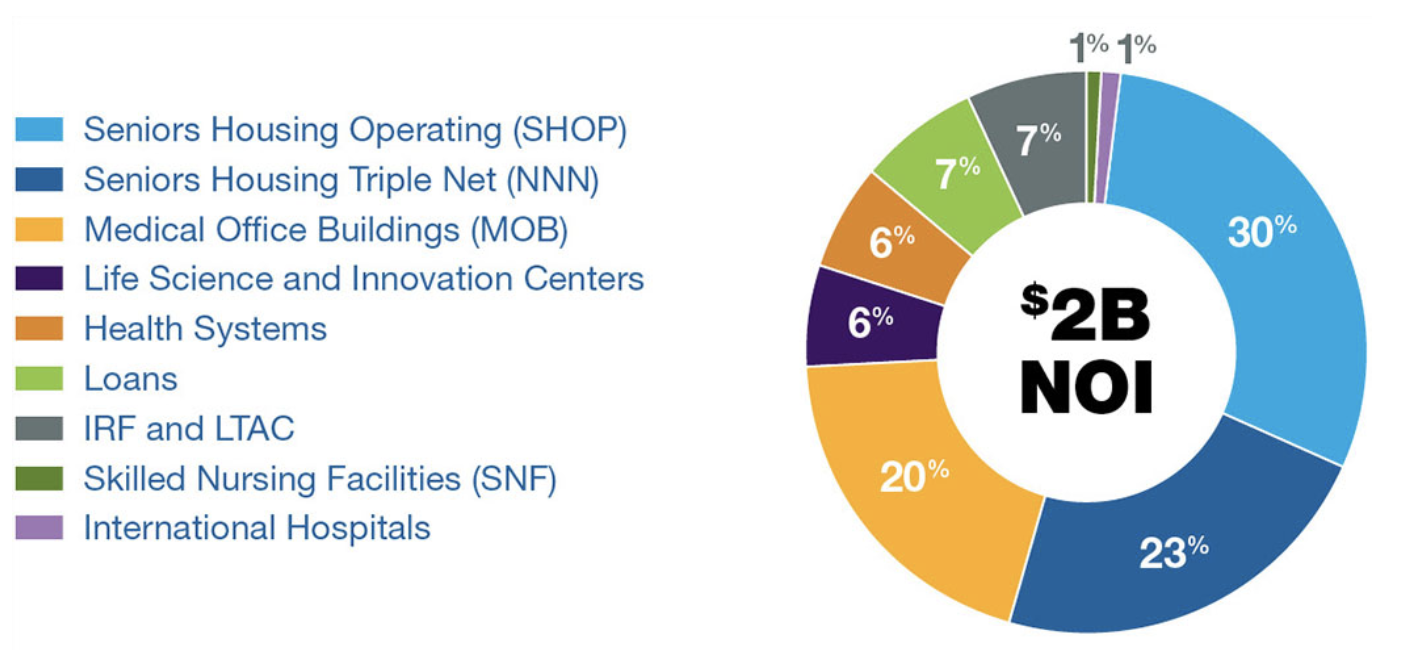

Ventas (VTR) was founded in 1983 and is the second largest medical REIT in the country, with more than 1,200 properties in the U.S. and the U.K. Ventas’ property portfolio consists primarily of seniors housing communities, medical office buildings, life science centers, and inpatient rehab and long-term acute care facilities.

The largest source of Ventas’ cash flow is derived from senior housing properties, which are run by third-party operators under a triple net lease arrangement (tenant pays all maintenance, taxes, and insurance), as well as by the company itself.

Over the past few years, Ventas has embarked on an aggressive portfolio evolution in which it’s been selling off assets in struggling industries (such as skilled nursing) and investing more heavily into medical offices, acute care centers, and life sciences buildings.

