Closed-end funds can provide dividend investors with significantly more income compared to basic mutual funds, ETFs, and common stocks.

However, closed-end funds are not well-known by most investors and come with several complexities that need to be understood.

A closed-end fund is a type of investment company whose shares are traded on a stock exchange or in the over-the-counter market. Its assets are actively managed by the fund’s portfolio managers and may be invested in equities, bonds, and other securities.

However, closed-end funds have several important differences compared to the mutual funds you are likely more familiar with, which are known as open-end funds.

What are the Differences between Closed-End Funds and Open-End Funds?

There are two types of mutual funds – closed-end funds and open-end funds. When most people discuss mutual funds, they are referring to open-end funds, such as the Vanguard Dividend Growth Fund (VDIGX).

However, closed-end funds are very popular with income investors because they offer higher dividend yields (made possible with financial leverage and generous distribution policies) and distribute regular payments.

Unlike open-end funds, which issue and redeem shares to meet investor demand, closed-end funds have a fixed number of shares outstanding.

Since they do not need to manage inflows and outflows of assets, closed-end funds can remain fully invested to help generate more income or pursue less liquid areas of the market (e.g. micro cap stocks). The majority of them also use leverage to increase the amount of income they generate.

Open-end funds and closed-end funds are also priced very differently. Open-end funds trade at a price that is calculated by dividing the market value of their assets by the number of shares held by investors. They are traded at the end of the day.

On the other hand, closed-end funds trade at prices determined by supply and demand forces in the market and can be bought at will. This results in closed-end funds trading at a discount or premium to the market value of their assets.

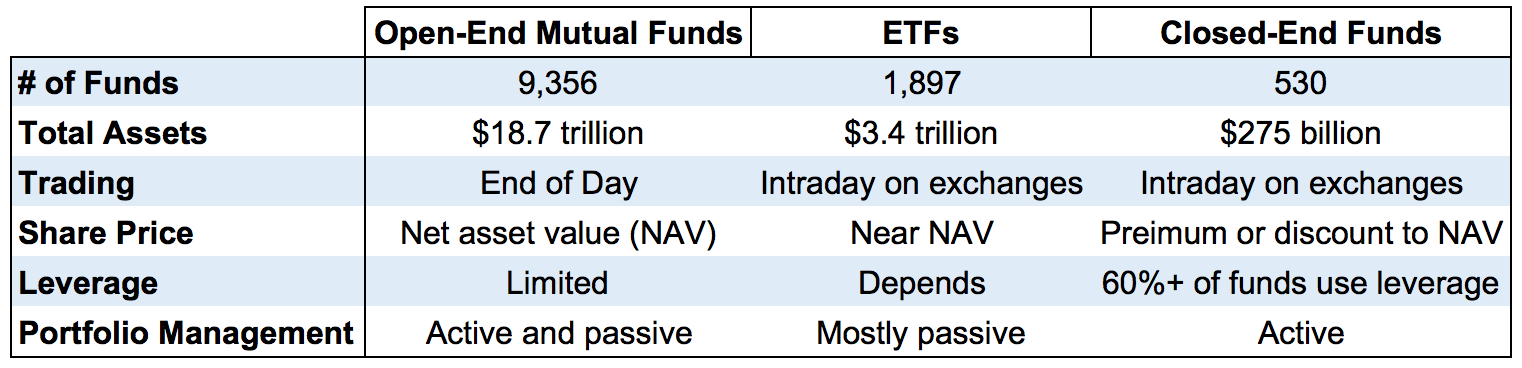

The following table highlights the key differences between closed-end funds, open-end funds, and ETFs.

Source: 2018 Investment Company Fact Book - as of 12/31/17

Generally speaking, investing in closed-end funds offers much higher income potential but can result in significant price volatility, lower total returns, less predictable dividend growth, and the potential for more surprises.

