While only 46 stocks exist on our list of master limited partnerships (MLPs), these businesses are popular with income investors due to their high yields and generally stable cash flow.

However, MLPs are more complicated investments in part because of how their distributions are taxed.

Let’s take a look at the most important MLP tax issues to help you determine whether or not MLPs are right for your income portfolio.

Important Differences between MLPs and Regular Dividend Stocks

Unlike a regular dividend stock such as Johnson & Johnson, which is structured as a C-corp, MLPs (which legally must obtain at least 90% of income from natural resources such as oil, gas, timber, or the storage, transportation, or processing of these resources) are structured as pass-through entities.

This means means that they "pass through" most of their cash flow, as well as their tax obligations, to investors (who are termed unitholders instead of shareholders).

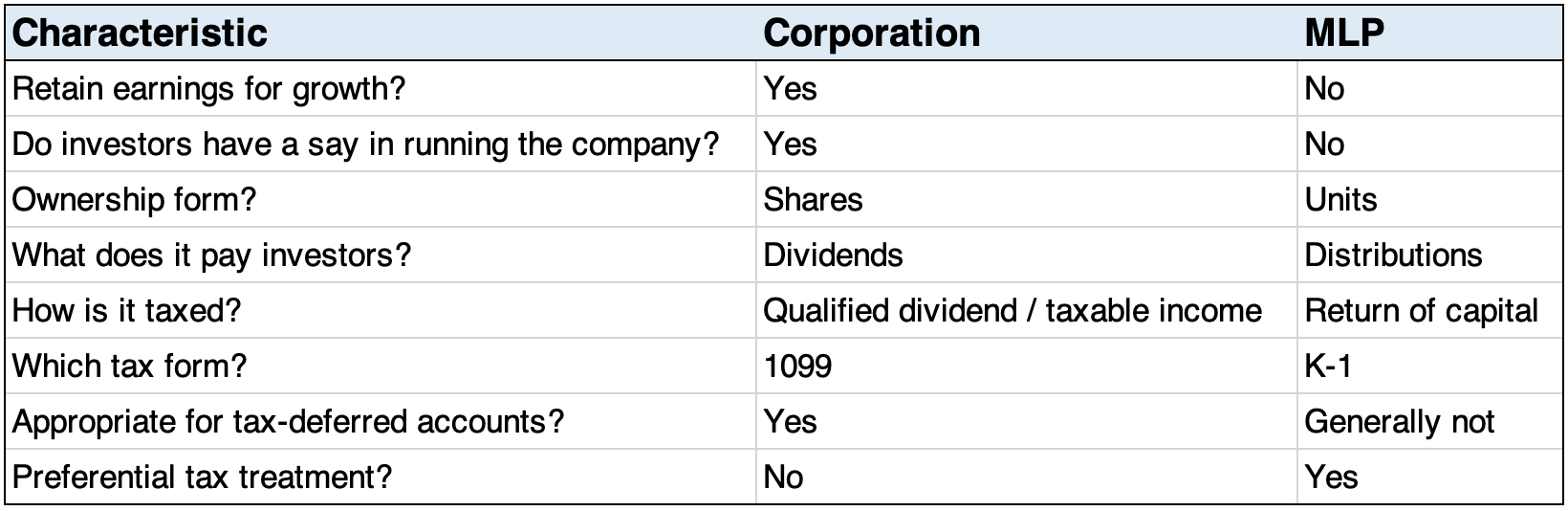

The chart below highlights the major differences between corporations and MLPs.

Source: Motley Fool, Simply Safe Dividends

Under the traditional MLP business model most MLPs don't have employees, but rather have management provided by their general partner or sponsor. The sponsor typically owns a 2% general partner stake in the business, a substantial amount of limited partnership units (what investors own), as well as the incentive distribution rights (IDRs).

IDRs create an incentive to grow the distribution quickly by selling ("dropping down") assets to the MLP to grow its cash flow and thus its payout. This is because IDRs entitle the sponsor to receive up to 50% of marginal distributions above a certain quarterly distribution threshold.

