Special Dividend Definition, Rules, and Impact on Stock Price

There are numerous reasons to embrace dividend growth investing as the best means to achieving long-term financial independence.

Most discussion focuses on traditional income stocks, those that pay out steadily growing quarterly dividends.

However, occasionally a company will issue a special dividend, which is generally much larger than a regular dividend and therefore tempting for yield chasers.

As you might suspect, special dividends don’t necessarily benefit investors nearly as much as regular dividends.

Let’s take a closer look at what a special dividend is, how special dividends impact a stock’s price, taxes on special dividends, and everything in between that you need to know.

What are Special Dividends and Why Do Some Companies Pay Them?

Generally, you can think of a special dividend as a one-time “gift” from a company thanks to the company’s earnings booming and cash piling up on the balance sheet.

A great example of this was Microsoft’s (MSFT) 2004 special dividend of $3 per share, or $32 billion.

However, as with most things on Wall Street, special dividends are often more complicated than they initially appear.

Unlike most quarterly dividends, which are paid regularly and at pre-determined amounts, special dividends are typically announced with little to no warning and with unpredictable amounts.

Companies might pay a special dividend for several reasons.

For example, companies that sell off large assets as part of a corporate restructuring often pay a one-time special dividend.

In 2017 the utility National Grid (NGG) announced a large special dividend to coincide with the sale of 61% of its U.K. gas distribution business for $17.2 billion, for example.

The company plans to pay out 75% of this cash as two special dividends that will, at least for 2017, result in National Grid’s effective yield spiking to close to 16%.

Another reason for paying a special dividend is due to strong but non-recurring capital gains or cyclical earnings.

For example, Main Street Capital (MAIN), a business development company, has been paying out a semi-regular special dividend of 55 cents per year every year since 2013.

This dividend is funded not by its distributable net interest income (DNII), but the capital gains on the equity stakes in the companies it lends to.

The reason that Main Street labels this a “special dividend,” despite the fact that management believes it will be able to continue paying it for the foreseeable future, is so that investors don’t get confused about the sustainability of its regular monthly payout.

For example, Main Street’s regular dividend has a payout ratio between 90% and 100%, which for a BDC is considered reasonably safe.

However, if you include the special dividend, then the firm's payout ratio rises to well over 100%. As a result, investors might worry that the monthly dividend might be at risk.

Similarly, companies in highly cyclical industries such as Ford (F) also utilize special dividends as part of hybrid payout plans.

Specifically, Ford’s dividend policy is to pay out a quarterly dividend of 15 cents per share and then issue an annual special dividend in order to achieve a dividend payout of 40% to 50% of adjusted EPS.

Management’s reason for this hybrid payout strategy is that automotive earnings are highly cyclical, coming in booms and busts.

Management has determined, however, that Ford should be able to maintain a secure 60 cents per share annual payout during the next industry downturn, even if it were harsher than the Great Recession of 2008.

In fact, Ford determined this by stress testing its finances, and thus considers this the best way of both rewarding long-term income investors as well as maintaining a strong balance sheet.

With this capital allocation plan, Ford can hopefully maintain enough financial flexibility to remain competitive in this highly capital intensive industry.

Finally, we can’t forget about tax policy. Often times a company will try to take advantage of an expiring lower dividend tax rate by issuing a special dividend, as we saw in 2012 when qualified dividends were taxed at just 15%.

Uncertainty over whether or not the expiring Bush tax cuts would result in dividends becoming taxed as regular income (top marginal tax rate), leading to a record amount of special dividends across corporate America that year.

Special Dividend Taxes

Unlike most regular dividends, which are taxed as qualified dividends (and thus as long-term capital gains), special dividends can be made up of a mixture of capital gains, ordinary income, and returns of capital.

The exact breakdown of the special dividend is spelled out in the 1099-DIV form sent to you by the company at tax time, but in general most special dividends are treated as returns of capital.

Rather than paying taxes on dividends classified as a return of capital, you lower the cost basis of your shares and only get taxed when you sell them.

However, this aspect of special dividend taxes also means that special dividends held in tax-deferred accounts, such as IRAs or 401(k)s, will miss out on the tax benefit.

That’s because any money withdrawn from these accounts after the age of 59.5 will be taxed as ordinary income.

Special Dividend Rules

The usual rules about holding periods don’t necessarily apply to special dividends.

For example, with normal dividends the company will issue three dates: the ex-dividend date, the record date, and the pay date.

This means that anyone who is a shareholder of record (i.e. your broker’s clearing house has a record of you owning shares) will get the dividend on the pay date.

The ex-dividend date is the first day that you won’t get the dividend if you purchase shares that day.

In other words, in order to get the most recently announced regular dividend, you must purchase shares the day before the ex-div date.

Special Dividend Impact on Stock Price

In theory, a company’s stock price will automatically fall by the special dividend amount on the ex-dividend date because the company’s distribution of this cash represents a decrease in the value of the company.

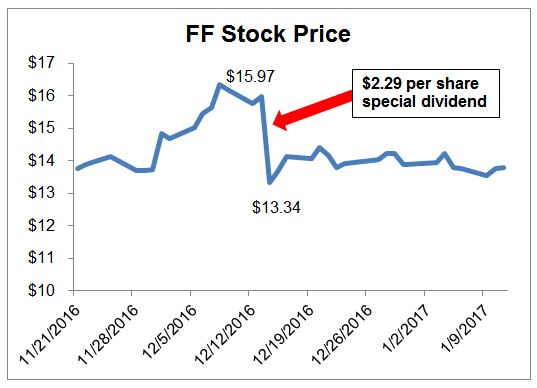

Take a look at FutureFuel, for example. FutureFuel (FF) declared a special dividend of $2.29 per share at the end of 2016.