Business Analysis

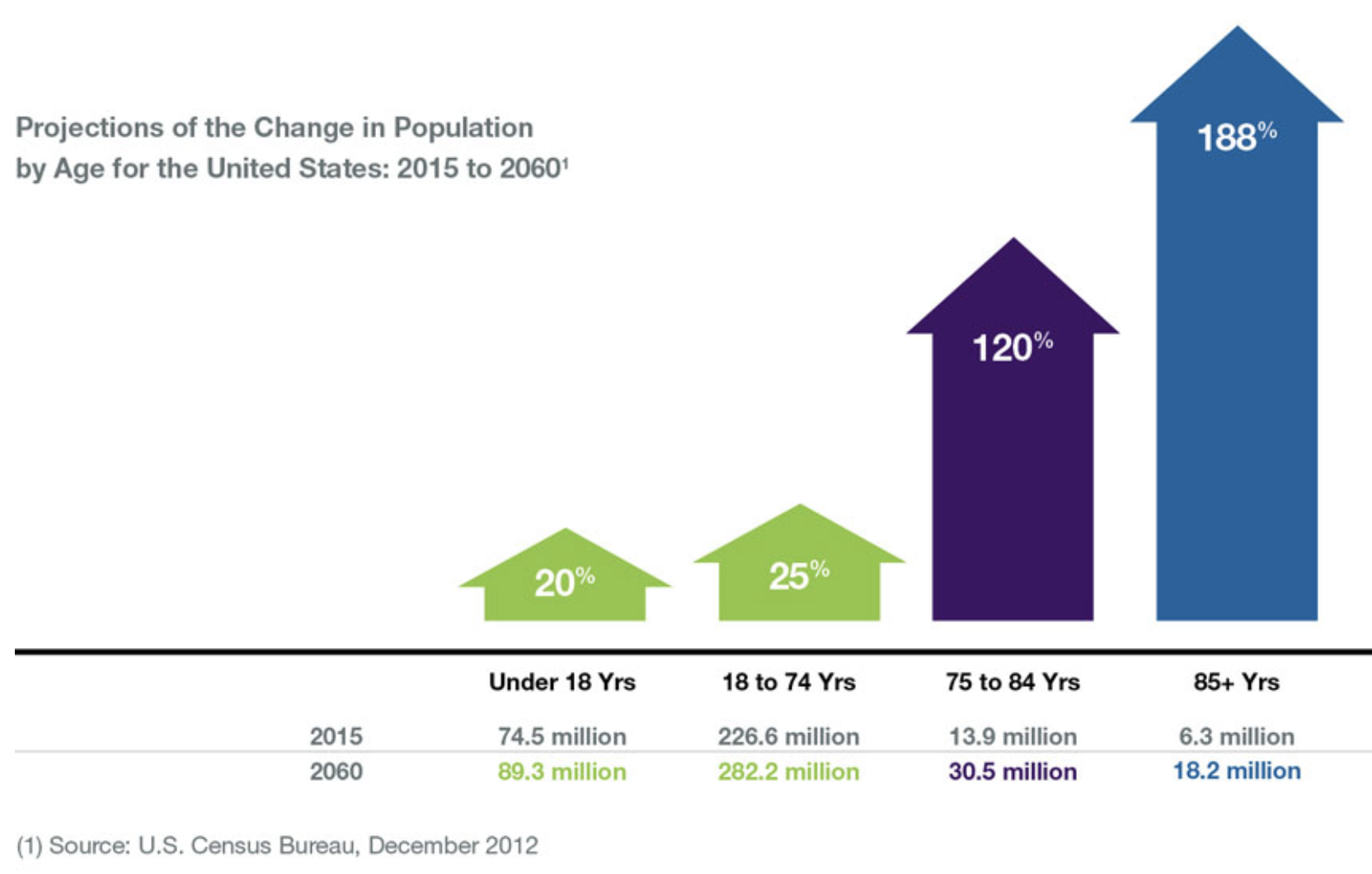

The underlying long-term investment thesis for almost any medical REIT is that strong demographic trends, including the rapid aging of the population, will greatly increase the need for medical services and medical properties over the coming decades.