When combined with their general partner and limited partnership stakes, sponsors can frequently obtain the majority of cash flow from an MLP, while also recouping the cost of building or acquiring the assets from the MLP who raises external debt and equity capital to buy them.

In other words, from the perspective of the sponsor, MLPs are a tax-efficient method of monetizing natural resource-based assets (such as pipelines, and energy storage and processing terminals), while still benefiting from their stable cash flow.

From the perspective of individual investors, MLPs can be a source of substantial and growing income, underpinned by cash flow streams with minimal direct exposure to commodity prices.

However, due to low oil prices, regulatory changes, U.S. tax reform, and generally poor valuations across the industry, many MLPs have adapted their business models in recent years.

This has included simplifying their structure to either eliminate costly IDRs, convert to a corporation, acquire their GPs, or have the GP buy out the MLP. The pool of remaining MLPs continues to shrink.

The Tax Benefits of MLPs

Due to the way MLPs are structured, these entities usually don't pay corporate taxes. MLPs avoid the standard double taxation problem that regular C-corps have, in which the company pays tax on its net income that funds the dividend, and then investors have to pay their own tax on that dividend.

MLPs' tax benefit is due to the large amount of depreciation created by the capital-intensive nature of the industry. For example, pipelines can cost billions of dollars to build. Accelerated depreciation rules enable MLPs to expense many of their construction costs, reducing taxable income.

Additionally, when an MLP acquires assets or another MLP entirely, then it can step up the value of those assets to match its purchase price (including any premium paid). This further helps MLPs write off depreciation to reduce their profits.

Due to their high depreciation charges, an MLP's reported earnings are often depressed. Therefore, it is important to use distributable cash flow (similar to free cash flow for an MLP) to determine the safety of their distributions.

Under IRS rules, the majority of an MLP's distributions are considered a "return of capital" (ROC) because they exceed the MLP's earnings.

As a result, the IRS treats the distribution as if the company was simply taking the cash that investors gave the MLP (when it sold more shares to raise capital) back to them.

Rather than pay taxes on this ROC, this portion of the distribution is simply deducted from the investor’s cost basis. If an investor's cost basis eventually hits zero, then any future distributions are taxed as long-term capital gains.

Since the ROC distributions are caused by depreciation and other deductions taken by the MLP, those deductions are recaptured upon the sale of an investor's units and taxed as ordinary income. The remainder is taxed as a capital gain.

For example, suppose you bought an MLP at $10 per unit, and it paid out $1.00 in an annual distribution, 80 cents of which is classified as a ROC. That 80 cents per unit in distribution is not taxed, but rather deducted from your cost basis, which is now $10.00 – $0.80 = $9.20 per unit.

If you then sell the MLP at $11 per unit, the $1.80 per unit difference between your cost basis of $9.20 and your $11 selling price will result in ordinary income taxes on the 80 cents per unit of ROC and capital gains taxes on the $1 per unit of appreciation the MLP experienced since it was purchased.

Note that if your MLP gets bought out by a C-corp (as has occurred several times since the oil crash), then this is considered a taxable event and you must pay all deferred taxes you've accrued over your investment period.

What if you never sell your units? Eventually you might be able to reduce your cost basis to zero, at which point all future distributions get taxed at long-term capital gains rates (effectively like qualified dividends).

A substantial benefit to ROC is that when you die, your heirs can inherit your units (up to certain limits) tax-free. The cost basis steps up to the closing price on the day you died.

In this way, you can theoretically defer up to your cost basis in distribution taxes permanently, and your heirs can potentially inherit an income-producing portfolio of MLPs.

Note, however, that this mostly applies to older investors who have held MLPs for a long time. Since MLPs service the oil and gas industry, which could eventually see demand peak at some point over the decades ahead, the ability to "buy and hold forever" for tax purposes may not apply to younger investors whose investing horizons are longer than a few decades.

If MLP distributions were treated the same as other pass-through stocks (like REITs or BDCs), whose payouts are classified as non-qualified dividends, then investors would be taxed at their top marginal tax rates.