Immediately before FutureFuel’s ex-dividend date, its stock price was $15.97 per share. Then, the company’s stock price immediately dropped to $13.34 per share, a decrease of $2.63 (somewhat more than the special dividend amount).

Source: Simply Safe Dividends

If you had purchased shares of FutureFuel prior to the ex-dividend date just to get the special dividend, the market value of your investment would have actually dropped by slightly more than the special dividend you received!

You never know how a stock's price will respond to a special dividend, making this dividend capture strategy a risky one to pursue.

Now here’s where special dividends differ from regular dividends. Since special dividends can be very large (sometimes as much as 25% to 30% of a company’s share price), stock markets need to avoid having a share price collapse by that much, which could trigger stop loss orders or margin calls.

Thus markets will adjust a company’s dividend dates with a “due bill” document. This represents a promissory note whose new ex-dividend date is set by the exchange, via its own complicated rules (not the dividend-paying company’s), which are designed to minimize the potential disruption caused by special dividends.

Basically what this means is that the exact dates at which you need to buy and sell a dividend stock in order to “capture” the special dividend can be complicated and different than the ex-dividend date stated in a company’s press release.

That’s just one of the main reasons why this strategy, of specifically buying a stock just to get the special dividend, is a poor one.

Don’t Chase Special Dividends

When a company announces a large special dividend, many investors are initially drawn to the idea of buying shares to get the special payment.

However, this strategy, a derivative of the regular dividend capture idea, is usually not a good idea.

That’s because after the bill due ex-dividend date, the share price will almost always decrease by the special dividend amount. In other words, from a total return perspective you gain nothing from a special dividend, as the total value of your investment is unchanged (you collect the dividend, but the price of your investment decreases by an equal amount).

In addition, you need to remember that a special dividend represents a return of capital to investors, meaning the cash paid out will no longer be available to grow the business.

This also applies to regular dividend stocks. However, the difference is that a regular dividend, especially one that grows along with a company’s earnings and free cash flow, is a sustainable, long-term way of boosting shareholder value.

That’s because historically around 40% of the stock market’s gains have come from dividends, including dividend reinvestment.

In fact, studies have shown that the long-term total returns of steady dividend growers, such as dividend achievers, aristocrats, and kings, generally follows the formula dividend yield + earnings growth.

This makes intuitive sense because over time a high quality dividend stock will have a stable payout ratio and yield.

For example, say a company grows its earnings by 7.2% per year for a decade. That will lead to earnings doubling over that time period, and the share price will naturally rise as investors are attracted to the company’s growing profits.

However, a special dividend has no long-term benefit, specifically because it is a one-time event. This makes intuitive sense because the intrinsic value of a stock is the future discounted cash flow the company can be expected to generate.

So a major special dividend, even one that represents a one-time 30% yield, won’t raise the long-term value of a stock.

This is why special dividends, except for rare exceptions such as in the case of Main Street Capital or Ford, are often a bad idea.

The only reason that those companies’ special dividend policies are ideal for long-term shareholders is because these special dividends are regular; they can be extrapolated out into the future to a degree and thus discounted to a present fair value.

On the other hand, take the example of National Grid, which sold off a major and steady cash flow asset to pay its special dividend. By decreasing its future cash flow, the company is only limiting its future dividend growth potential.

But what if a company is simply piling up so much cash on its balance sheet that it can’t possibly spend it all? Apple (AAPL) has over $200 billion in cash and cash equivalents and generates annual free cash flow of over $50 billion, for example. The company could pay a substantial special dividend if it wanted to.

However, Apple instead announced a $100 billion buyback authorization and has continued to raise its regular dividend at a fast pace.

Consistent buybacks of undervalued shares provide a great, permanent way to boost long-term earnings per share and help keep the payout ratio low.

Not only does that help to maintain a highly secure dividend, but it also allows the company to maintain a faster payout growth rate for longer.

This approach creates far more incentive for income investors to buy its shares and drive solid long-term total returns.

Where to Find Special Dividends

Generally I don’t recommend hunting for companies just because they pay special dividends.

Rather, it’s best to stick with high-quality dividend growth stocks that have occasionally paid out a special dividend every now and then.

This includes T. Rowe Price (TROW), Lazard (LAZ), Costco (COST), Franklin Resources (BEN), Main Street Capital (MAIN), and Cracker Barrel (CBRL).

Just remember to always do your research to make sure that you are only investing in a company for the long-term and one that fits your own unique risk tolerances, time horizon, and financial goals – not in hopes of a special dividend.

As for news about special dividends, Barron’s is a good source for this kind of news and doesn’t require a paid subscription unlike most other sites that track such information.

Closing Thoughts on Special Dividends

While special dividends aren’t necessarily bad, at the same time there is no evidence that they provide any long-term benefit to investors.

In effect, they are neutral and sometimes can actually be negative, especially if they result in slower long-term earnings and dividend growth.

Thus, investors would be wise to avoid the temptation to “chase” special dividend announcements.

Due to the fact that the share price should fall by the exact same amount, and that the company will lose the financial flexibility of that cash, the best strategy for dealing with special dividend announcements is the same as most Wall Street news: do nothing.

Stick with a buy, hold, add on dips, and reinvest the dividend strategy for companies with a solid track record of consistent regular dividend growth.