In recent years the master limited partnership (MLP) business model has seen significant disruption, resulting in a multiyear bear market and numerous distribution cuts.

Slumping oil prices, regulatory changes, and U.S. tax reform have all pressured MLPs. Many of these firms are now simplifying their business structures in an effort to reduce their cost of capital and lessen their dependence on equity markets for growth financing.

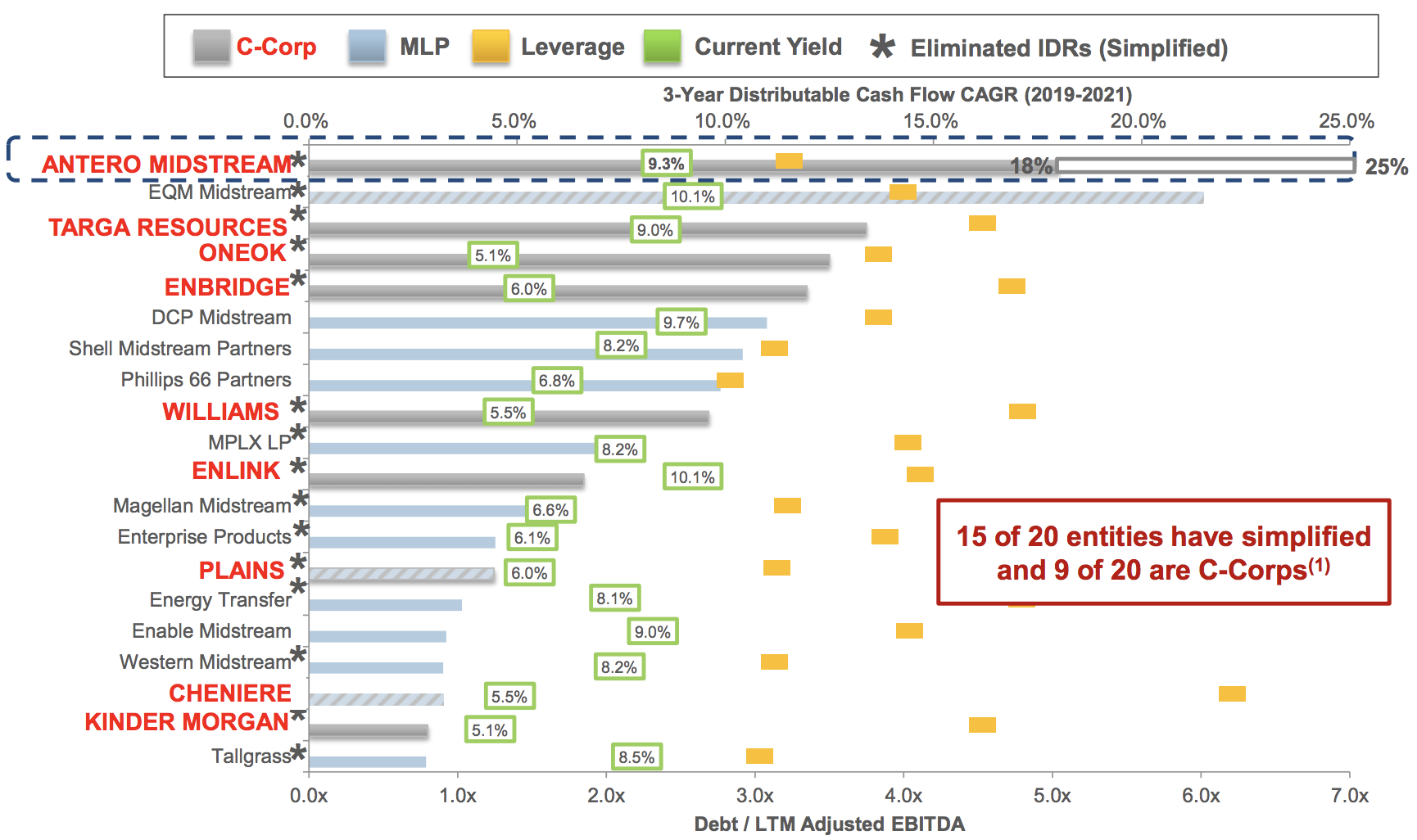

In fact, as of May 2019, 15 of the 20 largest midstream stocks by market cap have simplified their structures by eliminating their incentive distribution rights, and another nine of these stocks are now corporations.