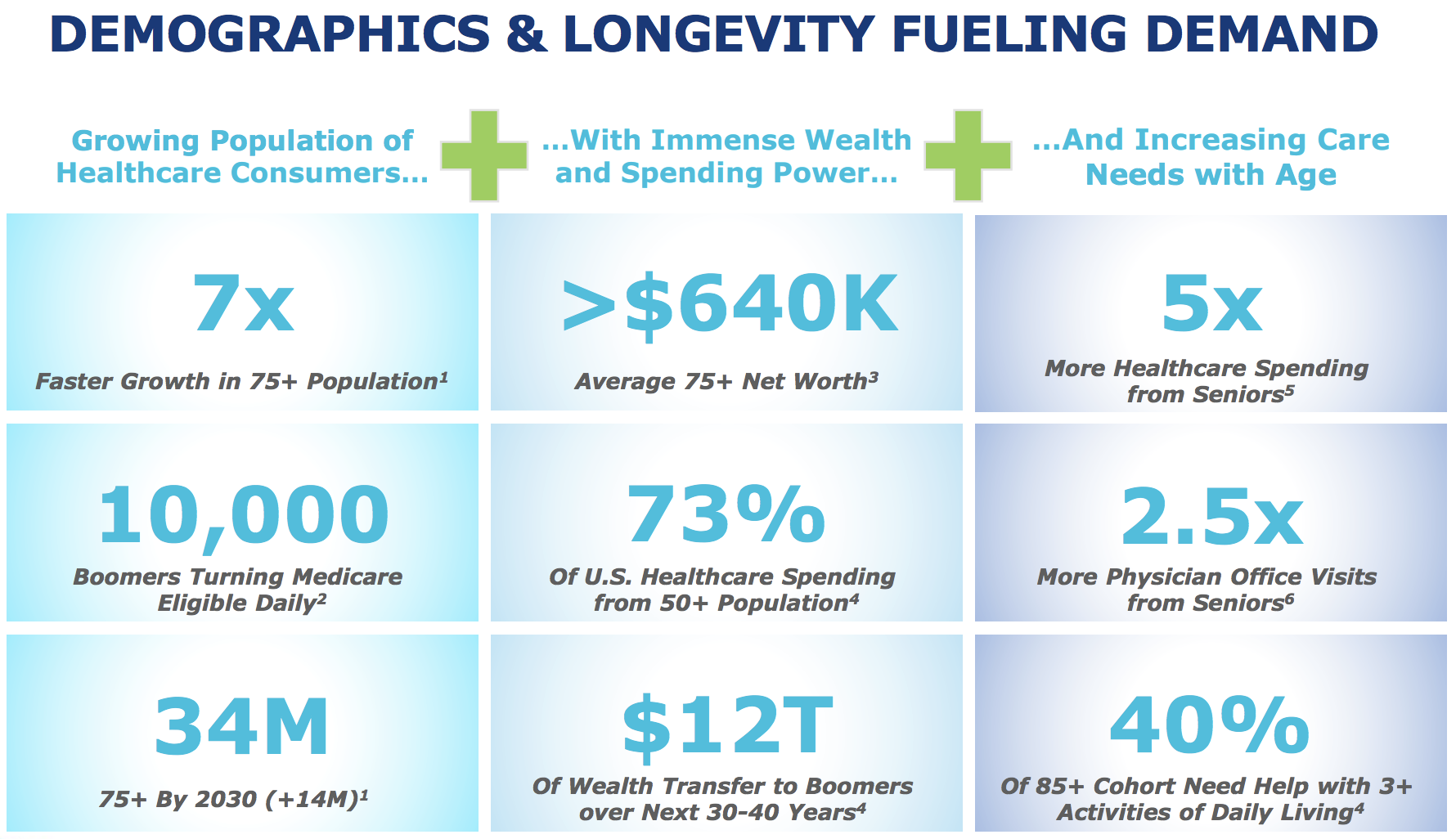

In fact, it’s estimated that U.S. spending on healthcare will rise by 5.8% a year between 2014 and 2024, resulting in healthcare accounting for 20% of U.S. GDP (from 18% in 2012).

Meanwhile, the seismic shift of an elderly population that’s growing seven times faster than the overall U.S. population and is the richest generation in history (on an aggregate basis) means there are major opportunities for medical REITs to consolidate this fragmented industry and fuel decades of growth.