A long investment time horizon, stomach for price fluctuations, and diversified retirement portfolio are best to possess before even beginning to learn about closed-end funds, which are generally more appropriate for relatively sophisticated and risk tolerant dividend investors.

Let’s take a closer look at the key facts you need to be aware of before considering closed-end funds for part of your income portfolio.

Types of Closed-End Funds

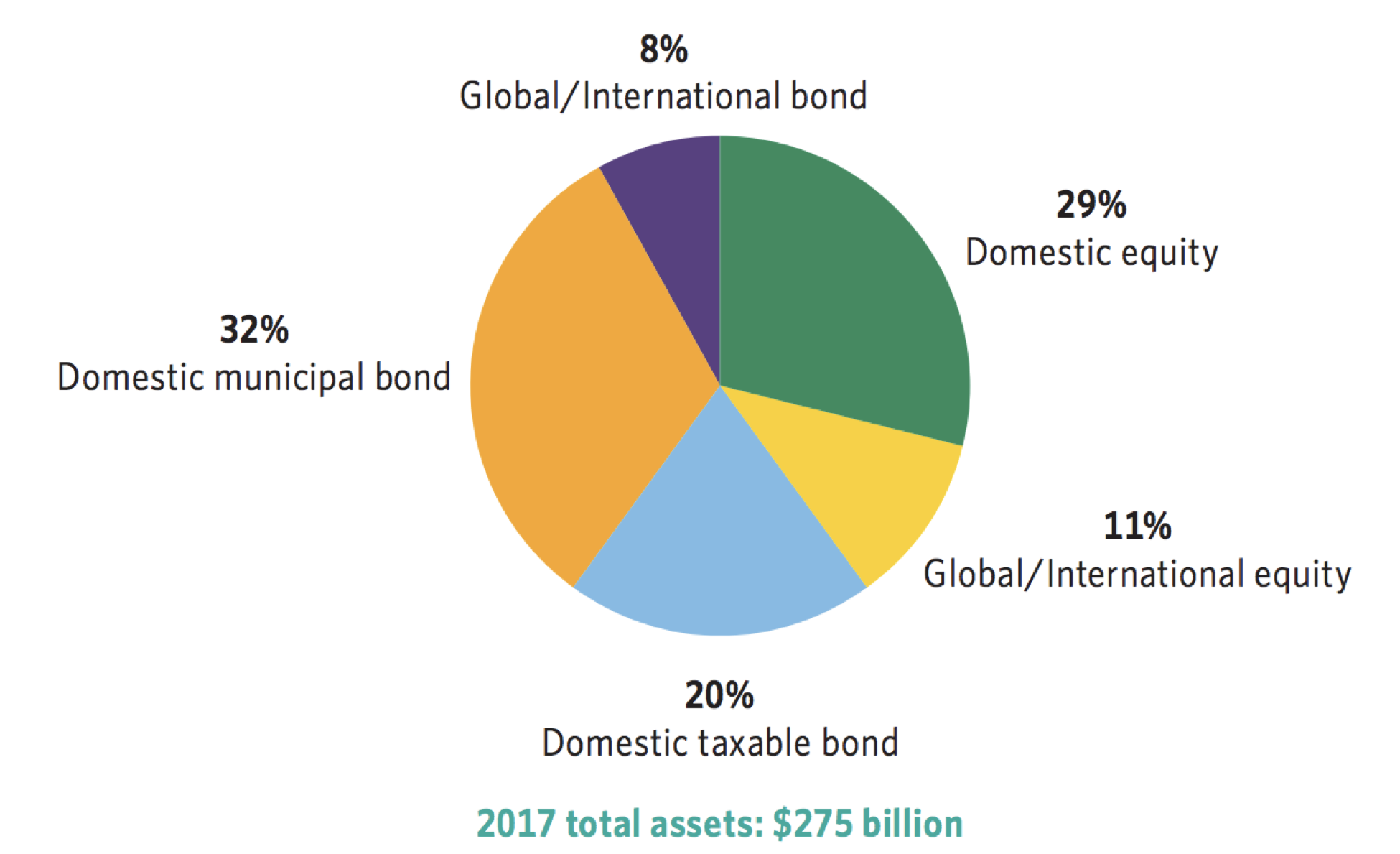

According to the 2018 Investment Company Fact Book, the total asset value of the 530 closed-end funds that existed at the end of 2017 was $275 billion. Bond funds accounted for roughly 60% of closed-end fund assets, with equity closed-end funds representing the remaining 40%.

