McCormick Has Double-Digit Dividend Growth Potential

Established in 1889, McCormick (MCK) manufactures and distributes over 16,000 spices, seasoning mixes, condiments, and other flavorful products to the entire food industry – retail outlets, food manufacturers, and foodservice businesses.

Some of the company's leading brands include McCormick, French's, Frank's RedHot, Lawry’s, Club House, Zatarain’s, Thai Kitchen, and Simply Asia.

Source: McCormick

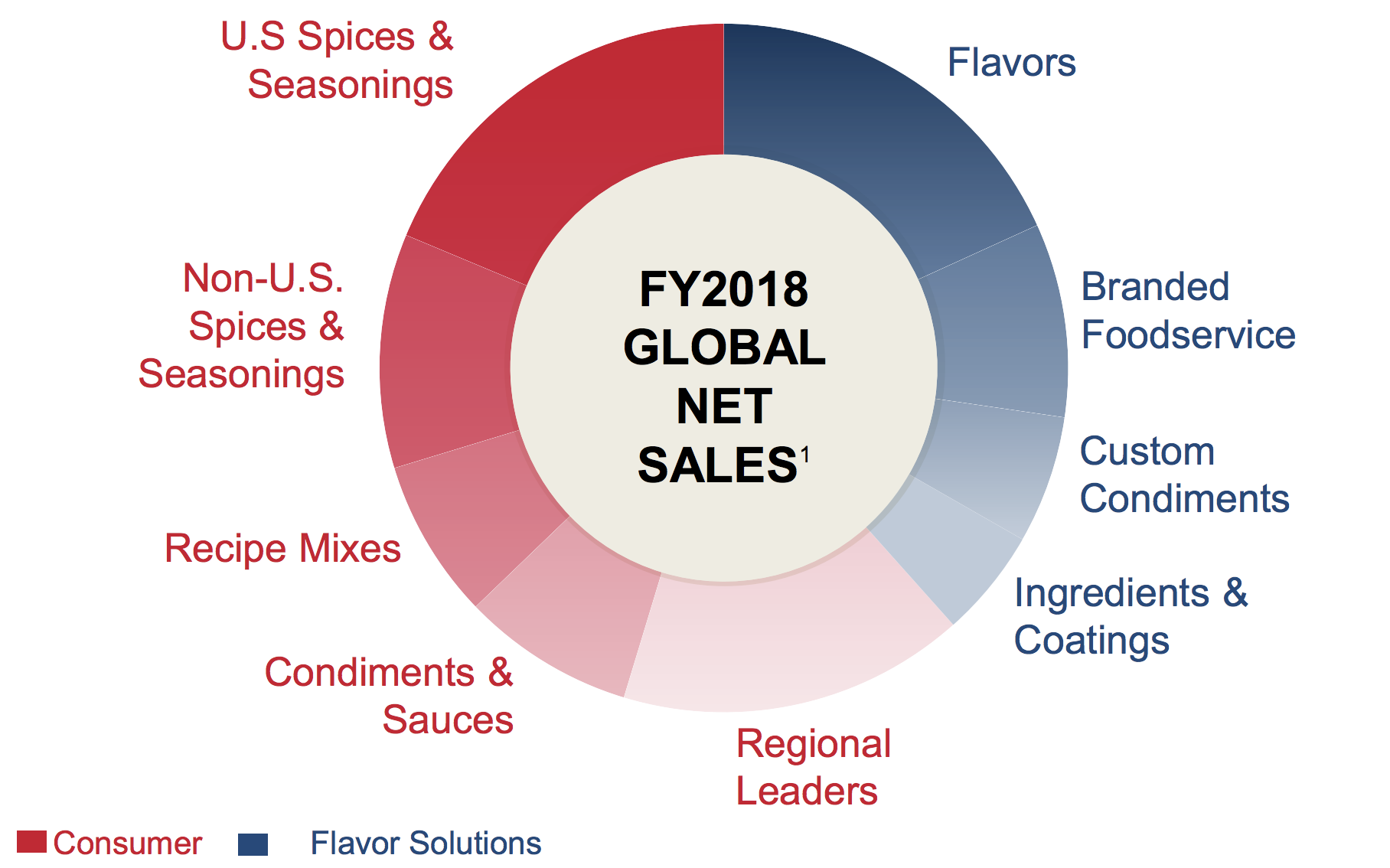

McCormick has two business segments – Consumer (61% of sales, 69% of operating income) and Flavor Solutions (39% of sales, 31% of operating income).

The Consumer business sells spice, herb and regional favorite brands to grocery stores, supercenters, discounters, convenience stores, and e-commerce players.

Flavor Solutions sells to each of the top 10 global packaged food and beverage companies and the top 10 foodservice restaurant chains. Its offerings include snack seasonings, sandwich sauces, and branded foodservice products.

Source: McCormick Investor Presentation

By geography, 69% of the company's sales are generated in the Americas, 19% from Europe, the Middle East, and Africa, and 12% from Asia Pacific. About 20% of sales are in developing markets.

McCormick is a dividend aristocrat that has paid dividends since 1925 and increased its payout every year since 1986.

Business Analysis McCormick’s long-term success has been driven by its strong portfolio of brands, continuous product innovation, marketing investments, and gradual expansion into new product categories and geographies.

The company’s history dates back to the 19th century, building up over 100 years worth of brand awareness and scale. Today McCormick is about four times the size of its next largest competitor, and the majority of the firm's consumer sales are from brands that have No. 1 market share positions in their categories.

McCormick's range of products is also one of the broadest in the industry and covers every price point ranging from premium to private label, helping the business stay relevant almost regardless of customers' changing preferences.