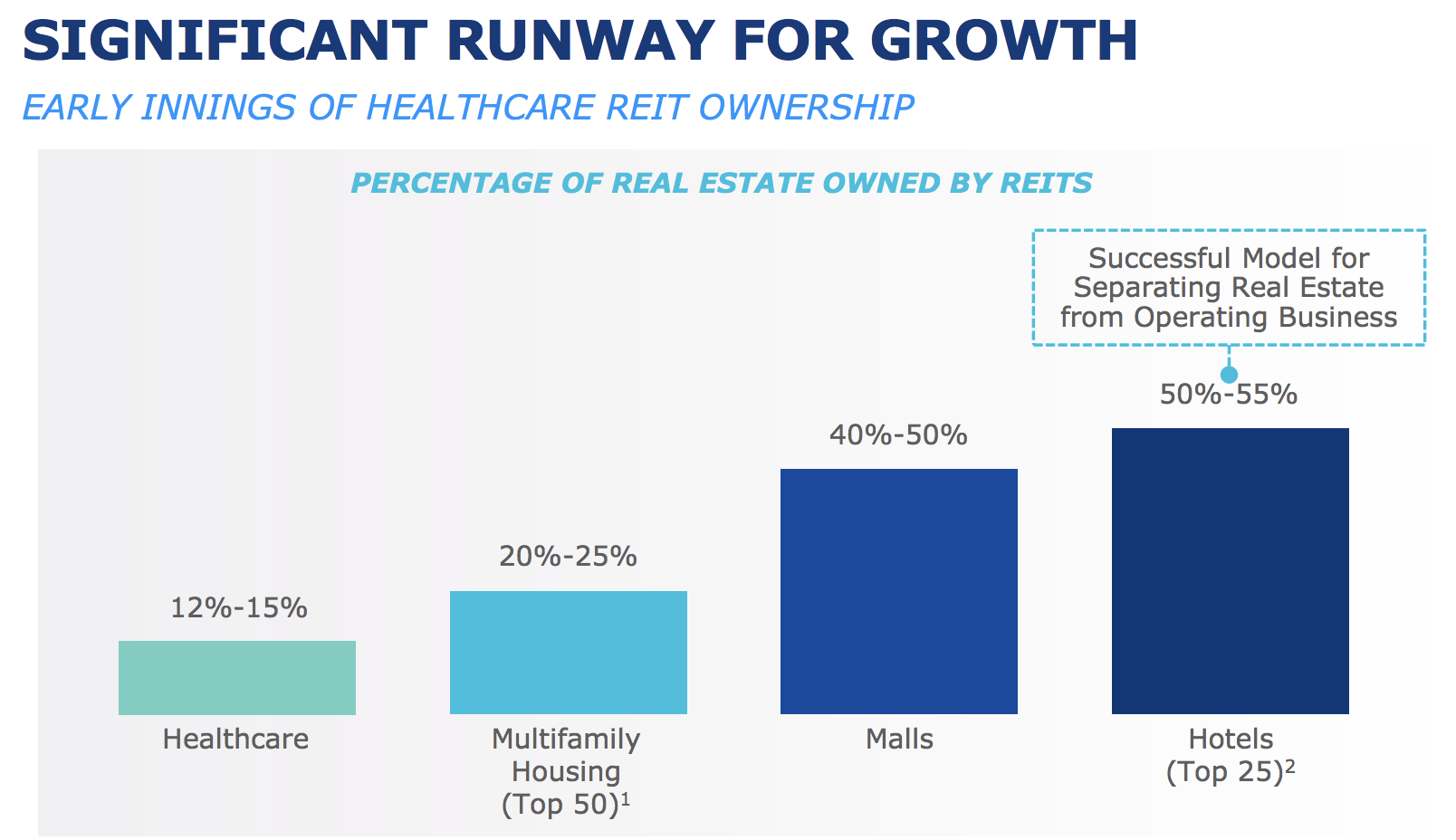

Consolidation is expected because it’s estimated that medical REITs currently own just 12% to 15% of the $1 trillion medical real estate market, suggesting that even industry giants such as Ventas have plenty of growth runway ahead of them.