Source: 2018 Investment Company Fact Book

There are many different types of closed-end funds – diversified equity funds, taxable bond funds, municipal bond funds, sector funds, international equity funds, single-country funds, and more.

Essentially, there is a closed-end fund for almost any type of asset class exposure you are looking to add to your portfolio.

Closed-End Funds are Impacted by Investor Sentiment

Importantly, the market price of a closed-end fund fluctuates like any other stock and is determined by supply and demand of investors in the marketplace.

When a closed-end fund is created, a fixed number of shares are issued to investors during an initial public offering. Once issued, shares are bought and sold by investors in the open market and can trade at a significant discount or premium to their net asset value.

In other words, if a closed-end fund’s assets are worth $10 per share but it is trading at $8.50 per share, you could buy the fund at a 15% discount to its net asset value. If the discount gap closes, you would enjoy some extra capital appreciation on top of the fund’s basic return. However, there is far from any guarantee that the discount will narrow.

Discounts and premiums have historically moved with the business cycle, with extremes on either end being reached during times of maximum investor optimism or pessimism.

For this reason, it is very important to be aware of a fund’s discount or premium, as well as its historical averages. They can vary substantially over time and really impact your total return.

As an example, suppose you discover a closed-end fund trading at a 15% discount to its net asset value. Not bad, right? Maybe, but what if its historical discount is 30%? The fund is actually relatively expensive compared to history.

Just like with high yield dividend stocks, many closed-end funds that trade at substantial discounts could turn out to be too good to be true.

Discounts to net asset value often arise due to the closed-end fund’s poor historical returns, weak credit quality, unsustainable distributions, or subpar portfolio managers, among other factors.

To understand a fund’s current discount or premium, investors can usually ask the fund for its average one-year discount or premium since it started trading. This figure can then be compared to the fund’s current discount or premium.

Many Closed-End Funds Use Financial Leverage

Another distinguishing characteristic of closed-end funds is that many of them use financial leverage as part of their investment strategy. At the end of 2017, roughly 64% of closed-end funds were using leverage as part of their investment strategy, and most funds can borrow between two and three dollars for every dollar in equity.

Leverage can allow closed-end funds to generate more income than most open-end mutual funds.

For example, suppose a closed-end fund had $100 of net assets and invested everything into bonds. If the fund took on $20 of debt to buy more bonds, it would receive more income using the same amount of net assets.

However, leverage increases the fund’s price volatility as well, creating more risk for the investor.

Investors should also be aware that buying closed-end funds at a discount results in additional leverage effects. If a fund’s net assets provide a yield of 10%, investors would lock in a 10% yield if the fund’s shares traded exactly at net asset value.

If shares instead trade at a discount, the investor generates a higher yield than what the underlying securities offer on their own.

Distribution Policies

Closed-end funds typically pay distributions to their investors on a monthly or quarterly basis. Funds adjust their distribution rates up or down for numerous reasons such as market conditions or reinvesting bond maturities at higher or lower interest rates.

Therefore, their dividend payments are often more challenging to forecast than they are for blue chip dividend stocks.