Coupled with the company's strengths in branding and product innovation, many of McCormick’s customer relationships have spanned decades. Breaking up these relationships to secure shelf space is no small feat for new entrants.

McCormick’s focus on innovation is also worth noting. Many of its products are prepared from confidential formulas developed by its research laboratories and product development teams.

For example, since 2000 McCormick has done a comprehensive annual flavor forecast, in which it brings together top chefs, culinary professionals, sensory scientists, dietitians, marketing experts and food technologists to keep abreast of changing consumer preferences in spices and its specialty food products.

This is why McCormick was one of the first packaged food companies to recognize the increasing trend in healthier foods, especially of the organic variety, and as a result over 75% of its premium consumer spices are now organic.

In addition, McCormick operates over 20 global technical innovation centers, where new products and flavors with maximal regional popularity are developed.

Meanwhile, the McCormick Science Institute funds numerous clinical trials at universities around the world to keep abreast of the latest scientific breakthroughs in the realm of nutrition, helping the firm stay ahead of its rivals in recognition of new dietary trends into which it can market its products.

Simply put, McCormick’s long-term investments help ensure it can stay at the cutting edge of spice and flavor science to continue meeting consumers' flavor and health demands.

Combined with the fact that most of its seasons and spices represent no more than 10% of a finished product's cost but drive 90% of its flavor, McCormick seems positioned to continue enjoying strong demand and pricing power.

In its Flavor Solutions segment, McCormick works closely with major food companies such as PepsiCo and McDonald’s. The firm's products help them create food and beverages that are aligned with the healthier eating trend without compromising taste.

In fact, the majority of product development projects for McCormick's U.S. Flavor Solutions customers includes health and wellness attributes like lowering sodium, artificial ingredients, or calories.

While consumers increasingly want healthier, more natural, and simpler food, they still desire appetizing tastes and flavors. As a result, the global flavor market is projected to grow 5% annually in the years ahead, according to McCormick.

Besides growing with the market, McCormick has made more than a dozen acquisitions over the last decade to expand its portfolio, strengthen its market position, and gain additional scale.

Management believes acquisitions will drive about a third of the firm's revenue growth going forward. When McCormick buys a business, it can often improve its distribution and performance thanks to the dedicated resources it provides.

For example, in 2017 McCormick made its largest acquisition ever, paying $4.2 billion to purchase Reckitt Benckiser's Food division. The deal added well-known condiment brands such as Frank’s RedHot sauces, French’s mustard and ketchup, and Cattleman’s BBQ sauce to McCormick's portfolio.

This business wasn't a core focus for Reckitt Benckiser, providing McCormick with plenty of low-hanging fruit to improve its shelf space, marketing, product line, and overall performance.

With almost an endless number of flavor categories, McCormick can continue building its global growth platforms through acquisitions over the years.

Coupled with McCormick's cost-cutting efforts, R&D, and marketing investments to protect its market share positions and customer relationships, management believes the company can achieve the following long-term goals:

4-6% annual sales growth

9-11% annual EPS growth

McCormick has historically met these goals, which represent some of the fastest growth rates of any consumer packaged goods company and have fueled about 10% annual dividend growth over time.

The company's future continues to look bright, but there are some potential challenges that could slow its pace of growth.

Key Risks Growing competition from private label and new brands is a key concern of most consumer packaged goods businesses. McCormick has demonstrated excellent pricing power over time, but this has also created a sizable gap in price between many of its spices and herbs and those sold under private labels.

The company does have its own private label line of products, but it is a small proportion of overall sales. McCormick's brand recognition and predictable tastes have helped the firm hold market share against lower-priced options, but the stock could lose its premium valuation multiple if its brands begin to experience weaker volume growth in mature food markets such as North America.

Many packaged food companies, especially those with a large presence in developed markets, have fallen on hard times recently. As consumer tastes and shopping habits evolve, organic, natural, and healthier products are taking more shelf space at virtually every retailer. Consumers are reading more labels and want to know what exactly they are putting in their bodies.

Fortunately, McCormick seems to face less risk than other players in this space because spices and herbs are not generally perceived to be health concerns with consumers. If anything, they are viewed as good ingredients to consume and can even serve as substitutes for sodium.

McCormick has also invested heavily to combat this risk. Over 70% of its McCormick brand spices, herbs, and extracts in the U.S. are non-GMO, for example. About 80% of its premium gourmet lines are organic as well, and the company continuously invests in its own proprietary flavor modulation technologies to meet "low" and "no" challenges without sacrificing flavor.

Another risk to consider is acquisitions. While McCormick has historically executed well on acquisitions, the 2017 Reckitt Benckiser deal was by far the company’s largest and significantly increased the firm's leverage ratio.

McCormick has so far delivered on its goals with this purchase, but future acquisitions always come with risks of overpaying and underdelivering on expected synergies. However, management deserves the benefit of the doubt based on their track record.

Finally, in the short term McCormick's results can be affected by foreign currency exchange rate fluctuations and volatile raw material costs. However, these issues seem unlikely to impact the firm's long-term earning power.

Closing Thoughts on McCormick Few companies have demonstrated the consistency that McCormick has over the last 100 years. The company’s dividend safety and long-term growth prospects are excellent, and the business should benefit over time from competing in slow-changing, steadily-growing markets.

While consumer tastes are changing, McCormick's well-managed brands and science-based focus on keeping up with the latest dietary and health trends help ensure that the business stays relevant.

McCormick's relatively low yield may knock it out of consideration for current income-focused portfolios, but the company's double-digit dividend growth potential makes it a solid candidate for longer-term investors.