While these changes are largely intended to make these businesses less risky and more attractive to a broader investor base, many MLP investors have been stuck with large tax bills as a result of these activities.

Source: Antero Midstream Investor Presentation

Most of the C-Corp conversions that have taken place resulted from corporate sponsors buying out their MLPs. These MLPs existed to buy midstream assets from their corporate sponsors, raising the proceeds primarily by issuing equity.

However, the crash in MLP unit prices no longer allowed this financing strategy to work, so many corporate sponsors opted to roll up their MLPs instead. Here are several examples:

Kinder Morgan: in August 2014 Kinder Morgan agreed to buy Kinder Morgan Energy Partners (KMP), Kinder Morgan Management (KMR), and El Paso Pipeline Partners, L.P. (EPB)

Enbridge: in May 2018 agreed to acquire its sponsored vehicles Spectra Energy Partners, LP (SEP), Enbridge Energy Partners, L.P. (EEP), and Enbridge Energy Management, L.L.C (EEQ)

Dominion Energy: rolled up Dominion Energy Midstream Partners, LP (DM) in November 2018

ONEOK: in June 2017 ONEOK acquired ONEOK Partners LP (OKS)

Williams: in May 2015 announced an agreement to acquire Williams Partners L.P. (WPZ)

Targa Resources Corp: acquired Targa Resources Partners LP (NGLS) in November 2015

Antero Midstream Corporation: in October 2018 AMGP agreed to acquire Antero Midstream Partners (AM) and then convert to a corporation

What if you were a unitholder of any of these MLPs which were acquired and converted into corporations? What tax consequences would you face?

While each transaction can be structured differently, including in ways designed to avoid taxes, unfortunately the vast majority of MLP conversions announced have been treated as a taxable sale for unitholders. The main exception is when two MLPs merge in an all-stock deal.

Upon closing of taxable merger tranactions, MLP unitholders will very likely owe taxes, and potentially a significant sum. To compute your taxable gain, you need to calculate the difference between the value of the proceeds you receive from the merger and your adjusted cost basis.

The value of the sale equals the merger consideration, or the market value of the shares you received in the corporate sponsor in exchange for your MLP units, plus any cash received. These transactions are usually all-stock deals.

As for your cost basis, remember that MLP distributions usually reduce your cost basis over time. That's because the majority of an MLP's distributions are considered a "return of capital" by the IRS.

Instead of paying taxes on distributions classified as a return of capital, these amounts are deducted from your cost basis. In other words, taxes on MLP distributions are deferred until you sell your units or the MLP is acquired.

If you hold your units long enough until your cost basis reaches zero, then future distributions are taxed as long-term capital gains. Some folks plan to hold their MLP units until death, when their heirs can inherit them tax free and step up the cost basis to the MLP's closing price on the day you died.

However, the lower your cost basis falls, the higher the taxable income you will report in the event of a merger or taxable conversion. All of the taxes you might have deferred over the years now come due, so taxable transactions especially hurt long-term investors whose cost bases are very low from many years of distributions.

Since distributions reduce your cost basis, it's also very possible to be on the hook for a taxable gain even if the MLP's acquisition price is well below the initial amount you paid for your units.

For example, suppose you initially paid $10 per unit and over the next few years received $4 per unit in distributions classified as a return of capital, reducing your adjusted cost basis to $6 per unit. If the MLP is rolled up at $7 per unit in a taxable transaction, then you would still have a taxable gain.

Making matters worse, a portion of your gain can also be taxed at ordinary income rates, which are higher than the rates for capital gains. This can result from stickier accounting issues such as depreciation recapture and unrealized receivables owned by the MLP.

It's also worth noting that reorganizations can create headaches for folks holding MLPs in retirement accounts such as IRAs due to issues with unrelated business taxable income (UBTI).

UBTI is any "income from a trade or business, regularly carried on, that is not substantially related to the charitable, educational, or other purpose that is the basis of the organization's exemption," according to the IRS.

Your retirement accounts can collectively generate up to $1,000 per year in total UBTI, but if they exceed that threshold, then they must report and pay taxes on it.

Most MLPs generate negative UBTI any given year, but mergers and reorganizations can trigger a substantial amount of UBTI and thus another unexpected tax liability.

Overall, the amount and character of gain recognized by unitholders in an MLP merger or conversion will vary depending on your particular situation, including the value of the stock and cash received from the corporate sponsor, your adjusted tax basis, and any suspended passive losses that may be available to you to help offset part of the merger-related gain.