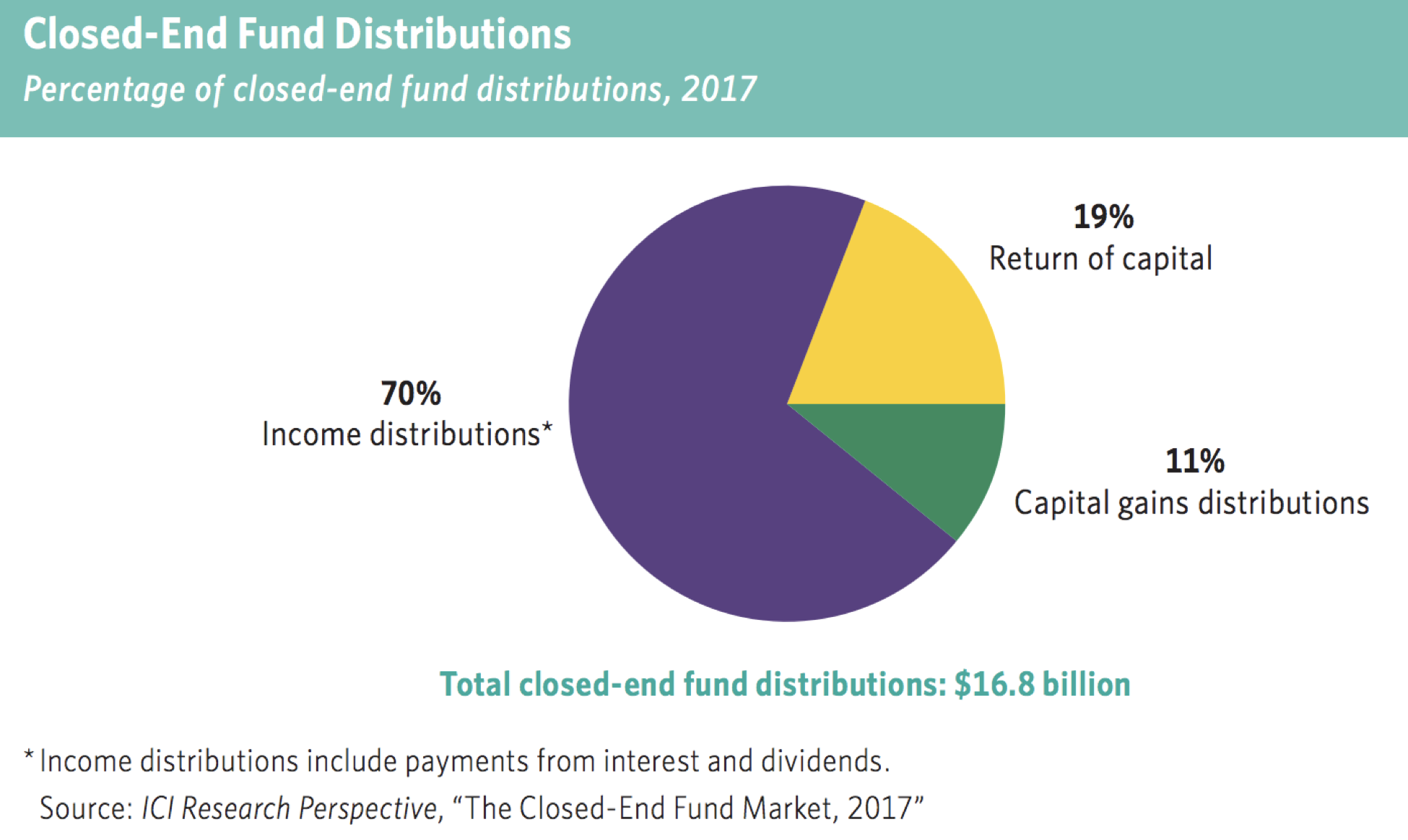

Closed-end funds can make distributions to their shareholders from three sources – income from interest and dividends, realized capital gains, and return of capital (i.e. the money used to pay the distribution comes from the fund’s assets rather than from income generated from the fund’s investment portfolio).

Income distributions accounted for 70% of closed-end fund distributions in 2017, but you can see that return of capital distributions were significant as well.