Of course, just because an overall market is large and growing doesn’t mean that investors can just blindly invest in it. The key to what makes Ventas successful is the company’s exemplary management team, headed by longtime (since 1999) CEO Debra Cafaro.

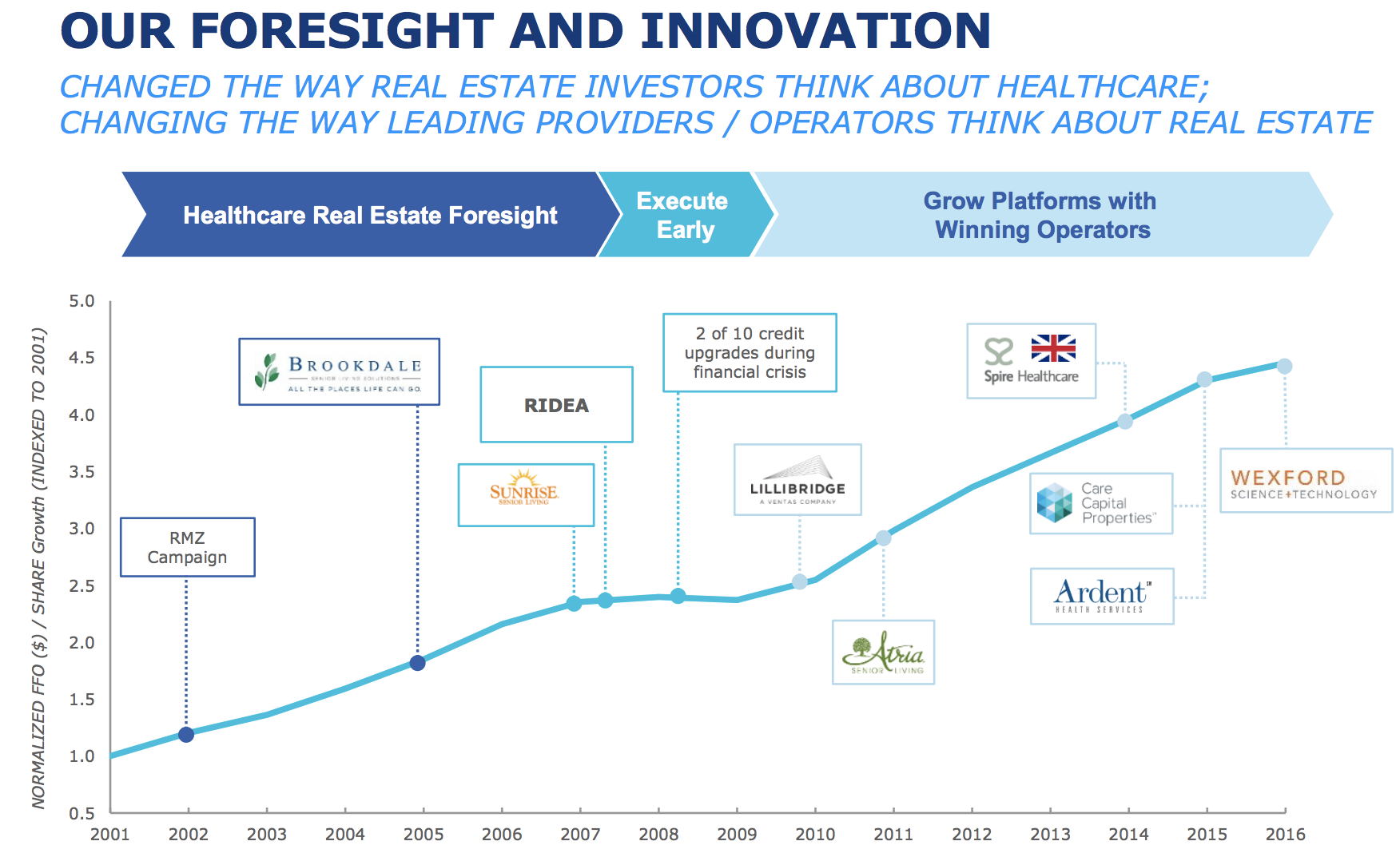

Mrs. Cafaro has led Ventas to not only steadily grow over time, but more importantly adapt to the rapidly-evolving medical industry through a series of well-timed strategic shifts in the company’s business model.