When an MLP undergoes a simplification transaction like the ones listed above, the firm will usually direct unitholders to a unique page on Tax Package Support that helps them estimate their tax liability.

However, you probably won't be able to determine your actual taxable gain or loss until you receive your K-1 tax form in March of the year following the year in which the merger is completed.

The most important thing is to be prepared for a large tax bill. And since these simplification deals tend to be all-stock transactions, note that you won't receive cash proceeds when the merger closes. Instead, you might need to sell some of your new shares to raise enough cash to cover your tax bill.

If you hold through the merger or conversion and allow your units to be converted to new shares in the corporate sponsor, your holding period will reset beginning on the day the transaction closes. In taxable deals, your cost basis will also be stepped up to the current market value of your new shares.

Simplifications Aren't That Simple

Most reogranizations that have taken place have been taxable events for MLP unitholders. However, there are numerous ways of handling the conversion of a partnership into a corporation.

For example, in 2018 private equity firm KKR (KKR) converted from a partnership to a corporation in a tax-free transaction for U.S. federal and state income tax purposes. In this case, unitholders generally carried over their original tax basis in the shares of stock received in the conversion. Viper Energy Partners LP (VNOM), an owner of oil and natural gas properties, provided another example of the different paths firms can take when it elected to be taxed as a corporation rather than as a pass-through partnership in 2018. This was not taxable to Viper's unitholders and the firm's business model did not change, but it allowed Viper to rid itself of issuing K-1 tax forms.

Simply put, corporate conversions can come in various shapes and sizes. Any simplification transaction could be a taxable or non-taxable event. Therefore, it's difficult to predict how future potential conversions could play out and ultimately impact an investor's net return.

But if conversions and even mergers can be structured in tax-free transactions, then why are so many MLPs opting to create taxable events? Ironically, while most individual unitholders are stuck with tax bills, the corporate sponsor can reap meaningful tax benefits going forward.

In a taxable roll-up transaction of an MLP, the corporate sponsor steps up all of the MLP's assets and liabilities to their fair value (rather than keeping the original cost they were recorded at on the books).

The stepped-up tax basis of an MLP's assets allows the corporate sponsor to record much larger depreciation and amortization charges going forward, reducing the amount of taxable income it reports and thus boosting its after-tax cash flow.

MLP Conversions Can Result in Dividend Cuts

Besides hairy tax consequences, MLP roll-ups, in which MLP investors swap their units for common stock in the corporate sponsor, can lead to dividend cuts.

That's because MLPs generally have much higher yields than their general partners. So when a general partner (often a corporation) buys its MLPs, even accounting for the conversion ratio (ratio of shares received per MLP unit owned) the effective yield on the new shares owned by midstream investors can fall.

This even applies for some MLP mergers. For example, Energy Transfer Equity (an MLP) acquired Energy Transfer Partners (one of its MLPs) in an all-stock deal. Since all-MLP mergers are usually not taxable events this didn't have any negative tax implications for Energy Transfer Partners investors.

However, even with the conversion ratio of 1.28 Energy Transfer Equity units per 1 unit of Energy Transfer Partners (MLP has changed its name to Energy Transfer LP, under the ticker ET), Energy Transfer Partner investors still saw an effective 31% decrease in their total distributions. And that's after the 2016 merger of Sunoco Logistics Partners and Energy Transfer Partners, which resulted in a 26% payout cut.

The good news is that not all MLP simplifications lead to such distribution cuts. For example, MPLX bought out Marathon Petroleum's (MPC) incentive distribution rights without cutting its distribution, and both Tallgrass Energy Partners (now TGE) and Antero Midstream Partners (AM) were bought by their general partners in corporate conversions structured in a way that actually increased their payouts.

However, the point is that any simplification can potentially pose the risk of significant tax consequences and a distribution cut. Even incentive distribution rights buyouts are usually all-stock deals that dilute investors, lower the distribution coverage ratio, and thus require slower payout growth in the future.

Uncertainties surrounding simplification transactions (around half of publicly-traded MLPs have now simplified in some form) continue to serve as a major overhang for the industry.

Conservative income investors interested in this space should remain focused on firm's that have already simplified their business structures (eliminated incentive distribution rights, implemented a self-funding model, reduced leverage, etc.), maintain quality contract profiles, and have large customer bases. Enterprise Products Partners and Magellan Midstream Partners are two examples.