Source: 2018 Investment Company Fact Book

A fund should ideally generate enough income to fund its distributions, but some frequently return shareholders’ capital instead (i.e. you are investing just to get some of your money back).

If this is the case, you should understand why the fund is not generating enough income to fund its distributions. These funds are gradually eroding their asset base, which is needed to generate future income for distributions.

As a result, the current distribution might not be sustainable and can lead to longer-term challenges for the fund. Additionally, funds that rely heavily on capital gains to fund their distributions might be in trouble in the event of a bear market.

As previously mentioned, distributions can be very sensitive to movements in the stock market. For example, the Gabelli Equity Trust’s (GAB) distribution policy is to pay out 10% of its average net assets each year. If the market crashes 30%, the distribution is almost certainly going to be reduced.

Sure enough, Gabelli Equity Trust’s dividend fell from 80 cents per share in 2008 to 51 cents in 2010, representing a 36% drop. The fund's dividend has yet to fully recover to its pre-crisis high. Unlike many blue chip dividend stocks, closed-end funds can have much less predictable dividend payments.

You need to be sure your lifestyle can tolerate such a shock, and should remain aware of the composition of each fund’s income – some is of higher quality than others. The more reliable funds will have distributions that primarily reflect the dividend and interest income earned from their holdings.

Key Risks of Investing in Closed-End Funds

By now, you are likely familiar with some of the key risks involved with investing in closed-end funds. While they generally offer much greater income potential for every dollar you invest, make sure you are aware of the following risk factors:

Price versus Net Asset Value: the fund’s net asset value (i.e. the market value of its underlying holdings) is often different from the share price of the fund itself. This can help or hurt closed-end fund investors. Although you can likely buy a fund at a discount to its net asset value, the discount could widen by the time you are ready to sell, especially if market conditions weaken, the fund’s performance hits a rough patch, or investor sentiment starts to turn.

Financial Leverage: over 60% of closed-end funds use financial leverage, which magnifies returns up or down. Funds with more leverage are likely to get whipped around more and see larger investment gains or losses. Do you really have the stomach for this?

Distribution Policy: you should fully understand how your fund determines the amount of distributions it pays out. This information should be in the fund’s prospectus. If the fund has been returning capital (i.e. eroding its asset base) to fund part of the distribution, you should find out why it hasn’t been generating enough income. The current distribution rate could be different from future distributions as well, especially if the stock market’s value drops significantly.

Trading Liquidity: since closed-end funds are a much smaller asset class than open-end mutual funds, ETFs, and stocks, some of them have much less trading liquidity. In other words, it could be harder to buy and sell the stock at desirable prices depending on how many people are willing to take the other side of your trade. You should be aware of a fund’s trading volume and bid-ask spreads (i.e. the different in prices between what buyers are currently willing to pay to purchase a share and the price that sellers are currently willing to pay to sell a share – wide gaps are not good) before investing. Using limit orders, which protect against unexpected price movements, is not a bad idea either.

It’s worth repeating that discounts and premiums can be extremely volatile during times of market duress. According to an October 2008 article by the Wall Street Journal, the average discount for U.S.-listed closed-end funds was 4.4% from 1997 through October 2008.

As you know, this period marked the beginning of the financial crisis. Over the three months leading up to October 2008, the weighted average discount for closed-end funds widened from 6.2% to 15.6%, and some funds saw their discounts widen to as much as 25%.

At the time, roughly 72% of closed-end funds used leverage (compared to 64% at the end of 2017), which investors feared would challenge the funds to roll over the debt and result in more expensive financing, hurting returns.

Keep this in mind as you look at high-yielding closed-end funds. Their distribution rates are not guaranteed and are certainly not the same as their total return potential.

How to Invest in Closed-End Funds

Closed-end funds trade just like dividend stocks on a stock exchange or in the over-the-counter market. Investors can easily purchase closed-end funds through their brokerage accounts.

If you are in the beginning stages of researching closed-end funds, Morningstar provides an excellent closed-end funds list. You can view Morningstar’s list by clicking here.