For example, Ventas was the first large medical REIT to take advantage of the 2007 REIT Investment Diversification and Empowerment Act (RIDEA) via its 2007 acquisition of SunRise Senior Living REIT.

Before RIDEA, the only way it was legal for REITs to own certain medical properties, such as skilled nursing facilities and senior housing, was under a triple net lease business model, which basically meant they were nothing more than landlords with no ability to share in any profits from rising occupancy rates or average revenue per occupied room (REVPOR).

After RIDEA, Ventas was able to aggressively enter the senior housing space and actually operate its own properties, most of which are located in the country’s largest and most affluent markets.

Next, Ventas broke into Medical Office Buildings (a $200+ billion market), which generally have far higher occupancies and more premium rents (due to their key locations on medical center campuses and near hospitals), via its $350 million acquisition of Lillibridge Healthcare Services and its 154 buildings in 2010.

In addition, Ventas was the first of the big three medical REITs (the others being Welltower and HCP) to start shifting out of the troubled skilled nursing facility industry, via its $4 billion spinoff of Care Capital Properties (CCP) in 2015.

More recently, the company also struck an agreement with Kindred Healthcare (KND), one of America’s largest skilled nursing facility operators, to sell 36 of its facilities in exchange for $700 million, which at a 7.3% cash yield represents a very good price (most facilities go for 8% to 9% cash yields).

Importantly, the CCP and Kindred exits also provided the REIT with the capital to further target far healthier and faster-growing markets, such as medical office buildings and life sciences properties.

For example, Ventas recently bought Ardent Health Services ($1.8 billion) and Wexford Life Science ($1.5 billion) in order to gain stronger exposure to acute care hospitals and medical research facilities, which can have occupancy rates as high as 97% and are rented out to the world’s leading medical research universities.

In fact, among its major peers Ventas has been the most aggressive in evolving its portfolio into medical office buildings and life sciences, with more than $7 billion invested over the last seven years.

A key reason why Ventas is able to more aggressively target these promising medical REIT industries is thanks to its low cost of capital. Specifically, Ventas maintains one of the strongest balance sheets of any REIT, which has provided the company with a top credit rating in the industry and allows it to access debt at very cheap levels.

When combined with its relatively low payout ratio (for a REIT), which results in more cash flow retained for the company, Ventas is able to pursue more accretive investments to grow its cash flow and dividend in all manner of economic and interest rate environments.

Overall, Ventas has a portfolio of diversified healthcare properties run mainly by best-in-class operators who should collectively benefit from favorable demographic trends over the coming decades. Management has shown capital allocation skill since Ventas went public in 1999, and the large and fragmented nature of the healthcare real estate market provides numerous opportunities for continued growth.

Key Risks

As impressive as Ventas’ growth has been, investors shouldn’t necessarily expect similar results going forward, even with the industry’s strong demographic tailwinds. Numerous risks are created by the highly volatile medical industry, which is going through some major growing pains.

For example, while the long-term aging of the U.S. population is certainly likely to generate strong growth in medical demand and spending in the coming decades, the brunt of this trend is still about five to ten years away, according to most projections.

In addition, the same strong growth in medical spending (which has grown at double the rate of inflation in recent decades) is making both government and private payers increasingly desperate to cut costs.

As a result, third-party operators, the triple net lease tenants that make up close to 40% of Ventas’ cash flow, are increasingly struggling from a combination of factors, including:

- Medicare and Medicaid reimbursement changes

- Rising labor costs

- Falling occupancy

Specifically, the Center For Medicare and Medicaid Services has instituted a series of long-term reforms designed to cut costs by moving away from pay-for-service and towards a more holistic, outcome-based model.

However, while this is a necessary long-term step to improve the quality and cost structure of U.S. medicine, it also means that skilled nursing facility operators are suffering, both from lower reimbursement, higher costs (labor and regulatory compliance), and declining cash flow/rent coverage ratios. Ventas has massively decreased its dependency to this industry in recent years, but it still has some exposure.

