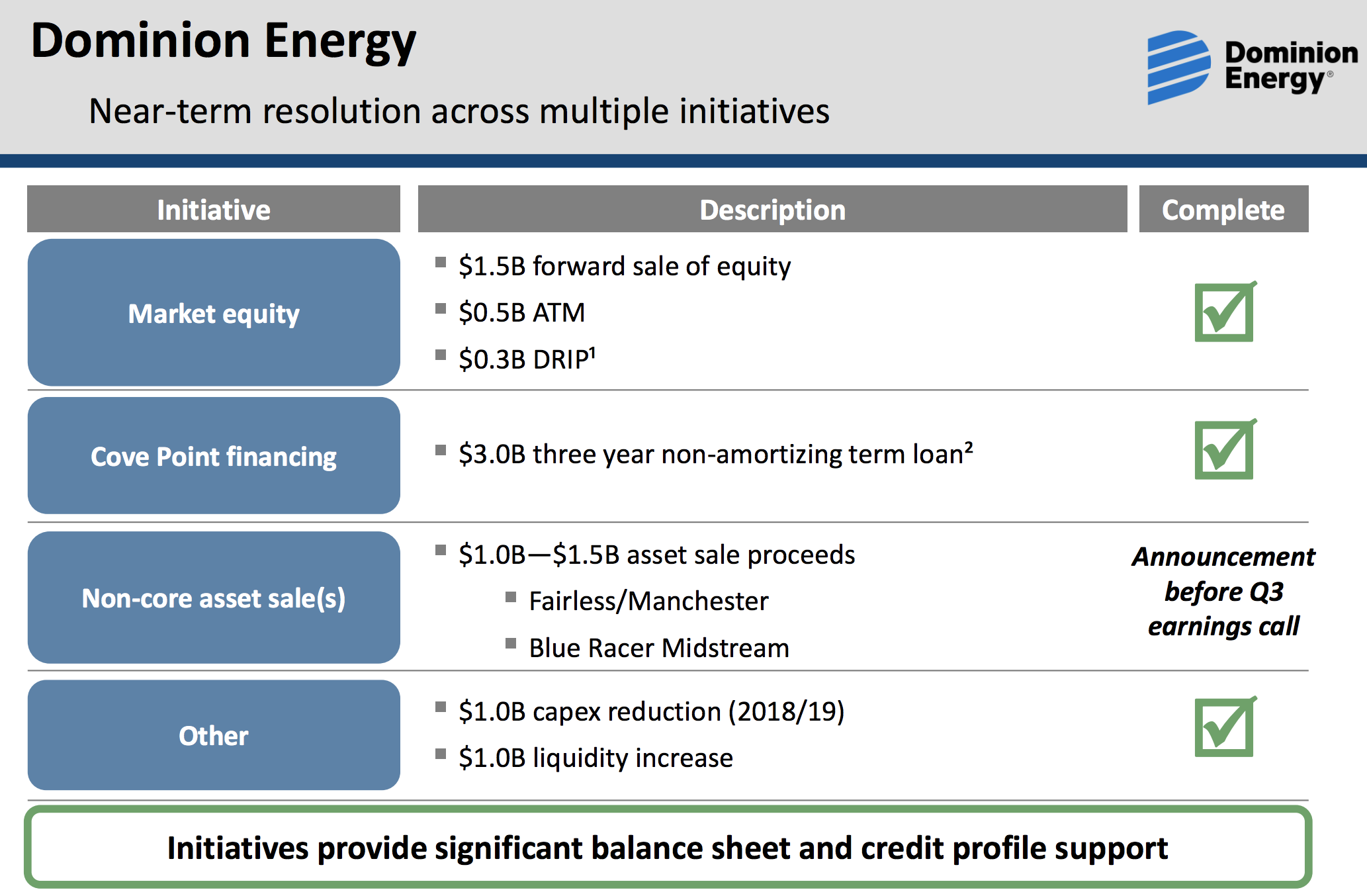

Fortunately, according to CEO Thomas Farrell, "Dominion Energy has already successfully completed several steps that will allow us to achieve our earnings and credit objectives."

In the past few months, Dominion has successfully tapped alternative financing options including:

Raising $2 billion in equity

Obtaining a $3 billion low interest term loan on Cove Point

Selling three non-core three merchant generation assets for $1.3 billion

Source: Dominion Energy Investor Presentation

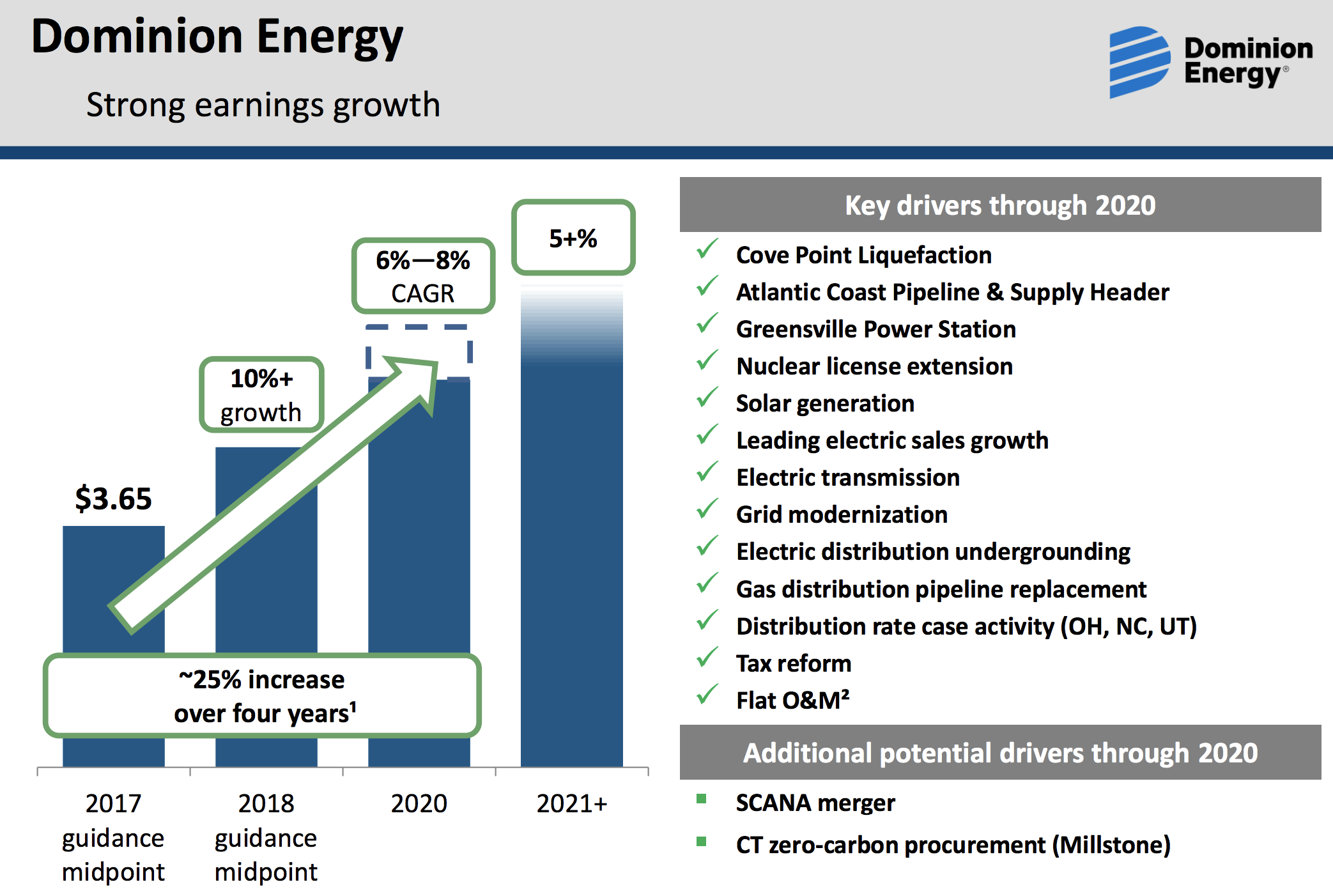

In total, Dominion thinks it now has sufficient capital to avoid further equity issuances through 2020 and complete its $11.4 billion in planned growth projects through 2020.

Most importantly, Dominion Energy expects the MLP buyout to be neutral to its earlier EPS guidance and credit rating. That's because upon acquiring Dominion Midstream, the company will retain 100% of its highly stable cash flow.

What this effectively means for Dominion Energy investors is that management is reiterating its updated EPS growth guidance of last quarter which called for at least 10% EPS growth in 2018, about 7% annual growth through 2020, and "at least 5%" growth beyond 2020.

Source: Dominion Energy Investor Presentation

Should management's assumptions play out as expected (including the planned acquisition of SCANA), Dominion Energy's dividend can likely be expected to grow at 10% in 2018 and 2019, and 6% in 2020. Beyond that, dividend growth is likely to slow to a mid-single-digit pace, which is still better than the payout growth rates put up by most regulated utilities.

Closing Thoughts on Dominion Energy's Planned Buyout of Dominion Midstream

Even great dividend stocks run into challenges over time. The key to long-term income investing is owning well-run businesses, with management teams that can adapt to changing industry conditions.

The failure of Dominion Midstream to live up to its purpose as a funding vehicle for Dominion Energy is disappointing. But ultimately it shouldn't put the utility's dividend at risk and appears to have only minimally impacted Dominion's long-term earnings and payout growth prospects.

Dominion Midstream investors aren't so fortunate as they face a potentially painful distribution cut and negative tax liabilities from this buyout. These investors must now decide if they want to cut bait and reallocate their capital elsewhere, or accept the buyout offer and ultimately receive an ownership stake in Dominion Energy.

Despite this most recent midstream setback, Dominion Energy still has a solid base of predictable regulated businesses, a strong financial profile, and a number of attractive long-term growth drivers. In other words, the stock appears to remain a reasonable holding as part of a well-diversified dividend growth portfolio.

However, investors considering Dominion Energy need to be comfortable with the proposed SCANA merger, which should have a final verdict by the end of 2018. If it goes through, this deal could prove to be an excellent opportunistic acquisition by Dominion, but it also comes with its fair share of risks given the large size of the acquisition and the liabilities Dominion could inherit related to SCANA's partially-completed nuclear plant.

For now, management continues to deserve the benefit of the doubt.