Thus MLPs, unlike other kinds of pass-through stocks, benefit from both deferred tax liability, as well as effectively being taxed at the same rate as qualified dividends such as those paid by C-corps.

Another benefit that MLPs offer in terms of tax advantages is due to a key provision in tax reform passed in 2017. Specifically, all pass-through stocks, including MLPs, now have a 20% pass-through deduction through the end of 2025 (after which it expires).

In other words, the first 20% of every distribution can be deducted from your taxes immediately. This lowers your proportional tax burden by 20% and can be claimed by anyone, whether or not you itemize your deductions and no matter how high or low your wages are.

Since tax reform about doubled the standard deduction, this means that most Americans won't be itemizing, yet will still benefit from this 20% pass-through deduction provision.

Tax Headaches from MLPs: Beware of the Tax Forms

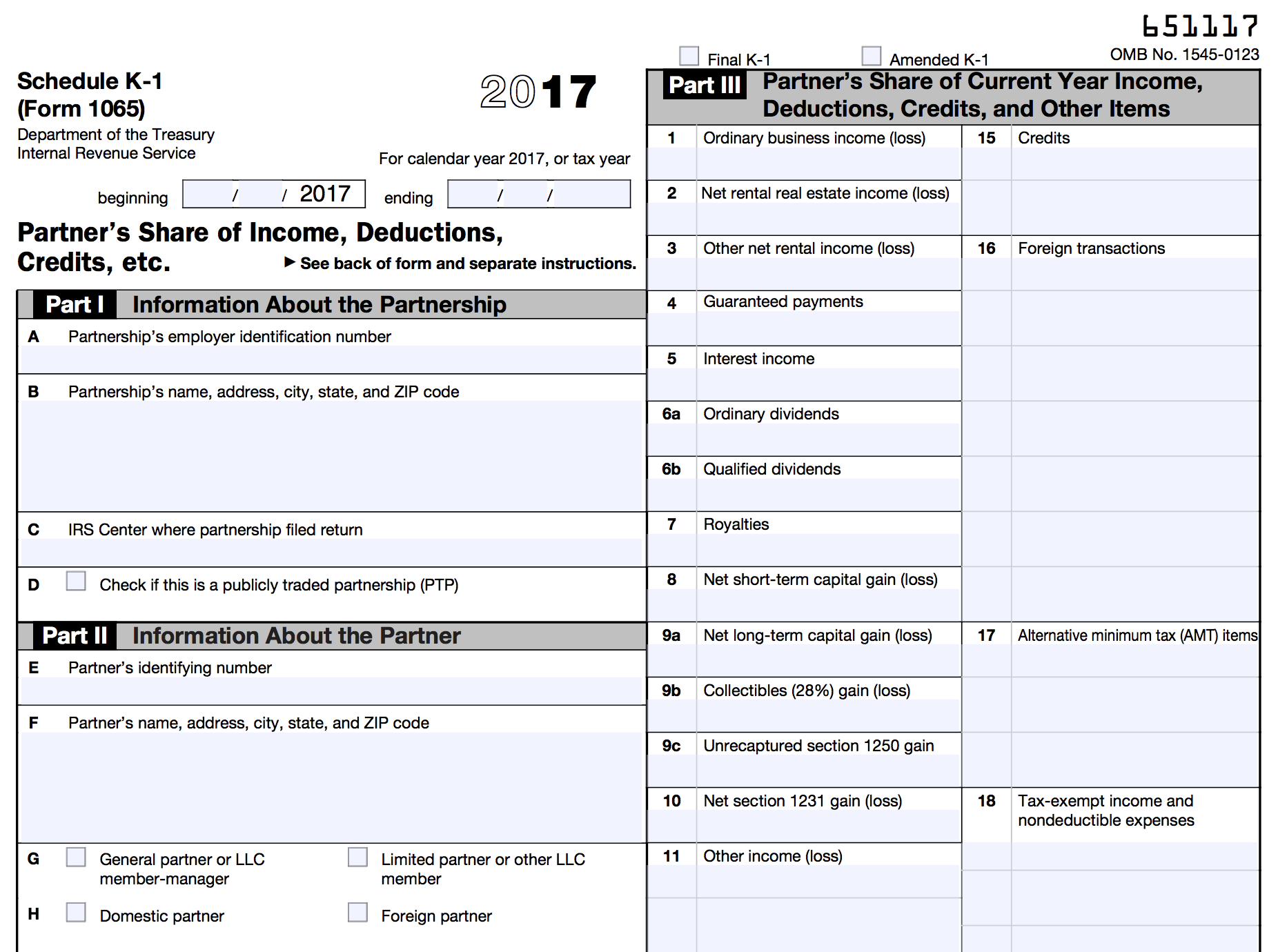

While MLPs have many tax benefits to like, there are trade-offs. The biggest one is arguably the Schedule K-1 MLPs send investors at tax time. This form is more complex than the standard 1099 form that C-corps issue.

Source: IRS

Fortunately, tax services such as Turbotax can usually handle K-1 forms in just a few minutes, and help to keep track of your cost basis and annual tax liabilities. If you use an accountant to prepare your taxes, having a lot of K-1s can result in a higher overall bill.

This is because an MLP’s distributions consist of income, ROC, and something called Unrelated Business Taxable Income. Each K-1 will be different, and the proportion of each component of its distributions vary from year to year.

In other words, a key downside of owning an MLP is higher complexity at tax time. In addition, there are important implications for owning MLPs in tax-advantaged accounts that have led most financial experts to advise owning these stocks in taxable accounts rather than IRAs or 401(k)s.

MLPs in Tax-Deferred Accounts: Why It Might Not Be A Good Idea

Many people look at the added tax complexity of MLPs and might think, “a tax advantaged account can help me avoid this mess.” While this is partially true, as the account custodian will aggregate and summarize all the MLP tax info in a 990-T form, there are two things to keep in mind before you purchase MLPs for your IRA or 401(k).