You can select which type of closed-end fund you want (domestic stock, international stock, municipal bond, etc.) and filter on a handful of helpful metrics such as premium / discount, fund manager tenure, standard deviation, and more.

You will quickly notice that analyzing a closed-end fund is very different from analyzing a basic dividend stock. For example, there are no financial statements to evaluate.

Before pulling the trigger on a fund you find in the closed-end funds list, you should make sure you are able to answer the following questions:

How does the fund invest? There are all sorts of different fund types (domestic stock, international stock, municipal bond, etc.), investment strategies (high financial leverage, no leverage, illiquid stocks, etc.), and distribution policies that impact their risk structures. If you can’t get comfortable with the fund’s strategy after reading through its prospectus and reports, move on to the next one (or a different asset class altogether).

Are shares cheap or expensive compared to net asset value and history?Closed-end funds trade at discounts or premiums to their net asset value, depending on supply and demand in the market. The discount or premium can fluctuate significantly, so you should be aware of what it currently is relative to the fund’s history. The price you pay can significantly impact your total return.

How much financial leverage does the fund use? More leverage equals more risk and price volatility. If you cannot stomach large swings in the value of your investments, most closed-end funds might not be appropriate for you.

What is the income distribution composed of? Funding the distribution with capital gains and returns of capital is likely unsustainable and can cause future distributions to differ significantly from the current payment. The most reliable payers have distributions that reflect the income generated by their underlying holdings.

What is the fund’s long-term performance track record? Dividends are only part of the total return equation. While collecting an 8% distribution is nice, what if the fund has chronically underperformed the S&P 500 by 5% per year? You would have been much better off owning the index and occasionally selling shares to fund your income needs – especially after considering the fact that the closed-end fund distribution is likely to be cut during a bear market in many cases (or return part of your capital as a distribution), and closed-end funds (particularly those employing leverage) typically perform poorly when investors turn overly pessimistic (their discounts widen).

Is the fund’s trading liquidity adequate? Some funds are very small, making it difficult or costly to get in and out of positions. Check the fund’s daily trading volume and bid-ask spreads.

For bond funds, what is the fund’s exposure to interest rates? Should interest rates start to rise, the fund’s net asset value could fluctuate significantly. Will the distribution be at risk?

Can my portfolio still meet my income needs if distributions from my closed-end funds get cut in half? Distributions are generally less reliable than the payments you receive from blue chip dividend stocks. Can your lifestyle handle a potential distribution haircut from your closed-end funds?

What are the management fees? The lower the fund’s expenses and fees, the more income you get to pocket. Are the fees reasonable given the fund’s long-term performance track record?

What are the tax consequences? Closed-end funds pass through their tax obligations to the fund’s investors. Since you don’t control when you receive distributions, you need to determine how they will impact the taxes you owe.

You can acquire most of the information above by reading through the fund’s prospectus or distribution announcements. You could probably contact the fund directly as well.

Closed-End Funds: Approach with Caution

Closed-end funds can be an excellent way to generate income. However, if you have made it this far, you are fully aware of the complexities and risks involved with investing in closed-end funds.

Their distribution rates are not the same thing as their total return and are certainly not guaranteed to represent future distributions. The value of your principal investment could also substantially decline, especially during a bear market.

Discounts and premiums can fluctuate significantly with investor sentiment, financial leverage adds further volatility, distributions can be sensitive to the stock market’s current level, and management fees can eat into returns.

It’s never advisable to put all of your income-generating eggs in one basket, and closed-end funds are no exception. In our humble opinion, closed-end funds should not be depended on for more than 20% of a diversified retirement portfolio.

In general, closed-end funds seem most appropriate for relatively sophisticated investors that have well-diversified income portfolios (i.e. their lifestyles could tolerate a 50% drop in income from their closed-end funds), a stomach for price volatility, and a long-term investment time horizon.