Meanwhile, the senior housing industry that makes up over half of Ventas’ cash flow is also experiencing challenges, though not anywhere near as bad as skilled nursing (largely because senior housing is mostly privately funded).

However, the issue for senior housing operators (Ventas’ triple net senior housing tenants) and its company-owned and operated facilities, is that a big increase in supply has swamped demand and resulted in depressed overall occupancy in recent years.

While U.S. Department of Health and Human Services estimates that ultimately 65% of older Americans will end up needing some form of long-term care (assisted living or nursing homes), this long-term trend also faces its own challenges for Ventas.

For one thing, senior housing is generally seen as a necessary evil, one that the vast majority of Americans want to avoid. For example, a recent Pew Research poll found that just 21% of seniors wanted to end up in senior or assisted living, with the vast majority wishing to remain at home or depend on family for medical care.

So while the future demographic wave may indeed ensure that the overall number of Americans in senior housing will increase, the fact that so many people are fundamentally (and understandably) opposed to ending up in these facilities means that demand growth might end up being slower than expected, potentially keeping occupancy rates lower for longer.

In addition, while Ventas’ portfolio reshuffling has reduced its dependence on government spending to just 6% of cash flow, that doesn’t mean it has eliminated all risks.

After all, assisted living is still very expensive. In fact, a 2014 Genworth Cost of Care survey found the median monthly cost of assisted living came to $3,500 a month, or $42,000 a year.

Meanwhile, retirement homes are even more expensive, with most homes charging $6,500 to $7,300 a month, depending on if its a semi-private or completely private room. The average nursing home stay is 42 months, meaning that total costs to consumers is over $270,000.

Most seniors cover these expenses via Medicaid, private insurance, or taking out home equity loans, or sometimes a reverse mortgage. However, Ventas has chosen to mostly forgo Medicaid-funded business and focus on private payers, which provides less uncertainty.

However, the issue is that the overall market for senior housing may end up being smaller than many people think, since assisted living/nursing home insurance is something that needs to be taken out years in advance before you need it. Unfortunately, a large proportion of aging Americans have probably not thought through how they plan to fund their potential long-term healthcare needs.

All of which means that, although the physical demand for senior housing may be very large in the coming decades, it’s far less certain how many individuals will actually be able to afford it.

Finally, there is issue of interest rates, which pose a challenge to some medical REITs more than others. REITs are highly capital intensive and are required to distribute at least 90% of their taxable income as dividends, making them dependent on capital markets to fund their growth.

One reason why rising interest rates are a headwind is that they increase the cost of debt. Fortunately, Ventas has proven itself capable of growing the business steadily in all types of environments, including when long-term rates were as high as 6.5%. Ventas also uses long-term, fixed rate loans to match up its capital needs with its long-term investment strategy, thus locking in guaranteed profitable growth.

In addition, in a higher rate environment, slow-growing, bondlike REITs become relatively less appealing income investments compared to risk-free securities, such as Treasuries. As a result, REITs can see their share prices decline (yields rise when prices fall) and their cost of equity capital rise (most REITs periodically issue new shares to raise capital), potentially denting their growth plans.

Due to the very long-term nature of their leases, which means higher risk of inflation overshooting annual rental escalators, medical REITs can be particularly sensitive to interest rates. Ventas is in great financial shape, so its growth opportunities and dividend safety seem very unlikely to change even if rates rise.

However, health care REITs such as Ventas could face many challenges in the future, as the entire medical industry experiences greater political and economic uncertainty in the face of growing demand from an aging population.

Closing Thoughts on Ventas

Ventas is arguably one of the safest dividend payers in the health care real estate sector thanks to its diversified property portfolio, strong balance sheet, defensive business mix, conservative management team, and focus on private payers rather than government funding.

However, keep in mind that due to the company’s ongoing portfolio reshuffling (e.g. selling off skilled nursing facilities), as well as some of the struggles in the competitive senior housing market, Ventas’ payout growth seems likely to be slower over the next few years.

The company still seems like a reasonable selection for a retirement portfolio, but investors should go in being fully aware of the industry’s risks and some of the growth headwinds they could pose.

To learn more about Ventas’ dividend safety and growth profile, please click here.

Leave A Comment