First, due to the significant amount of deferred tax benefits that come with owning MLPs, owning them in tax-deferred retirement accounts means you won't gain from this benefit.

That's because when you eventually withdraw funds from a retirement account, you will be taxed at your top marginal tax rate (except for Roth IRAs). Thus, the benefit of MLPs being effectively taxed at the same rate as qualified dividends (long-term capital gains rate) doesn't apply to tax-deferred accounts.

The other issue is unrelated business taxable income (UBTI). UBTI is basically any “gross income derived by any organization from any unrelated trade or business regularly carried on by it.”

UBTI was created by Congress in 1950 to ensure that any business that is structured as an MLP doesn't abuse its tax-exempt status to gain an unfair advantage over entities such as C-corps that do pay taxes. Simply put, if an MLP derives income from a business that is unrelated to its tax-exempt status, then it will generate UBTI.

If the amount of UBTI generated by all of your retirement portfolios exceeds $1,000 per year, then you must report it. In most cases, the plan custodian of your IRA or 401(k) is the taxpayer and needs to pay the tax by withdrawing money from your account’s funds. Some custodians charge high service fees for this task, reducing the appeal of MLP ownership.

While most MLPs generate negative UBTI most years, if there is a major asset sale or merger, then a substantial amount of UBTI can be generated and thus result in an unexpected tax liability.

So, while it may seem counterintuitive, owning MLPs in taxable accounts is generally the best way to minimize potential tax headaches.

Closing Thoughts on MLP Taxes

The more complex nature of MLP taxes should not necessarily deter you from including them as part of a well-diversified dividend portfolio.

MLPs' deferred tax benefits and the 20% pass-through deduction can make MLPs an attractive high-yield option for many investors.

Just don't forget that while most pass-through stocks (such as REITs and BDCs) are best owned in retirement accounts, MLPs are the exception and are usually best held in taxable ones. If you are ever in doubt about MLP taxes, consider consulting a certified tax professional.